- Pellet offers remain stable in Raipur

- Sponge iron, billet prices drop by INR 500/t w-o-w

Pellet prices in Raipur continued to remain stable over the last couple of days, with market activity subdued due to the ongoing festive season. Trading volumes have been minimal as buyers refrained from bulk procurement during the Dussehra and Durga Puja holidays.

Price movements, trades

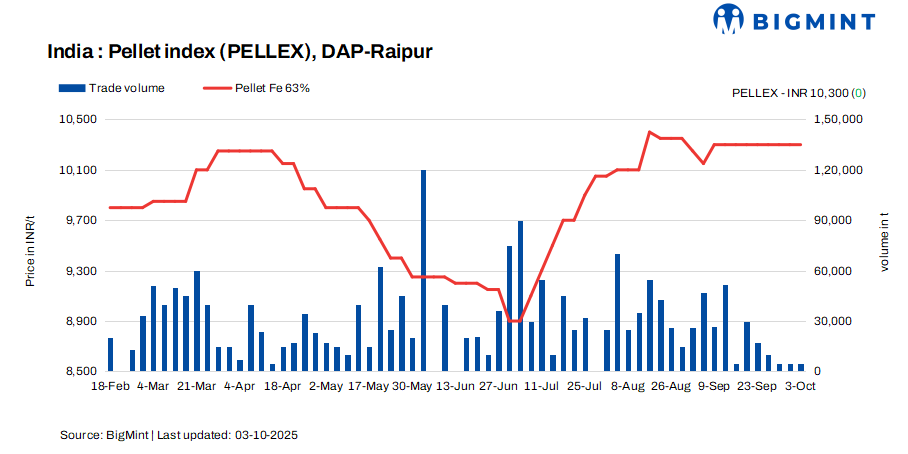

PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained stable at INR 10,300/t ($116/t) DAP on 3 October 2025 compared to the previous assessment on 30 September. Deals for around 5,000 t were recorded in the Raipur market in the last couple of days.

Raipur-based pellet producers kept their offers for Fe 63/63.5% (+/-0.5%) material stable at INR 10,200-10,500/t ($115-118/t) exw recently. Meanwhile, a few plants hiked their offers, though no deals were concluded.

Some Odisha-based suppliers offered pellets at INR 9,800-10,400/t ($110-117/t) DAP Raipur, but buyers remained cautious and deals were absent.

Market scenario

Market participants reported that only need-based inquiries were heard in the region, while sellers kept their offers unchanged. A supplier said, “There is hardly any bulk movement in the market right now. Buyers are approaching only for small-quantity requirements, which is keeping overall activity limited.”

Adding to the cautious sentiment, several participants are waiting for the announcement of NMDC’s iron ore prices for October, which are yet to be declared. A steelmaker informed, “NMDC’s prices will set the tone for pellet demand in the coming weeks.”

Meanwhile, sponge iron and semi-finished steel prices have remained under pressure, further impacting pellet demand. A Raipur-based steel producer noted, “With sponge and billet prices weakening, mills are hesitant to take large positions. Most are only buying as per immediate production needs.”

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- One (1) deal was reported in this publishing window, which was not taken for calculation. Thus, the T1 trade category was accorded 0% weightage.

- Nineteen (19) firm offers, bids, and indicative prices were heard. Fifteen (15) were taken for price calculation and given a balance of 100% weightage.

Key market drivers

- Sponge iron tags down w-o-w: P-DRI prices declined by INR 500/t ($6/t) w-o-w to INR 24,000/t ($270/t) exw-Raipur on 3 October while falling by INR 100/t ($1/t) d-o-d. Inventory buildup was largely avoided, as participants continued to anticipate further price corrections. Additionally, continued weakness in downstream steel segments added pressure on sponge iron prices, reinforcing a cautious outlook and limiting prospects for any short-term recovery.

- Billet prices drop w-o-w: Billet prices in Raipur decreased by INR 550/t ($6/t) w-o-w to INR 36,050/t ($406/t) exw today. Prices fell by INR 150/t ($2/t) d-o-d. Trading was largely confined to need-based procurement, with only a handful of spot deals reported. Continuous weakness in finished steel demand compelled sellers to reduce offers in the semi-finished steel segment to attract buying.

Outlook

Stable pellet prices are providing temporary support, but limited demand and downstream weakness continue to weigh on market outlook. Market participants expect pellet prices to remain volatile in the near term, with a lot depending on NMDC’s October prices.

Leave a Reply