- Seasonal RBCT tightness lifted offers, trades stayed limited

- Weak sponge iron capped upside despite steady enquiries

Trade activity remained limited despite higher offers, as ample domestic coal capped acceptance.

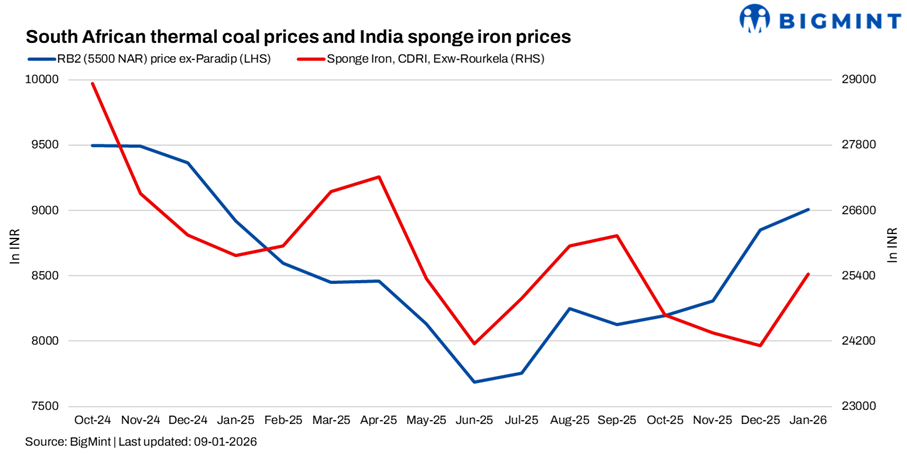

Indian portside South African thermal coal prices increased marginally by INR 50/t w-o-w in the week ended early January 2026. Exw Paradip, RB2 (5,500 NAR) rose to INR 9,050/t, while at Vizag, RB2 increased to INR 8,950/t. RB3 (4,800 NAR) also firmed up, rising to INR 7,600/t at Paradip and INR 7,550/t at Vizag, each up INR 50/t w-o-w.

Market offers moved to the higher end this week, supported by temporarily lower coal availability. Market participants noted that such seasonal firmness is typical during this period, as operations at Richards Bay Coal Terminal slow during peak winter conditions and New Year holidays. Offers for RB2 across Mangalore, Ennore, Paradip, and Gangavaram were quoted in the range of INR 9,000-9,300/t, though no trades were concluded at these elevated levels.

On the export front, FOB RBCT RB2 (5,500 NAR) prices hovered around $78-79/t, while bids remained lower at $73-74/t. RB3 (4,800 NAR) FOB offers were around $68-69/t against bids near $61/t. Cargo availability remained tight, with January and February laycan cargoes largely sold out, though enquiries were reported to be gradually increasing.

India’s portside thermal coal inventories stayed broadly stable w-o-w at 12.95 mnt in week 1 of 2026, marginally higher than 12.91 mnt in week 52, as holiday-related disruptions muted both arrivals and evacuation.

In contrast to coal, the Indian sponge iron market weakened. Prices declined by INR 200-500/t across southern, eastern, and central regions amid weak enquiries and subdued finished steel demand. Sponge Iron (CDRI), exw-Rourkela, fell by INR 300/t w-o-w to INR 25,000/t exw, reducing immediate fuel cost pass-through support.

Domestic coal prices remained unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t. Comfortable availability across key regions continued to keep procurement largely need-based.

Outlook

South African thermal coal offers may remain firm in the near term due to seasonal export tightness and gradual enquiry improvement. However, subdued sponge iron prices and ample domestic coal availability are likely to limit deal closures at elevated levels.

Leave a Reply