- Sellers initially reduce offers amid cautious buying but raise them later

- Surge in sponge iron, billet prices on Monday limits sharper drop

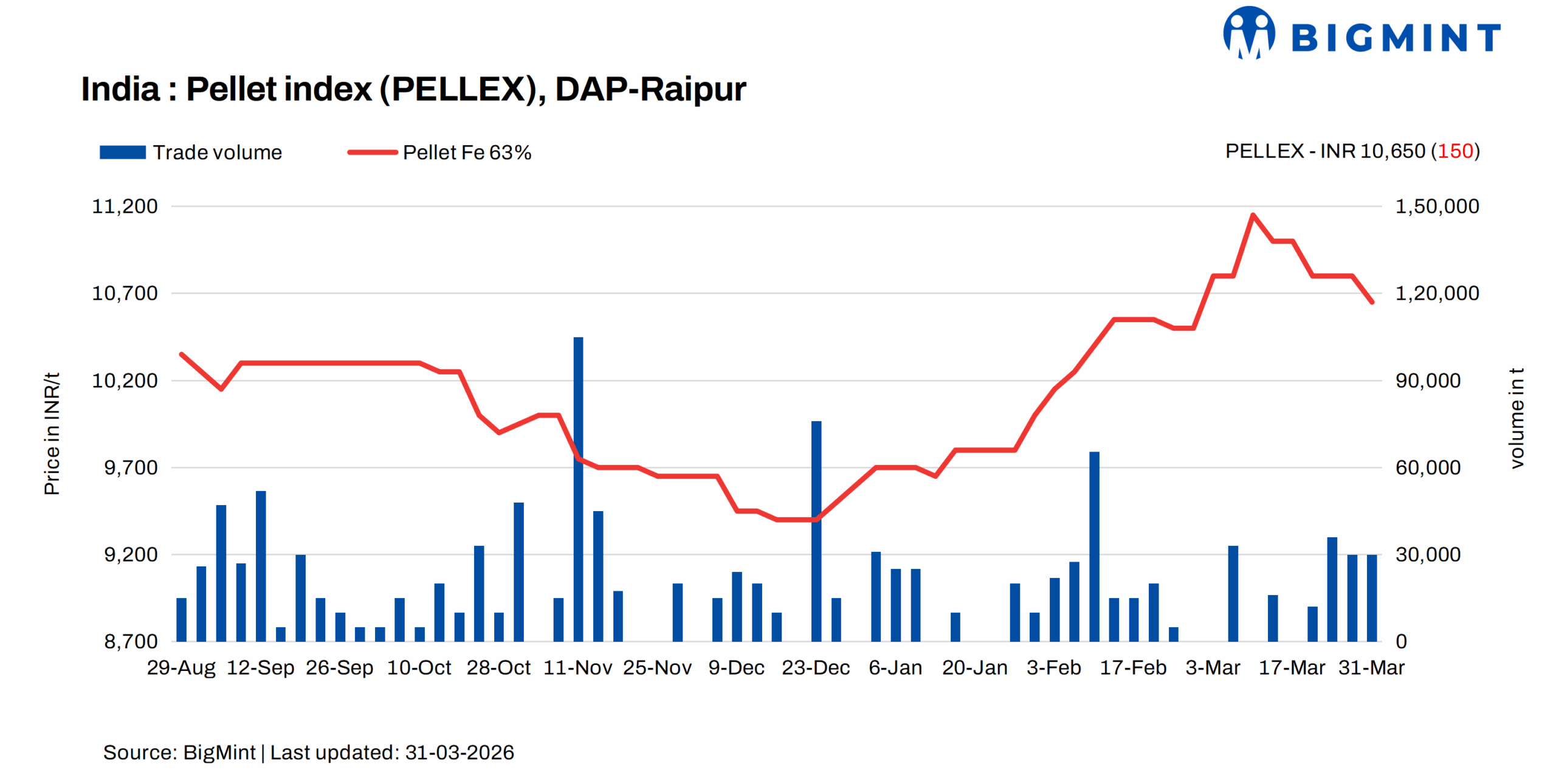

Pellet prices in the Raipur region fell by INR 100-200/t on 31 March compared to the previous assessment, as buyers concluded deals on need basis ahead of the fiscal year-end. The price correction occurred despite a marked improvement in the buying interest from the weekend, which led to some active deals concluded by steelmakers. A sharp single-day uptick in sponge iron (+INR 1,250/t) and billet (+INR 1,550/t) prices on 30 March lifted sentiment earlier in the week.

Trades and price movements

PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur declined by INR 150/t ($2/t) INR 10,650/t ($113/t) DAP on 31 March, Tuesday, compared to 27 March, Friday, reflecting softer market conditions. BigMint recorded deals for around 30,000 t concluded at INR 10,300-10,600/t exw Raipur by local pellet producers.

Offers for Fe 62.5-63% (+/-0.5%) grade pellets were heard lower at INR 10,500-10,600/t ($112-113/t) exw Raipur, translating to around INR 10,600-10,700/t DAP.

Market dynamics

Market dynamics in the region were volatile over the past week. Raipur-based pellet producers had reduced their offers by around INR 300/t during the previous weekend, citing weak demand and subdued market sentiment. However, offers were increased by about INR 200/t following the sudden rise in semi-finished steel prices.

Market participants highlighted that, initially, procurement activity was strictly need-based, with most plants refraining from aggressive or bulk bookings. “We are only lifting material as per immediate requirements. There is no urgency to build inventory at current prices,” said a Raipur-based sponge iron manufacturer.

However, following the uptick in sponge iron and billet demand, which was largely driven by buyers from west India, pellet demad improved. A trader noted, “Scrap shortages and increased gas prices have pushed buyers towards sponge-based production, which indirectly supported pellet demand.” This shift helped improve liquidity in the pellet market, leading to the conclusion of some spot deals.

Pellet producers also highlighted improved sales volumes after a relatively dull period. “We have managed to sell decent quantities over the past 2-3 days, especially after witnessing limited deal activity in the last two weeks,” a Raipur-based producer said.

Among buyers too, sentiment turned slightly optimistic. A steelmaker commented, “The rise in downstream steel prices has encouraged procurement, as margins have improved marginally.”

However, inter-regional trade was limited. Odisha’s pellet prices were heard to be unviable for Raipur buyers, and no significant deals were recorded from neighbouring markets.

Going forward, market participants expect some clarity in the coming days, although activity may remain subdued in the initial phase of the new financial year.

Rationale

- PELLEX has been derived using data points, i.e., trades, offers, and bids. To download the detailed methodology, click here.

- Five (5) deals were recorded in this publishing window, and three (3) were taken for calculation. Thus, the T1 trade category was accorded 50% weightage.

- Eleven (11) firm offers, bids, and indicative prices were heard, and nine (9) were taken for price calculation and given the balance 50% weightage.

Key market drivers

- Sponge iron prices surge w-o-w: Sponge PDRI prices rose by INR 1,050/t ($11/t) w-o-w to INR 26,800/t ($285/t) exw Raipur, reflecting firm market momentum. Despite the sharp rise, trade activity was stable and did not rise sharply, with buyers adopting a disciplined and need-based procurement approach amid elevated price levels.

- Billet prices rise w-o-w: BigMint’s billet index in Raipur lifted by INR 950/t 9$10/t) w-o-w; however, amid slower response from buyers, prices dropped by INR 550/t ($6/t) d-o-d to INR 41,800/t ($445/t) ex-works on 31 March. The substantial w-o-w price hike was supported by improved bookings and firm demand from neighbouring regions. Market participants highlighted that rising coal and scrap prices, along with increased freight and handling charges, significantly elevated production costs, compelling mills to revise offers upward.

Outlook

Prices will remain steady in the upcoming week, with buying expected to pick up as operations normalise at the start of the next fiscal year.

Leave a Reply