- Australia-India remains the only active lane

- Drop in bunker costs weigh on SA & Indonesia-India rates

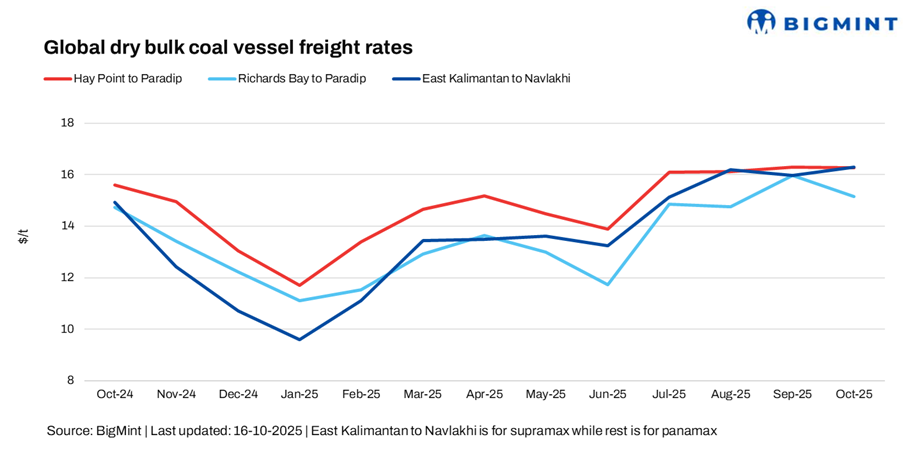

Dry bulk coal freight rates continued to reflect a mixed performance this week amid ongoing market uncertainty and limited trading momentum. The Indonesia-India route saw a slight decline, driven by muted cargo demand and a lack of active fixtures. Meanwhile, the South Africa-India route remained unchanged, with chartering activity subdued as market participants adopted a wait-and-see approach. Overall, sentiment across the market stayed cautious, with weak fundamentals and restrained buying interest keeping freight levels under pressure.

In contrast, a source said, “Australia-India coal freight rates increased this week, primarily supported by renewed spot demand from Indian steelmakers, particularly SAIL, which returned to the market with fresh inquiries and fixtures after a period of limited activity. The rise was further underpinned by tighter vessel availability in the Pacific, as tonnage supply thinned amid ongoing repositioning and selective chartering by owners seeking higher returns. Although overall market sentiment remains cautious, the surge in short-term demand and constrained vessel supply helped lift freight rates on the route.”

Freight rates on the South Africa-India route remained stable w-o-w, as the market continued to face a lack of fresh coal cargo inquiries from the region. The absence of new orders kept trading activity muted. Charterers largely stayed on the sidelines amid uncertain demand outlook and steady vessel availability in the region. As a result, the route saw limited rate movement, reflecting a balanced but inactive market environment.

Meanwhile, Asia-Pacific Supramax freight rates on the Indonesia-India route continued to head south, influenced by a decline in bunker prices. Market activity out of the Indian Ocean remained sluggish, with limited fresh inquiries and a generally flat sentiment prevailing across most lanes.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up by around 1.07/dry metric tonne (dmt) to $17.10/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route remained unchanged at $14.72/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $16.19/dmt, a w-o-w decrease of $0.06/dmt.

Meanwhile, Brent crude oil futures decreased significantly by around $3.52/barrel (bbl) w-o-w to $61.95/bbl. Brent crude futures dropped sharply due to concerns over global oversupply and weaker demand prospects amid economic slowdown fears, especially from U.S.–China trade tensions.

Outlook

In the near term, dry bulk coal freight rates to India are expected to stay supported, underpinned by steady import demand from power utilities and industrial buyers. Increased coal-based power generation amid high electricity consumption and ongoing restocking activity should keep tonnage demand firm, particularly on Australia-India routes. Limited vessel availability in the Indian Ocean could further lend support to Supramax and Panamax segments.

However, freight gains may be capped by easing bunker prices, and the availability of ballasters from other regions. Overall, the market is likely to remain range-bound with a slight upward bias, driven more by regional demand patterns and weather-related disruptions than by broad-based global strength.

Leave a Reply