- HRC trade prices decline INR 900/t m-o-m in Jun’25

- High stocks, tepid demand may further drive down prices

Indian steel producers have maintained list prices for hot-rolled coils (HRCs) and cold-rolled coils (CRCs) for July 2025 sales. While most mills officially held prices steady, market participants suggest price support or reduction of INR 1,000-2,000/tonne (t) ($12-23/t).

List prices of HRCs (2.5-8 mm, IS2062, Gr E250 Br) ranged within INR 52,150-54,000/t ($611-633/t) ex-Mumbai. CRCs (0.9 mm, IS513 CR1) were listed at INR 57,650-60,750/t ($675-712/t). Newer entrants offered HRCs slightly cheaper, at INR 51,900-52,000/t ($608-609/t).

The price stability could be attributed to the continued soft demand in the past few weeks.

Market scenario

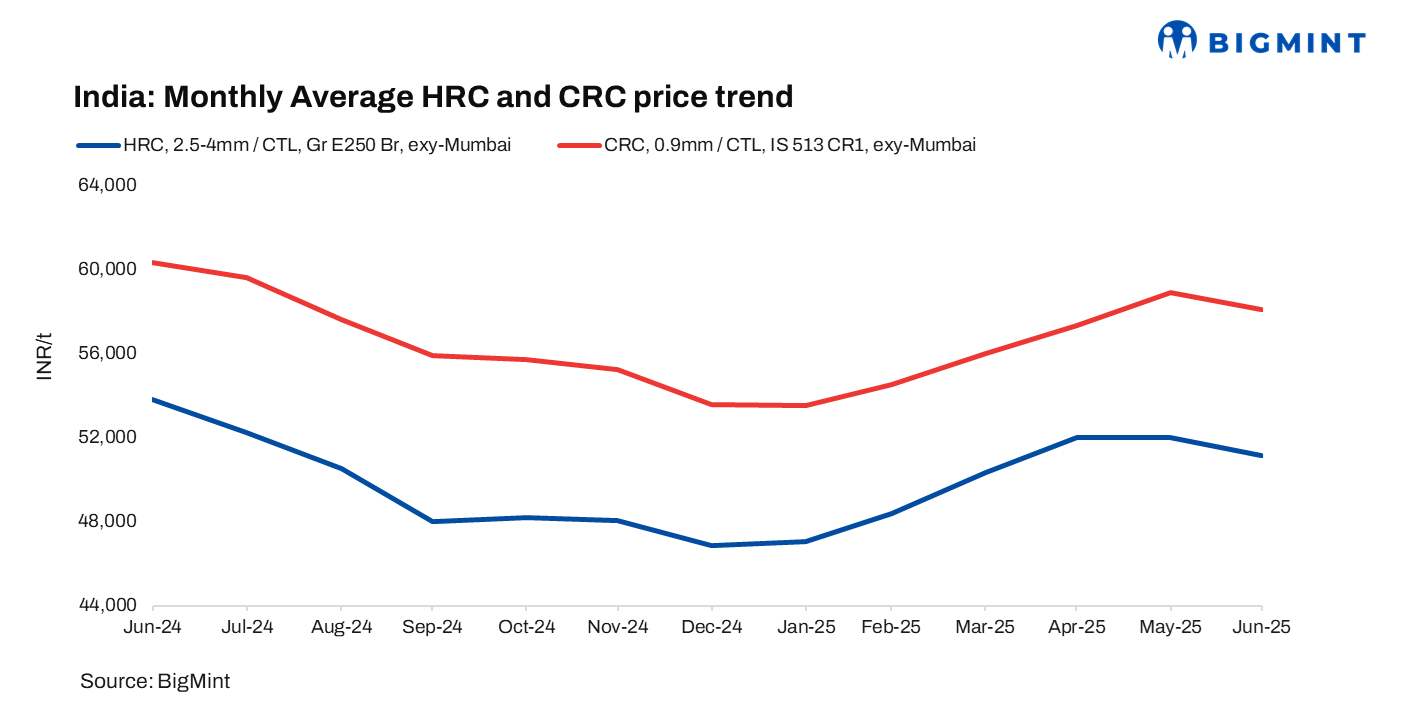

Domestic trade prices decrease m-o-m: In June 2025, average trade-level HRC prices fell by INR 900/t ($11/t) m-o-m to INR 51,100/t ($599/t), while CRC prices declined by INR 800/t ($9/t) to INR 58,100/t ($681/t), both exy-Mumbai and excluding 18% GST.

Domestic demand was need-based amid continued price resistance. Buyers pushed for lower rates, expecting further cuts, and delayed purchases. Sellers aimed to clear inventories before the quarter-end, but distributors limited price cuts, as trade rates were already well below mills’ list prices, and they did not receive support from mills.

Import trends: India’s bulk imports of HRCs touched 3,22,329 t as of June, based on vessel line-up data from BigMint. However, a slight uptick m-o-m was observed, given that May recorded 279,250 t and in April 2025 it was 2,72,258 t of HRCs. Moreover, 159,825 t of cargo are expected in July.

Export scenario: India’s bulk HRC exports stood at 1,38,868 t in June, down from 1,44,093 t in May, according to vessel line-up data from BigMint.

India’s HRC export offers to the EU dropped $26/t m-o-m to $565/t FOB in June. European prices remained weak due to poor demand, high inventories, and a summer slowdown. Despite lower offers, buyers stayed cautious amid sluggish automotive and construction demand. Indian mills prioritised the domestic market, where price realisations were stronger, and limited offers to the Middle East.

Outlook

In the near term, Indian HRC and CRC prices are likely to face mild downward pressure. While mills have kept list prices unchanged for July, limited demand, elevated inventories, and buyers’ expectations of further corrections may drive trade-level prices down. Export activity remains subdued due to weak EU demand, while imports remain moderate, reinforcing a cautious pricing outlook.

Leave a Reply