- Global benchmarks exhibit mixed trends

- Rising inventories cap price gains

Indian portside prices of Indonesian-origin thermal coal remained broadly stable week-on-week as of 3 April, after witnessing mild firmness earlier in the week.

The market tone softened toward the latter part of the week as industrial demand moderated, prompting buyers to adopt a cautious wait-and-watch approach. Despite sufficient availability of cargoes at major ports, procurement activity slowed as traders and end-users assessed near-term demand conditions and price direction.

Portside price movement across key grades

Portside prices across most Indonesian coal grades remained largely unchanged week-on-week, reflecting balanced supply and demand conditions.

According to BigMint’s latest assessment, prices of 5,000 GAR Indonesian coal were assessed at around INR 9,400/t at Kandla and INR 9,300/t at Visakhapatnam, holding steady from the previous week. Stable pricing in this segment was supported by adequate inventories and measured buying interest from industrial consumers.

Similarly, prices of 4,200 GAR coal remained unchanged at INR 7,700/t at Kandla and INR 7,600/t at Visakhapatnam. Limited spot buying by industrial users and sufficient cargo availability at ports kept price movements largely muted.

In contrast, prices of lower-grade 3,400 GAR coal declined slightly by around INR 50/t week-on-week to approximately INR 5,450/t at Navlakhi Port. The decline was primarily driven by weaker industrial offtake and cautious procurement by traders, particularly from sponge iron and small industrial consumers.

Port inventories rise amid steady cargo arrivals

Portside thermal coal inventories across India registered a moderate increase during the week, indicating steady inflows of imported cargoes. Total port inventories rose by around 5.8% week-on-week to 13.10 million tonnes in week 13, compared with 12.38 million tonnes in week 12.

The stock build-up was largely driven by higher arrivals at east coast ports such as Paradip and Dhamra, which offset the decline observed at Mundra. While overall demand remained steady, selective restocking by traders and industrial buyers contributed to the gradual increase in port inventories.

Power sector coal stocks remain comfortable

Coal inventories at Indian thermal power plants also improved marginally during the week, reinforcing the comfortable supply position in the domestic power sector. As of 2 April 2026, total coal stocks at thermal power plants stood at approximately 58.8 million tonnes, equivalent to around 19 days of consumption.

However, stock distribution across the power sector remains uneven. Around 24 thermal power plants are currently operating with critical coal inventory levels. Among these, 14 plants rely on domestic coal supply, seven depend on imported coal, and three operate on washery rejects. This highlights persistent logistical and supply chain challenges despite the overall comfortable national stock position.

Benchmark prices and freight influence import parity

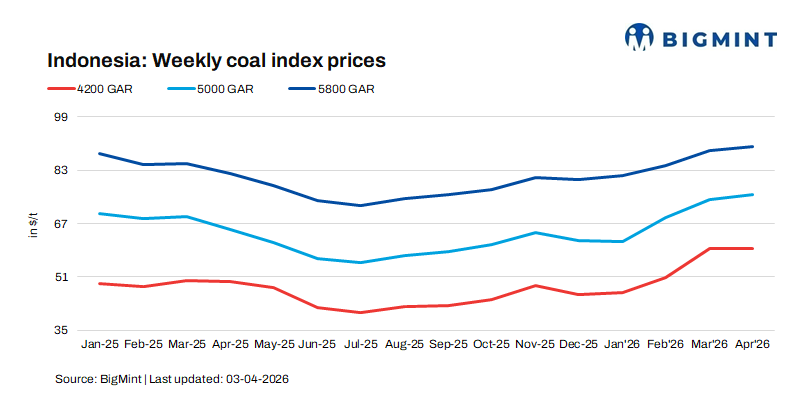

International market indicators presented a mixed trend during the week. Indonesian benchmark coal prices showed marginal increases for higher-calorific grades, with 5,800 GAR coal rising by around $0.6-1/t w-o-w. In contrast, 4,200 GAR coal prices remained largely stable, while 3,400 GAR coal prices declined slightly by around $0.45-0.6/t.

Freight rates for shipments to India also softened during the week, providing limited relief to import costs. Supramax freight from East Kalimantan to Navlakhi declined by about $1/t week-on-week to approximately $18/t, slightly improving import economics for buyers.

Outlook

We expect Indian portside prices of Indonesian thermal coal to remain muted in the near term amid comfortable inventories, stable global benchmarks, and moderate demand. However, gradual restocking ahead of the summer season may support buying interest, particularly for lower-CV grades due to cost optimisation. Price movements will largely depend on trends in international benchmarks, freight rates, and industrial demand recovery.

Leave a Reply