- Imports fall sharply m-o-m as buyers avoid high landed costs

- US share declines while Middle East supply gains presence

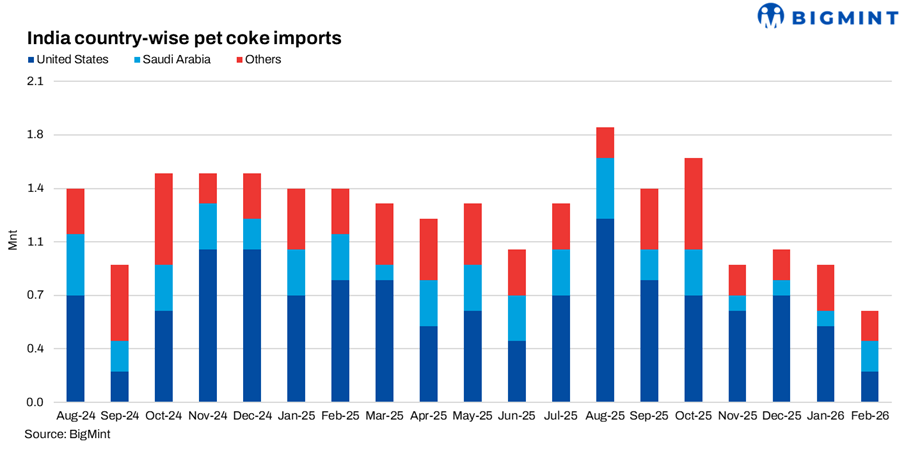

India’s pet coke imports dropped to 0.6 mnt in February, down 33.3% m-o-m from 0.9 mnt in January, marking one of the lowest monthly import volumes in recent years, as per data maintained with BigMint. The last comparable low was 0.5 mnt in February 2022, indicating a sharp contraction in overseas procurement.

The decline reflects cautious buying behaviour among cement and industrial consumers, as imported pet coke prices remained elevated and freight costs increased. Market participants indicated that many buyers relied on existing inventories and domestic supply, while delaying fresh bookings due to uncertainty in global markets.

Imports from US drop sharply

The United States remained the largest supplier, exporting 0.2 mnt in February, accounting for roughly 33.3% of total imports. However, shipments from the US declined sharply by 60% m-o-m from 0.5 mnt in January, reflecting weaker buying interest at higher CFR levels.

Saudi Arabia supplied 0.2 mnt, doubling from 0.1 mnt in January, increasing its share to around 33.3% of India’s total imports. The increase highlights a partial shift toward Middle East supply as buyers diversified procurement sources.

Other exporters included Netherlands, Oman, and Kuwait, each supplying 0.1 mnt in February. These secondary origins collectively accounted for around 50% of February shipments, highlighting a broader diversification in sourcing.

Meanwhile, Venezuela, which supplied 0.2 mnt in January, recorded no shipments in February, contributing significantly to the overall decline. Other minor origins such as Argentina and Malaysia also did not feature in February shipments.

Top buyers

On the buyer side, Ultratech Cement remained the largest importer, procuring 0.2 mnt in February, although volumes declined 33.3% m-o-m from 0.3 mnt in January.

Reliance Industries imported 0.1 mnt, down 50% m-o-m from 0.2 mnt, reflecting lower procurement as the company continues to rely heavily on captive production and inventory adjustments.

Other buyers included Rain CII and Sanvira Industries, each importing 0.1 mnt, broadly stable month-on-month.

New buyers in February included Chettinad Cement and Shri Cement, each importing 0.1 mnt, while several January importers such as Zuari Cement, Birla Corporation and Dalmia Cement did not record shipments in February.

Market overview

The fall in imports coincided with sharp increases in imported pet coke offers during February and early March. Global supply disruptions and higher freight rates pushed US-origin pet coke offers to around $150-155/t CNF India in March, compared with around $121-124/t earlier in the year.

Freight costs also increased significantly as shipping routes through the Middle East faced disruption amid geopolitical tensions, raising insurance premiums and voyage costs. These developments pushed landed replacement costs higher, discouraging aggressive buying.

At the same time, domestic market dynamics also influenced import behaviour. Many cement players have shifted towards sourcing thermal coal domestically or imports, instead of going for pet coke imports amidst thin margins. Indian refiners raised domestic pet coke prices sharply during March, while Reliance Industries continues to consume its entire pet coke production captively, limiting merchant supply availability.

Market implications

The sharp decline in February imports suggests that the pet coke market is currently being driven more by cost pressures than by demand expansion. Buyers appear to be adjusting procurement strategies, balancing between domestic supply, alternative fuels, and imported cargoes.

While India remains one of the largest global pet coke import markets due to strong cement sector demand , the February figures highlight short-term demand moderation driven by price sensitivity and inventory management.

Going forward, import volumes will largely depend on global freight movements, Middle East shipping stability, and relative pricing versus coal, all of which will influence fuel-mix decisions by cement and industrial consumers.

Leave a Reply