- Slight increase seen in sponge iron prices

- Billet, rebar demand sustains, supports scrap

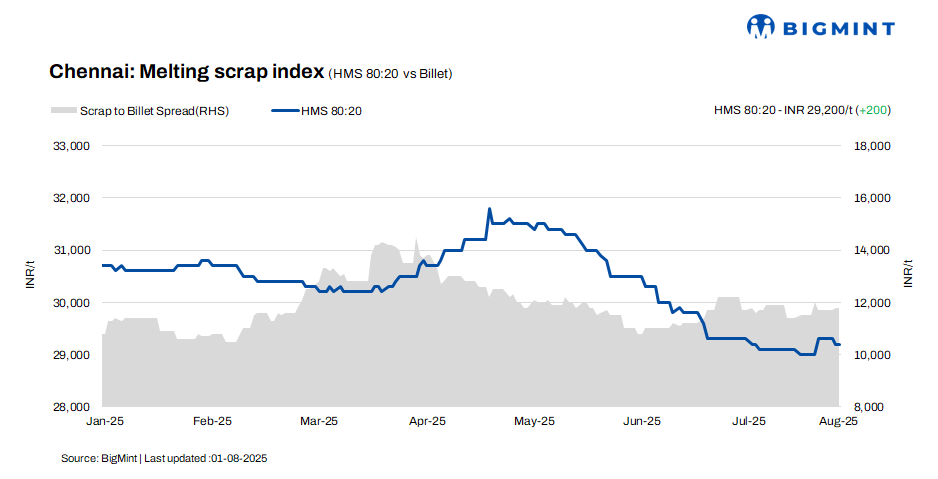

HMS (80:20) scrap prices in Chennai rose by INR 200/t on a w-o-w basis, reaching INR 29,200/t, as per BigMint’s latest data. Despite this weekly gain, prices held steady d-o-d. Meanwhile, billet and rebar prices remained unchanged both daily and weekly, with offers assessed at INR 41,000/t and INR 45,500/t, respectively. The modest rise in HMS scrap reflects localised buying interest, but overall market sentiment remains steady with unchanged billet and rebar prices.

Imported, domestic price trends

According to a scrap trader, shredded scrap from Australia is currently being offered at $365-370/t CFR Chennai, while HMS (80:20) is quoted at $345-350/t. However, bids have weakened by $5-10/t, indicating a cautious market sentiment. Additionally, market sources report that 2-3 vessels carrying scrap are expected to be beached at Chennai Port around the 10th of this month.

Prices of domestic HMS (80:20) were in the range of INR 29,000-29,500/t for buyers settling deals with immediate payment. For transactions involving extended credit terms, prices were higher, at INR 29,500-30,000/t. Most offers were concentrated within the INR 29,000-30,000/t range, with the majority of deals being concluded at these levels, indicating a stable market.

Buyer-supplier sentiments

A mill official informed BigMint that sponge iron offers have shown a slight uptick, driven by limited merchant market participation from mills. Meanwhile, average demand levels for billet and rebar are sustaining price stability, reinforcing a firm pricing outlook across these product categories. Limited sponge iron availability and steady demand for billet and rebar are maintaining firmness in market offers.

A market representative informed BigMint that HMS (80:20) scrap was traded in the range of INR 29,000-30,000/t, with price realizations varying based on payment terms. Mills have marginally raised scrap purchase prices, encouraged by mild improvements in other regional markets. However, liquidity challenges persist, with current scrap payment cycles ranging between 7 to 10 days. Slight uptick in scrap buying reflects improved sentiment in key regions, though liquidity constraints continue to delay payments.

Regional comparison

The Jalna steel market remains largely stable, with billet and HMS (80:20) scrap assessed at INR 39,800/t and INR 30,700/t, respectively. Rebar prices saw a marginal rise of INR 200/t, reaching INR 43,700/t. Overall sentiment is steady, supported by moderate trade activity, while scrap inflows into mills continue to align well with production needs, sustaining price stability.

Outlook

Sources suggest that scrap prices are expected to remain range-bound in the near term, with possible fluctuations limited to INR +/-500/t. This stability is largely attributed to prevailing uncertainty in the finished steel market, where both buyers and sellers are adopting a cautious stance. As a result, price volatility is likely to remain subdued within a narrow band.

Leave a Reply