- Demand remains weak from steel, textile sectors

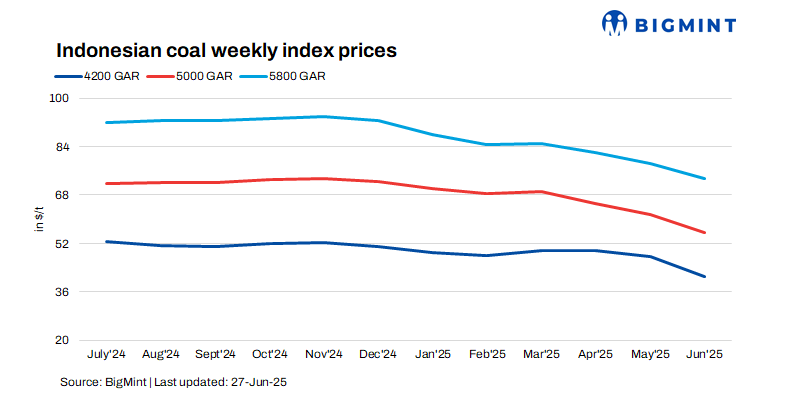

- Indonesian weekly coal index shows mix trends

Indonesian thermal coal prices continued to remain under pressure across key Indian ports during the week ending 27 June 2025. The market remained under pressure due to weak demand from core industrial sectors such as steel and textiles, which restricted aggressive buying. Most procurement activity was limited to need-based or speculative purchases. While overall sentiment remained subdued, portside prices largely held firm, reflecting a balance between supply and demand conditions.

As per BigMint’s assessment, the 5000 GAR grade saw a price drop of INR 50/t, reaching INR 7,400/t at Kandla and INR 7,300/t at Vizag. Likewise, the 4200 GAR declined by INR 50/t, settling at INR 5,750/t at Kandla and INR 5,650/t at Vizag.

The lower calorific value 3400 GAR grade also remained flat at INR 4,300/t at Navlakhi Port. Despite notable w-o-w corrections in indexed prices, local price movements at Indian ports were limited, indicating that fundamentals remained in equilibrium.

Portside inventories reflect controlled replenishment

Portside thermal coal inventories in India witnessed a marginal weekly decline, falling to 15.87 million tonnes (mnt) in Week 25 of the current calendar year, compared to 16 mnt in the previous week. This decrease was attributed to subdued vessel arrivals at some ports, even though a few locations experienced fresh stock inflows.

This inventory trend is consistent with the market’s cautious buying approach, where stockpiles are managed conservatively in anticipation of continued moderate demand through the monsoon season. Traders and consumers alike appear to be maintaining lean inventories, with no immediate concerns about shortages due to the prevailing supply surplus.

Power sector coal stocks edge up

Coal inventories at Indian power plants increased slightly over the week, with total stocks standing at 61.47 mnt as of 25 June 2025, up from 61.38 mnt a week earlier. These levels are sufficient to sustain approximately 21 days of power generation under standard operating conditions, providing short-term fuel security for utilities.

However, the stock situation remains uneven across plants. A total of 14 power stations reported critically low coal stock levels. Among these, seven plants are dependent on domestic coal, five rely on imported coal, and two use washery rejects. This disparity in fuel distribution highlights ongoing logistical bottlenecks and regional imbalances, despite overall adequate national stock levels.

Global benchmark prices show mixed trends

Internationally, Indonesian benchmark coal prices showed mixed w-o-w movements due to persistent oversupply concerns and reduced demand from major importers such as China and India. The 5800 GAR grade declined by $0.29/t to $71.96/t, reflecting ongoing weakness in the global market. In contrast, the 4200 GAR increased by $0.20/t to $39.45/t, possibly driven by spot purchases or short-term logistical constraints. Meanwhile, the 3400 GAR slipped by $0.75/t to $30.10/t.

These fluctuations suggest that while broader market sentiment remains bearish, individual price movements are being influenced by regional trading dynamics, stock levels at end-user locations, and short-term supply shifts.

Market outlook: Short-term stability expected

Indonesian thermal coal prices in India are expected to remain range-bound, supported by steady domestic supply and weak monsoon-season demand. Barring unforeseen demand spikes or supply disruptions, price movement is likely to be limited.

Leave a Reply