- Rising global scrap prices, US steel tariffs boost export demand

- Following absence in Feb, NMDC, SAIL auctions see price hikes

- Production costs rise amid soaring domestic met coke prices

Morning Brief:India’s pig iron prices reached a five-month high in March 2025, propelled by an uptick in export demand, a heightening supply squeeze, rising raw material costs, and positive finished market sentiments.

Prices in Durgapur, India, climbed up by INR 2,800/tonne (t) ($32/t) m-o-m to a monthly average of INR 35,800/t ($413/t) in March compared to INR 33,000/t ($381/t) in February, with similar levels last seen in November 2024. In tandem, Tata Metaliks, a leading market player, increased pig iron prices twice in March by a total of INR 2,500/t ($29/t) to INR 40,000/t ($462/t) exw-Kharagpur.

Factors supporting price surge

Export shipments climb up amid high scrap tags, US steel tariffs

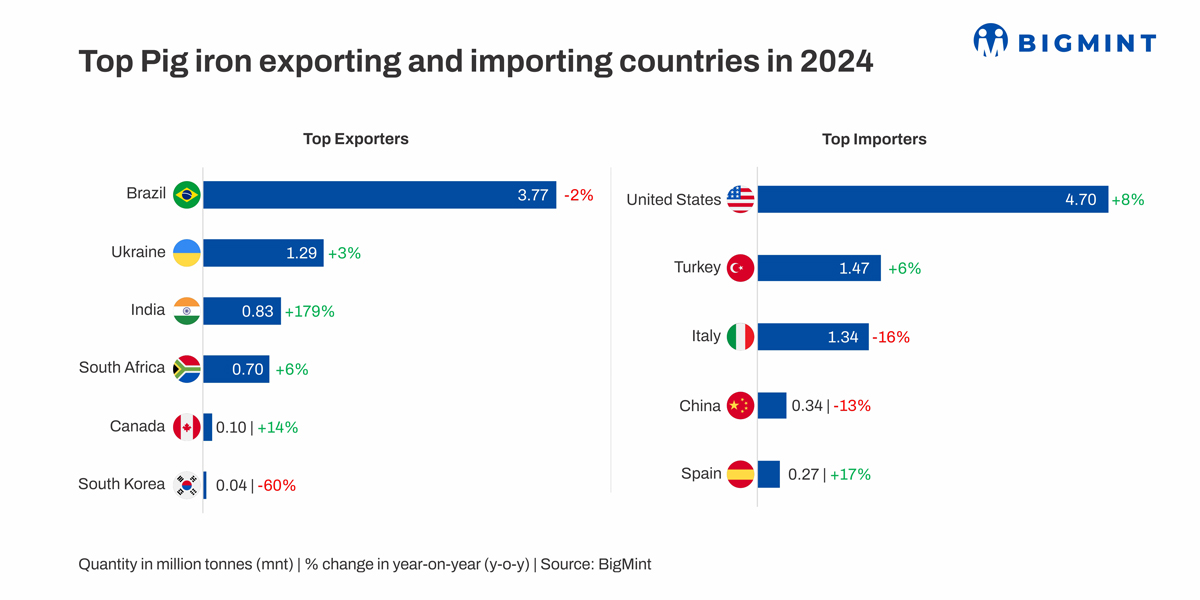

Pig iron export shipments increased in March, as major market players capitalised on favourable global dynamics. Notably, Vedanta concluded deals for around 100,000 t in March, primarily to Southeast Asian markets, while Welspun’s bookings touched nearly 35,500 t, targeting Middle Eastern buyers. Bookings for the US stood at around 140,000 t, according to provisional data.

The rise in exports could be attributed to the following:

(a) 25% tariffs on US steel imports: President Donald Trump’s blanket 25% tariffs on US steel imports went into effect on 12 March, which led to robust bookings from the US, a major pig iron export destination for India. To avoid the additional tariffs on finished steel, market participants in the US resorted to panic buying of feedstock, including imported pig iron. Additionally, amid increased scrutiny on trade with Brazil, India became the preferred choice for importers. Notably, Indian sellers can generally secure premium pricing from the US, which provided them further incentive for exports.

(b) Shortfall in scrap supply: Ferrous scrap, for which pig iron is a key alternative, was in short supply, which led to its prices surging globally. To illustrate, in March, average CFR values of US-origin HMS 80:20 scrap to Turkiye stood at around $376-377/t, an increase of $15-20/t m-o-m. Conversely, pig iron emerged as a more cost-effective option in March. FOB prices of material from the Black Sea region (Russia) were recorded at $339/t, an increase of $12/t m-o-m.

Supply tightens amid production cuts, labour issues

Domestic pig iron availability tightened in March due to a number of factors. Notably, in March, a few mills experienced production cuts totalling approximately 25,000-30,000 t, which led to a supply shortfall boosting prices.

The following factors contributed to limited pig iron supply:

(a) There were production disruptions at key integrated steel plants, compounded by seasonal factors.

(b) Increased export activity from major players such as Vedanta and Welspun impacted supply in the domestic market.

(c) Due to thinning margins, some merchant pig iron manufacturers were operating at lower capacity.

(d) Supply from auctions was limited, with NMDC not holding any in February. SAIL also conducted only one auction in February, offering only 1,500 t. This contributed to the supply constraints in February, though auction volumes picked up in March.

(e) Procurement increased, due to higher finished steel demand and increased preference for pig iron due to limited availability of scrap. With the onset of Ramzan, a labour shortage arose, which led to lower scrap collection in the domestic market. Amid tightening scrap availability, steelmakers turned to pig iron for their raw material needs.

Met coke prices rise amid import restrictions

Domestic met coke prices climbed up significantly following the imposition of import quotas in December 2024, pushing up production costs for pig iron producers. Blast furnace (BF) grade coke stood at INR 34,500/t ($398/t) exy-Jajpur in March, a rise of INR 2,700/t ($31/t) from INR 31,800/t ($367/t) in December and INR 400/t ($4/t) from February’s INR 34,100/t ($394/t).

Gandhidham witnessed a steeper increase, with prices rising by INR 3,600/t ($42/t) to INR 32,300/t ($373/t) in March against INR 28,700/t ($331/t) in December and by INR 600/t ($7/t) compared to INR 31,700/t ($366/t) in February.

This follows a significant drop in met coke imports, with volumes touching a 2.5 year low in early March.

Auction prices rise following limited supply in Feb

Auctions by Evonith Steel, SAIL’s Rourkela Steel Plant and NMDC’s Nagarnar Steel Plant received a robust response, highlighting strong demand for pig iron despite rising prices. This followed limited auctions in February, which also contributed to constrained domestic supply.

In January, NMDC saw a total of 32,000 t booked at INR 30,500-31,500/t ($352-364/t). The company did not hold any auction in February, leading to a temporary gap in supply. When it resumed auctions in March, NMDC was able to sell 28,000 t at INR 34,000-34,500/t ($393-398/t), which denotes a clear upward shift in pricing.

Additionally, in recent times, SAIL’s pig iron auction activity has been limited to its Rourkela plant. Only one auction was held in February, offering 1,500 t, which concluded at INR 32,600/t ($376/t). However, March witnessed a substantial pick-up in RSP’s auction volumes, with a total of 41,000 t booked at significantly higher prices of INR 35,500-36,500/t ($410-421/t).

Evonith’s auctions in March also saw steady price increases, with 6,000 t booked at INR 35,350/t ($408/t) on 3 March and then escalating to INR 35,800/t ($413/t) on 24 March.

The overall m-o-m rise in auction prices, especially in March, can be attributed to constrained supply in February due to NMDC’s absence, followed by renewed demand in March. NMDC’s and SAIL’s return to the market at higher prices supported the upward momentum in domestic pig iron pricing.

Finished steel sees firm demand

Steel mills, particularly those catering to the infrastructure and construction sectors, witnessed steady demand for finished products last month.

Several construction firms were in a rush to meet project deadlines by FY-end, leading to robust bookings. Accordingly, rebar and structural steel prices surged m-o-m. For example, rebar (Fe 500) tags increased by INR 1,500/t ($17/t) m-o-m to INR 49,400/t ($570/t) exw-Mumbai, while trade prices of the BF variant rose by INR 2,100/t ($24/t) m-o-m to average INR 54,900/t ($634/t) exy-Mumbai in March.

This demand uptick ultimately percolated to the raw material segment, leading to strengthening of pig iron prices.

Outlook

Pig iron prices may witness corrections in the near term, with the buoyant trade momentum of March having dissipated early on in April.

In fact, by the end of March, the market outlook appeared positive, with signs of an upward trend continuing into the first week of April. However, sentiments weakened from the second week, driven by reduced buying interest in finished steel and increased availability of scrap in the market. The easy availability of HMS at lower prices further pressured pig iron tags, leading to a decline of around INR 1,550/t ($18/t) in Durgapur till latest assessments on 19 April.

Moreover, the latest auction by NMDC also witnessed a weak response, with just about 30% of the offered quantity getting booked.

However, prices are likely to receive support from limited domestic availability, which could cap significant drops.

Leave a Reply