- Interest in imported scrap limited by ample domestic supply

- Finished demand stays moderate, mills liquidate 50% of stock

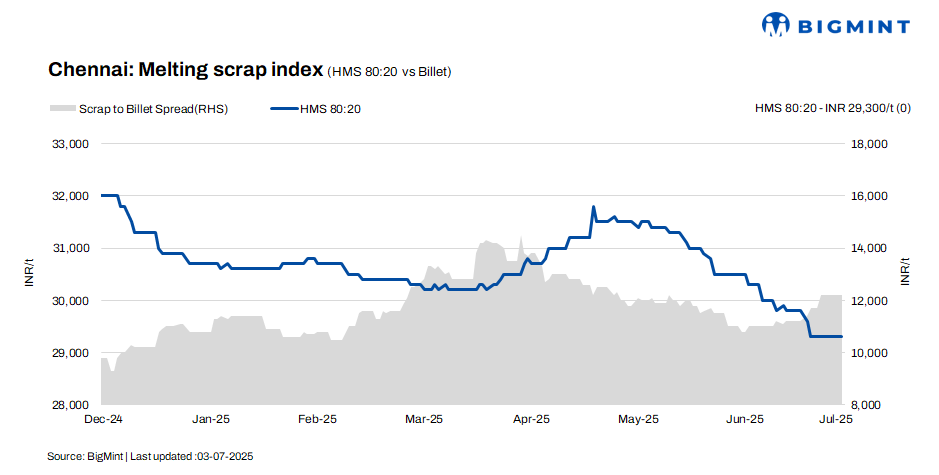

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai remained stable at INR 29,300/tonne (t), with no changes observed on a d-o-d or w-o-w basis. Similarly, rebar prices held steady at INR 46,000/t in both d-o-d and w-o-w evaluations. Billet prices saw an increase of INR 500/t w-o-w, now at INR 41,500/t, while remaining stable d-o-d. Market activity indicates a mixed trend, with stability in daily pricing and minor fluctuations over the week.

Imported, domestic price trends

According to a scrap trader, shredded from Australia was offered at $355-360/t CFR Chennai, with HMS (80:20) priced in the $335-340/t range. However, mills showed limited interest in imported scrap, as domestic material was not only competitively priced but also readily available.

Prices of domestic HMS (80:20) were in the range of INR 29,000-29,500/t for buyers settling deals within seven days. For transactions involving extended credit terms, prices were higher, at INR 29,500-30,000/t. Most offers were concentrated within the INR 29,000-30,000/t range, with the majority of deals being concluded at these levels, indicating a stable market.

Buyer-supplier sentiments

A mill representative informed BigMint that semis prices remained well-supported, with merchant sellers holding one week’s worth of bookings and prioritising deliveries over new sales. Finished steel demand was moderate, and mills strategically liquidated up to 50% of their stock through discounted pricing to manage working capital. Sponge iron pricing remained unchanged, with sellers holding back material due to resistance against low-priced deals.

According to a local scrap supplier, HMS (80:20) scrap was traded in the domestic market at INR 31,000-32,000/t, with minor price variations influenced by payment terms. Given the current steady flow of supply, the market does not foresee any major price softening in the short term, reflecting a stable outlook for scrap procurement strategies.

Regional comparison

The Jalna steel market continued to show d-o-d stability, with rebar and HMS (80:20) scrap assessed at INR 43,500/t and INR 30,600/t, respectively. Billet prices edged down by INR 200/t d-o-d to INR 39,000/t. Market sentiment was steady, supported by moderate trade volumes. Scrap inflows into mills were well-aligned with production requirements, reinforcing stable supply dynamics at existing price points.

Outlook

According to sources, scrap prices are expected to remain range-bound in the near term, with possible fluctuations limited to INR +/-500/t. This stability is largely attributed to continued uncertainty in the finished steel market, where both buyers and sellers are exercising caution. As a result, the current market sentiment is likely to restrict volatility and maintain pricing within a narrow range.

Leave a Reply