- NMDC raises iron ore prices for August deliveries

- PDRI, billet prices fall by INR 600-800/t w-o-w

Pellet prices in the Raipur region remained firm this week despite mixed market sentiments. The recent hike in iron ore prices by NMDC for August deliveries prompted pellet producers to maintain their offers, even as demand from sponge iron and steelmakers softened due to a sharp decline in sponge iron and semi-finished steel prices observed today.

Price movements, trades

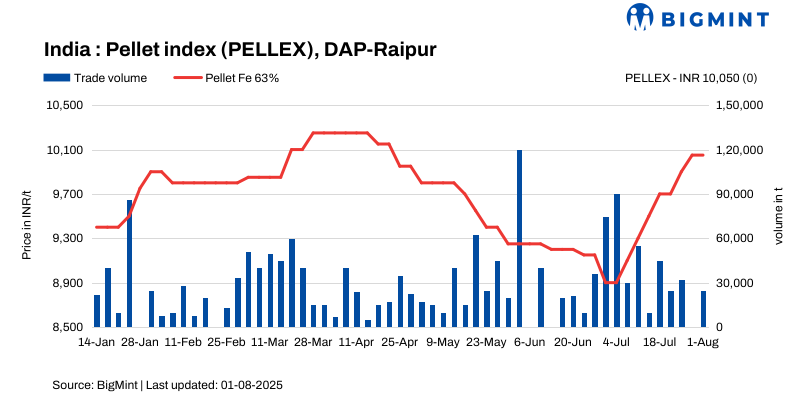

PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained stable at INR 10,050/t ($115/t) DAP on 1 August 2025 compared to the previous assessment on 29 July.

Raipur-based pellet producers maintained their offers for Fe 63% (+/-0.5%) material stable, at INR 9,900-10,000/t ($114-115/t) exw. Deals for around 25,000 t of pellets were concluded in the last couple of days by local pellet suppliers.

Pellet (Fe 62.5-63%) offers from Odisha for Raipur were heard at INR 9,700-10,200/t ($111-117/t) DAP.

NMDC increased its list prices of iron ore calibrated lump ore (CLO) and fines for August deliveries today, BigMint learnt from sources. The miner fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 6,850/t ($78/t) and of iron ore fines (-10 mm, Fe 64%) at INR 5,250/t ($60/t), an increase of INR 450/t ($5/t) and 400/t ($4.5/t), respectively. Prices are on FOR basis from the miner’s Bacheli complex and include royalty, DMF, and NMET.

Market scenario

Pellet buying interest was moderate, with local buyers making purchases only on a need basis. A supplier from the Raipur region stated, “We are witnessing selective demand. Buyers are cautious due to falling steel prices and are waiting for clarity before placing bulk orders.”

The downstream steel market remained under pressure, which impacted overall demand. A sponge iron manufacturer stated, “Only urgent buying is happening. With the current sponge iron and steel prices, pellet buying is not viable for us in bulk.”

Adding to the cautious sentiment, heavy rainfall in mining regions disrupted raw material availability. These supply-side concerns further supported pellet producers’ decision to keep their prices firm. A pellet supplier noted, “We will wait for the next round of orders at current levels.”

Additionally, pellet deals from Odisha suppliers to Raipur buyers were subdued, reflecting weak inter-regional trade flows under current market conditions.

Market participants expect pellet prices to remain range-bound, with more clarity likely to emerge next week, depending on steel market trends and supply movements.

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- Two (2) deals were reported in this publishing window and were taken for calculation. Thus, the T1 trade category was accorded 50% weightage.

- Fourteen (14) firm offers, bids, and indicative prices were heard. Thirteen (13) were taken for price calculation and given a balance of 50% weightage.

Key market drivers

- Sponge iron tags fall w-o-w: P-DRI prices declined by INR 800/t ($9/t) w-o-w to INR 24,650/t ($283/t) exw-Raipur on 1 August. Meanwhile, prices inched up by INR 50/t ($0.5/t) d-o-d today. This price uptick was primarily due to a recent hike of INR 450/t in iron ore prices by NMDC, which raised sponge iron production costs. In response, manufacturers adopted a firmer pricing stance, even as demand from the finished steel segment remained weak.

- Billet prices drop w-o-w: Billet prices in Raipur decreased by INR 600/t ($7/t) w-o-w to INR 37,550/t ($431/t) exw today while rising INR 150/t ($2/t) d-o-d. Market sentiment was cautiously optimistic, with participants closely monitoring further movements in raw material prices and regional supply-demand dynamics.

Outlook

Pellet prices are likely to remain volatile, with more clarity on the accepted trading levels expected in the next week. Buying interest will remain subdued for the next couple of days amid weaker market dynamics.

Leave a Reply