- New offers awaited in the market, new mines may improve material availability

- Drop in pellet and semi-finished prices keep market tight w-o-w

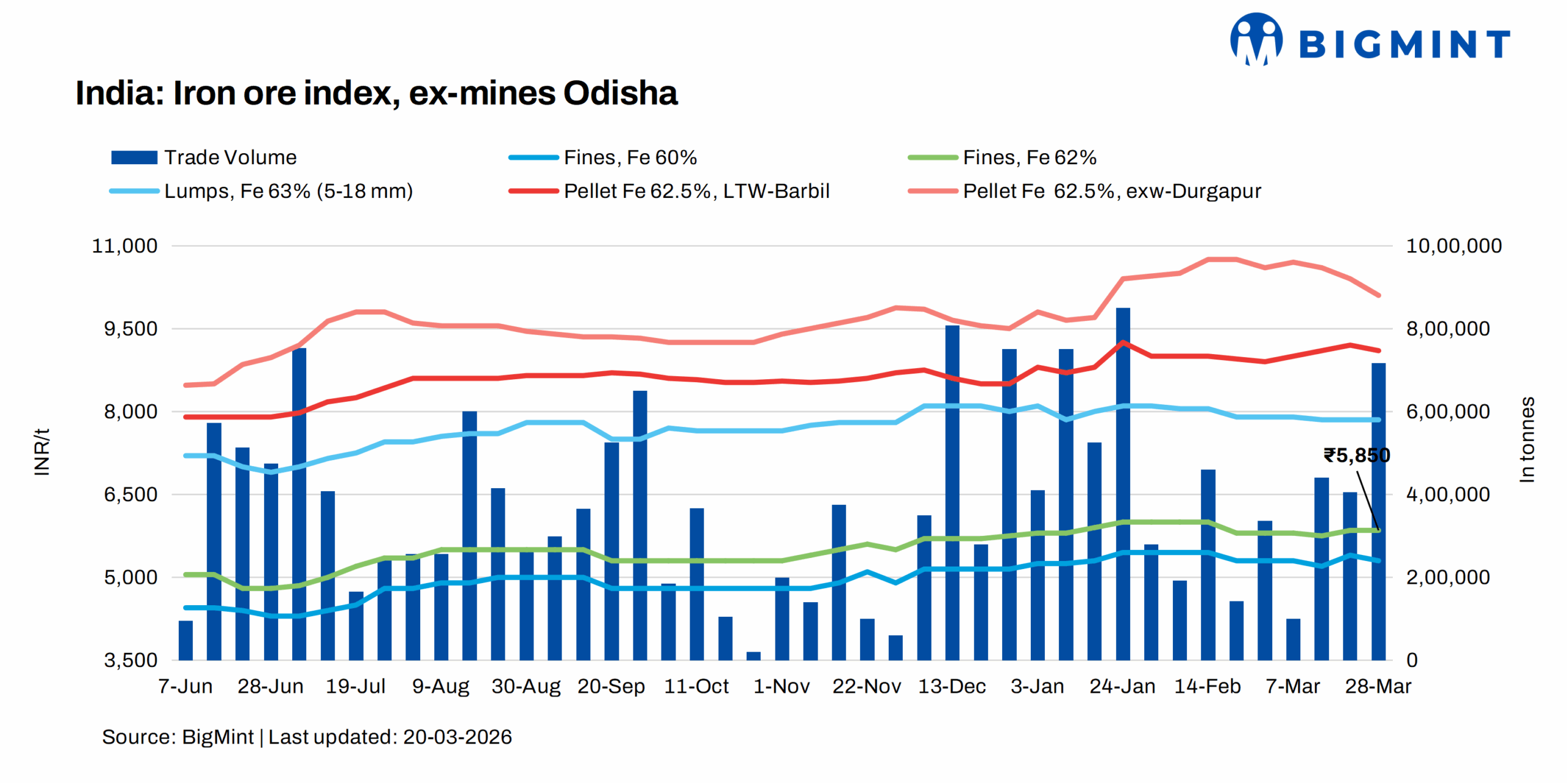

Iron ore prices in the Odisha region remained largely unchanged in the week ended 28 March, supported by a handful of bulk transactions concluded toward the end of the fiscal year. Market participants noted that while trading activity persisted, sentiment remained cautious amid mixed signals from the downstream steel market.

Price update

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,850/t ($63/t) ex-mines on Saturday (28 March). It recorded deals for around 720,000 t this week, concluded directly by steelmakers with private miners and traders. Few more deals were under negotiation, but buyers are waiting for new offers to get a slight ease in the prices for the April liftings of material.

Additionally, SAIL sold around 150,000 tons of iron ore from its Bolani, Barsua, and Kalta mines this week.

Market highlights

The market experienced slight pressure due to a decline in pellet, sponge iron, and semi-finished steel prices. However, deal levels continued to fluctuate, largely depending on the availability of material and immediate procurement requirements. A trader informed, “Transactions are happening, but pricing is not firm. It varies lot-to-lot depending on urgency and supply position.”

Miners indicated a temporary pause in fresh offers, with many awaiting revised Environmental Clearance (EC) limits expected next week. A miner noted, “We are holding back offers for now. With the new EC limits coming in, production visibility will improve, and we will revise prices accordingly. However, a few miners have already accepted orders for April delivery, indicating selective participation in the market.”

Steelmakers, on the other hand, expect some price correction in the near term. A prominent buyer commented, “Prices should see relaxation as supply normalises post EC revisions. Availability will improve, reducing the current tightness.”

The supply outlook is also set to improve with the entry of newly auctioned mines. Market sources have highlighted that new miners, such as Anandam Minerals and Dee Vee Projects, are expected to introduce fresh offers soon. Additionally, several existing mines have received expansion in their EC limits, which will further enhance production capacity in the region.

On the operational front, Sirajuddin Mines has resumed dispatches, with initial deals already reported by buyers. This has added to the supply-side optimism.

Meanwhile, auction activity remained active. SAIL concluded a few auctions this week, while upcoming auctions from JSW and AMNS are expected to provide further direction to market prices.

Factors affecting iron ore prices

Pellet prices show mixed trend: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil decreased by INR 150/t w-o-w to INR 9,000/t ($95/t) loaded to wagon on 27 March. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur fell by INR 300/t to INR 10,100/t ($106/t) exw.

Sponge iron prices drop w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela decreased by INR 600/t ($5/t) w-o-w to INR 27,000/t ($295/t) on 28 March.

Billet prices down w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela also dropped by INR 450/t ($4/t) w-o-w to INR 39,900/t ($421/t) on 28 March.

Rationale

- T1- Six (6) deals for Fe 62% fines were recorded in the publishing window, and five (5) were considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received sixteen (16) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Sixteen (16) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

According to BigMint analysis, Odisha iron ore prices are likely to soften in the near term, primarily due to increased supply from revised EC limits and fresh participation from new miners.

Leave a Reply