- Energy policy, fuel substitution, geopolitics to shape thermal coal prices

- Met coal critical mineral for India; Southeast Asia + India key market driver

Data Deep Dive: Global thermal and metallurgical coal (a collective term for coking coal and pulverised coal injection) markets have historically tended to move in tandem, with stronger or weaker economic activity influencing demand for both power generation and steel production. However, currently these two markets are responding to very different economic drivers, resulting in a clear divergence in both pricing behaviour and trade flows.

Although FOB prices of both Indonesian 4,200 GAR thermal coal and Australian premium hard coking coal (PHCC) have recovered by around 25% from CY’25 averages to $58.12/t and $236.84/t, respectively, the similarities largely end there.

Thermal coal’s recovery has been driven primarily by geopolitical risks and energy security concerns, even as demand from the two largest importers, China and India, has remained subdued despite lower export availability from Indonesia and Russia. Metallurgical coal, by contrast, has been supported by tightening supply fundamentals and robust demand from India, offsetting uneven steel consumption elsewhere.

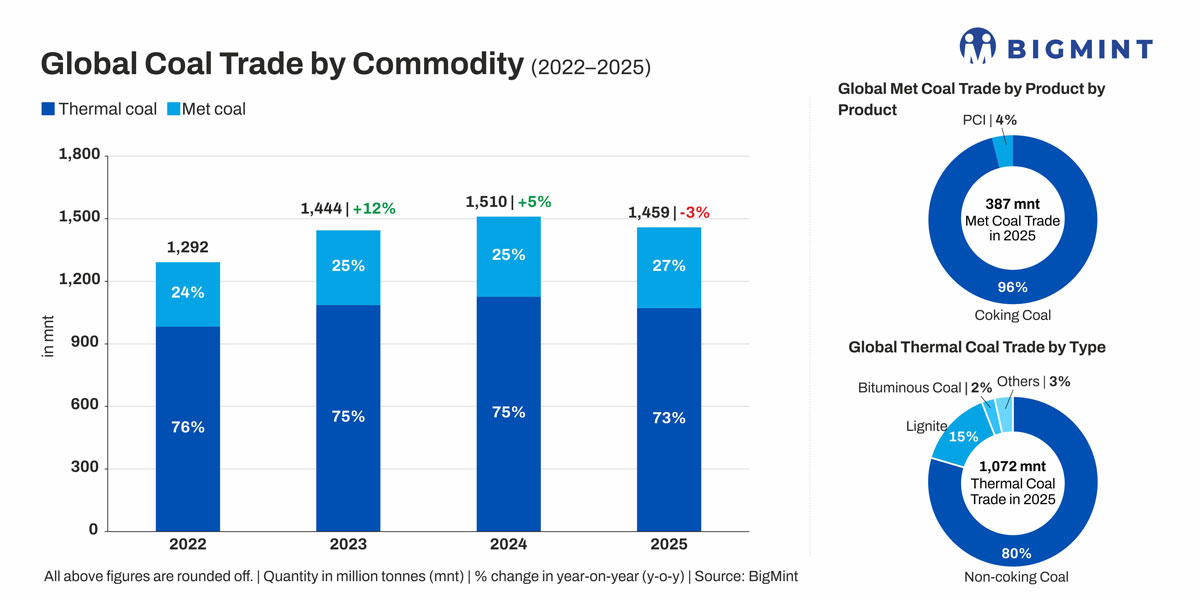

CY’25 trade patterns also reflect this divergence. According to BigMint data, global seaborne thermal coal trade expanded from 983 million tonnes (mnt) in CY’22 to a record 1.13 billion tonnes (bnt) in CY’24 before easing to 1.07 bnt in CY’25 as cooler weather and renewable energy capacity additions reduced coal-based power demand. Metallurgical coal trade, meanwhile, has continued to grow steadily, rising from 309 mnt in CY’22 to a record 387 mnt in CY’25.

Thermal coal remains supported by energy market dynamics in CY’26

In CY’26, thermal coal continues to derive support from factors extending well beyond the coal sector itself, with prices influenced as much by developments in gas and electricity markets as by traditional coal supply-and-demand balances.

Across Asia, utilities remain focused on securing reliable fuel supplies amid persistent uncertainty in gas and LNG markets, especially given the recent Middle East crisis. Coal continues to play a critical role in electricity generation across major importing nations, particularly where power demand growth remains robust and renewable energy deployment has yet to contribute meaningfully to baseload generation.

Supply-side disruptions have further supported prices. In Indonesia, the world’s largest thermal coal exporter, recurring policy interventions, including changes to mining work plans and budgets (locally known as RKABs), domestic market obligation (DMO) rules, royalty frameworks, export licensing procedures, and benchmark pricing mechanisms, have increased uncertainty over export availability. Although quotas for more than 600 mnt of production have been approved for CY’26, this remains well below the country’s CY’25 output of 790 mnt.

Russian exports, another key source of seaborne thermal coal supply, continue to face mounting challenges. Coal production fell 5% y-o-y to 176.7 mnt in January-May 2026, with output from the Kuzbass basin also declining 5% to 77.5 mnt. Higher rail tariffs, logistics bottlenecks, a stronger rouble, and rising costs have squeezed margins. As a result, Russian suppliers are becoming less able to respond to demand surges, tightening seaborne supply and helping support thermal coal prices.

However, these remain largely short-term drivers. Indonesian thermal coal prices are still well below the 2022 energy crisis average of $85.52/t, indicating that the current recovery reflects temporary supply disruptions rather than a structural tightening of the market. Over the longer term, growing renewable generation, natural gas, nuclear power, and energy storage are set to gradually reduce coal’s share in electricity generation, creating a more balanced market once geopolitical risks ease.

Metallurgical coal faces different reality

The metallurgical coal market is operating under a different set of conditions in CY’26. Although global crude steel production declined by 1.5% during January-May 2026 to 773.1 mnt and steel demand remains uneven across many regions, PHCC prices are around 26% higher than CY’25 averages.

This shows that supply-side developments are increasingly offsetting the impact of softer steel demand. Australia, which accounts for more than half of global seaborne metallurgical coal exports, is facing increasing questions about its long-term production outlook. The International Energy Agency has projected Australian coal exports could decline by around 5% by CY’27, while industry participants increasingly point to a shrinking pipeline of new metallurgical coal projects.

Additionally, several major miners have reduced exposure to the sector. Rio Tinto exited metallurgical coal mining in 2018, while Anglo American has divested its coking coal business. Investors and lenders are becoming increasingly reluctant to fund new greenfield coal projects amid tightening climate policies and ESG pressures.

Australian banks have also adopted more restrictive financing policies. The National Australia Bank has stated it will not provide project financing for greenfield metallurgical coal mines, reflecting expectations that lower-emission steelmaking technologies will gradually reduce long-term coal demand. At the same time, growing scrutiny of methane emissions from coal mining is adding another layer of regulatory risk for future supply growth.

The changing supply landscape is also evident in trade flows. Australia’s share of global seaborne metallurgical coal exports has fallen from nearly 50% in CY’22 to below 40% in CY’25, while Russia and Mongolia have accounted for much of the incremental supply growth. However, premium Australian coals remain difficult to replace in blast furnace operations, limiting the extent to which buyers can diversify.

This tightening supply outlook comes even as China’s steel production enters a structural downtrend, with incremental metallurgical coal demand shifting elsewhere in Asia. To illustrate, India (193 mnt/year announced or under construction) alone accounts for 60% of global blast furnace (BF) capacity under development in CY’26, according to the Global Energy Monitor, with China responsible for 26% (76 mnt). Substantial BF capacity additions are also underway in Southeast Asian countries such as Vietnam (8 mnt/year), Indonesia (3 mnt/year), Myanmar (4 mnt/year), and Malaysia (17 mnt/year).

India gains importance across both markets

One theme connecting the thermal and metallurgical coal sectors is the growing significance of India. Rising electricity consumption, continued industrialisation, and infrastructure investment are supporting demand for both thermal and coking coal imports. As growth in some mature markets slows, India is increasingly viewed as the most important source of incremental seaborne coal demand.

India’s import trends also reflect the changing dynamics across the two markets. Over CY’22-25, India’s overall coal imports have remained broadly stable, fluctuating between 264 mnt and 271 mnt. Beneath this stability, however, the composition of imports is changing.

For thermal coal suppliers, India remains a key destination for imported fuel required by cement producers, industrial users, and power generators, accounting for around 15% of global trade flows in CY’25, though this was lower than CY’22’s 18%.

Rising renewables capacity and ample domestic coal inventories have contributed to reducing India’s thermal coal import dependence. To illustrate, India’s non-coking coal imports fell 6% to around 163 mnt in CY’25, while volumes fell by a sharper 12% y-o-y to a four-year low of 65 mnt during January-May 2026 despite widespread heatwaves.

Conversely, for metallurgical coal exporters, the country’s expanding steel sector continues to provide an important source of long-term demand growth. India’s coking coal imports increased from 54 mnt in CY’23 (15% share of global trade) to 62 mnt in CY’25 (16%), reflecting continued blast furnace capacity additions. More importantly, most of the incremental growth has come from imports of hard coking coal and premium hard coking coal, rather than lower-quality grades.

As a result, developments in India are becoming increasingly important to pricing and trade flows across the broader coal complex.

Outlook

The divergence between thermal and metallurgical coal markets is likely to become more pronounced through the remainder of 2026 and into the next decade.

For thermal coal, demand growth is expected to moderate as renewable energy capacity expands, particularly in China, the world’s largest producer and consumer. The International Energy Agency (IEA) expects global coal demand to plateau before gradually declining towards CY’30, driven largely by China’s energy transition. The country expects coal consumption to peak during 2026-2030 and aims to raise non-fossil fuels’ share of energy consumption to 25% by CY’30.

Metallurgical coal faces a markedly different outlook. While steel demand is expected to grow at a slower pace as China’s property sector continues to contract, supply growth is becoming increasingly constrained. Industry forecasts increasingly point to a widening supply deficit for premium coking coal over the coming decades.

India is set to play a larger role in both markets. Its expanding power sector will continue to support thermal coal imports even as domestic production rises, while rapid steel capacity additions will make it the largest source of incremental seaborne metallurgical coal demand. Consequently, pricing across both markets is likely to become increasingly sensitive to Indian import trends.

The result is a growing divergence in market fundamentals. Thermal coal is evolving into a security-of-supply commodity, with prices increasingly dictated by energy policy, fuel substitution, and geopolitical disruptions. Metallurgical coal, by contrast, is becoming a scarcity-driven raw material, where investment decisions and supply availability are likely to have a greater influence on prices than cyclical fluctuations in steel demand. This divergence is expected to shape global coal trade flows well beyond CY’30.

Leave a Reply