- Weak demand and ample domestic supply weighed on portside thermal coal prices

- Limited high-GAR Indonesian cargoes may support premium coal prices

Indian portside prices of Indonesian-origin thermal coal softened during the week ended 10 July 2026, primarily due to subdued buying interest and sufficient domestic coal availability, which continued to limit the need for imported cargoes.

Buyers largely restricted procurement to immediate consumption requirements, while adequate inventories and consistent domestic coal supplies kept spot market activity subdued.

According to market participant “demand remained weak across key consuming sectors, leading to lower transaction volumes and downward price corrections. Although vessel availability remained limited, exporters in Indonesia continued to manage supply cautiously to avoid excessive price erosion.”

Market participants also highlighted that “exports of higher-calorific (high GAR) coal have been constrained as Indonesian producers continue prioritizing domestic requirements under the country’s Domestic Market Obligation (DMO) framework before allocating volumes for exports.”

Prices correct across major Indonesian coal grades

Price corrections were observed across all major Indonesian thermal coal grades at Indian ports as weak buying sentiment outweighed emerging supply-side concerns.

Prices of 5,000 GAR Indonesian coal declined by around INR 400/t week-on-week, settling at approximately INR 10,550/t at Kandla and INR 10,450/t at Vizag. The sharper decline reflected limited spot demand despite expectations of tighter availability of premium-grade cargoes.

Similarly, 4,200 GAR coal prices eased by around INR 150/t, reaching nearly INR 8,900/t at Kandla and INR 8,800/t at Vizag, while 3,400 GAR coal prices fell by approximately INR 100/t to around INR 6,850/t at Navlakhi, as abundant domestic coal availability reduced the requirement for lower-grade imported material.

Lower freight rates offer partial cost relief

Freight rates for Supramax vessels operating on the East Kalimantan-Navlakhi route declined sharply by around $2.9/t week-on-week to nearly $17.5/t. The correction was mainly attributed to improved geopolitical sentiment, softer chartering demand, and reduced cargo movement across regional trade routes. While lower freight costs marginally eased import economics, they were insufficient to stimulate significant buying activity amid the prevailing weak demand environment.

Port inventories rise on slower cargo offtake

India’s thermal coal inventories at major ports increased by 1.6% week-on-week to approximately 15.07 million tonnes (mnt) in Week 27, compared with 14.83 mnt in the previous week. The increase was primarily driven by slower cargo evacuation as consumers relied on existing inventories and deferred fresh purchases.

Steady domestic coal production, supported by regular supplies from Coal India and lower seasonal demand during the monsoon, continued to reduce dependence on imported coal, resulting in a gradual accumulation of stocks at port locations.

Power plant coal stocks remain comfortable despite weekly decline

Coal inventories at Indian thermal power plants declined by around 2% week-on-week to approximately 42.6 mnt as of 9 July 2026, equivalent to nearly 14 days of consumption. Although inventories moderated, overall domestic coal availability remained sufficient to meet power sector requirements.

However, nearly 28 thermal power plants continued to report critical stock levels, reflecting localized logistical bottlenecks and uneven coal distribution rather than a broad-based supply shortage.

Global thermal coal market continues to face demand pressure

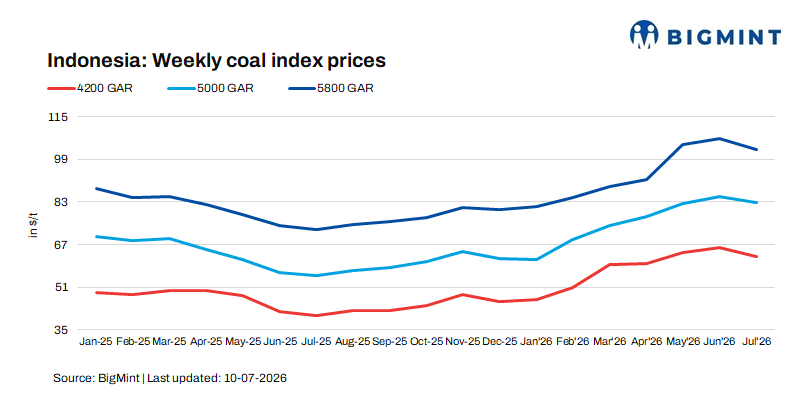

The international thermal coal market remained under pressure during the week as cautious procurement by major importing countries, particularly China and India, continued to weigh on prices. Indonesian benchmark coal prices softened across major grades, with 5,800 GAR and 4,200 GAR coal declining by around $1-2/t week-on-week, while 3,400 GAR prices eased by approximately $0.5-1/t.

The weakness was largely driven by comfortable inventories among end-users, subdued industrial demand, and restrained spot buying across the Asian seaborne market despite emerging concerns over tighter availability of higher-GAR Indonesian cargoes.

Outlook

Indian portside thermal coal prices are expected to remain broadly stable to slightly firm over the coming weeks. While comfortable domestic coal availability, adequate inventories, and subdued seasonal demand are likely to continue limiting import requirements, upside risks are emerging for premium high-GAR Indonesian coal due to restricted export availability under Indonesia’s domestic supply prioritization policy.

Additionally, any escalation in geopolitical tensions or disruptions to global shipping routes could increase freight costs and tighten seaborne supply, providing support to imported coal prices. However, unless industrial demand and power sector procurement improve materially, any price recovery is expected to remain gradual and largely confined to premium-grade cargoes.

Leave a Reply