- Safeguard duty proposal lends support to list prices

- Trade-level prices rally for five weeks in succession

Major coated flat steel producers have announced an increase of INR 2,000-3,000/tonne ($23-35/t) in their list prices for April 2025 dispatches, effective 1 April. Whereas the quantum of increase has been INR 2,000-2,500/t ($23-29/t) in galvanised plain (GP) coils, it is higher- around INR 2,500-3,000/t ($29-35/t)- for pre-painted galvanised iron (PPGI) coils.

The effective list prices of GP (0.8mm, 80gsm, IS277) stands at around INR 63,500-63,600/t ($741-742/t) ex-Mumbai, while those for PPGI (0.5mm, 90gsm, IS14246) are around INR 73,500-73,750/t ($858-861/t) ex-Mumbai for early April dispatches. Prices mentioned are for coil forms, excluding GST at 18%.

Safeguard duty: The recommendation of a safeguard duty boosted sentiments in the distribution channel. The Directorate General of Trade Remedies (DGTR) recommended the imposition of a 12% safeguard duty for 200 days on finished flat steel imports on 19 March. Thus, any finished flat steel product imported below the threshold prices mentioned in a gazette notification would attract a duty of 12%. The threshold price for zinc-coated flat products has been set at $861/t CIF (cost, insurance and freight) India, whereas the threshold price for colour-coated or pre-painted is $964/t CIF India.

It bears recall that a few mills had announced interim price hikes in the second fortnight of March.

Trade prices rise for fifth week in a row: Trade-level prices of coated flat products continued to rise for the fifth week in a row, taking a cue from the hike in list prices by mills.

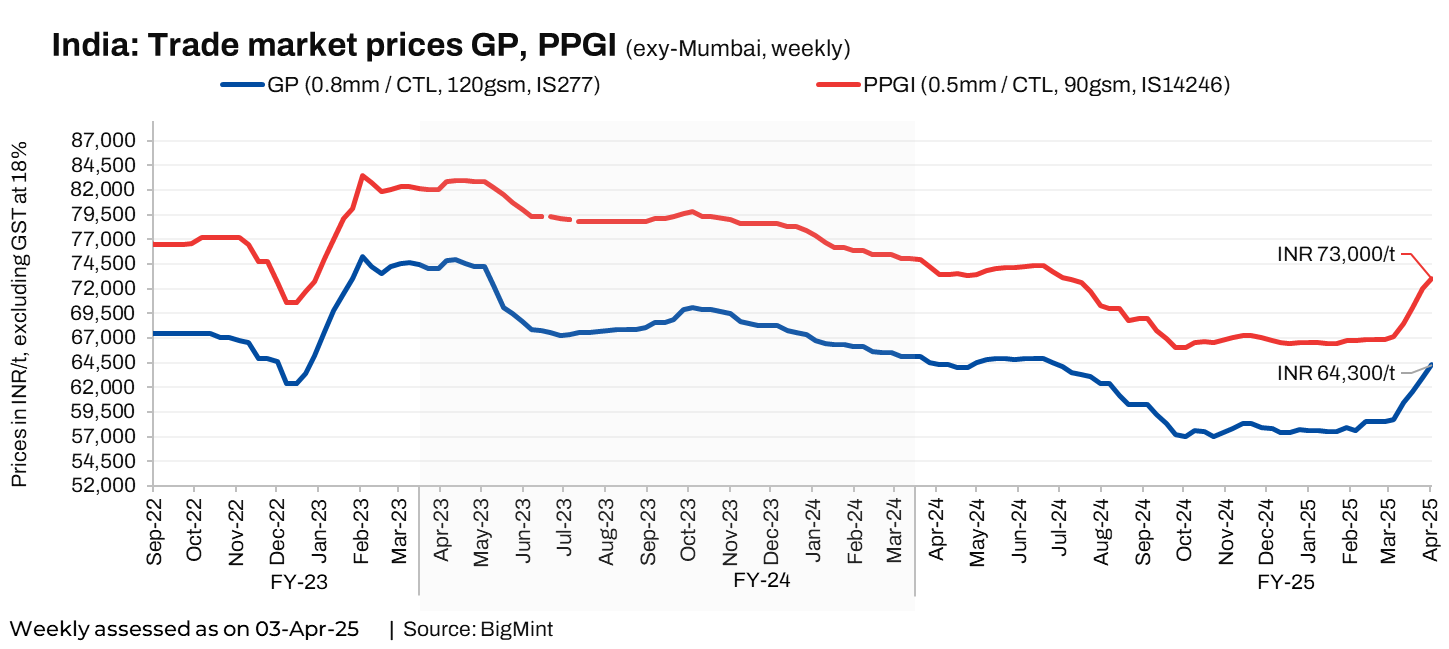

The latest weekly assessment, on 3 April, showed galvanised plain (GP, 0.8 mm/CTL, 120 gsm, IS277) coil prices at INR 64,300/t ($743/t) exy-Mumbai, with offers varying in the range of INR 63,500-65,000/t ($741-758/t). Similarly, pre-painted galvanised iron (PPGI, 0.5 mm/CTL, 90 gsm, IS14246) was assessed at INR 73,000/t ($852/t) exy-Mumbai, with offers at INR 72,500-74,000/t ($846-864/t). These prices are minus GST at 18% (USD 1 = INR 85.2928; INR 1 = USD 0.0117243).

Moreover, the monthly average prices of GP (0.8 mm/CTL, 120 gsm, IS277) have risen by about INR 2,700/t ($32/t) m-o-m to INR 61,000/t ($712/t) in March. Meanwhile, PPGI average tags increased by around INR 2,600/t ($30/t) m-o-m to INR 69,500/t ($811/t) in March. Prices are minus GST at 18%.

Demand-supply dynamics: Supply constraints propelled mills to raise their list prices amid production-related hassles while consumption volumes improved. “Mills had been short-supplying materials to distributors against the requirements raised through purchase orders (PO),” said a major distributor based in western India. Thus, despite a weak demand scenario, distributors are quoting higher.

Meanwhile, the market indices showed improvement in activities in the manufacturing segment, reflecting an increase in consumption levels. For instance, the manufacturing purchasing managers’ index (PMI) increased by 1.8 points to 58.1 in March 2025 as against the previous month. This hints towards mills witnessing improved demand from their business to consumer (B2C) segment sales, where trade market participants have been complaining about need-based demand and low sales.

Production and consumption volumes: The production levels of coated flat products dropped by 6.2% m-o-m to 0.877 mnt in February 2025 compared to 0.935 mnt in January 2025, as per recent data released by the Ministry of Steel. The average daily production computes at around 29,200 tonnes per day (tpd) in February compared to 31,200 tpd in January.

However, consumption increased by around 1.6% m-o-m in February to 0.962 mnt as compared to January’s 0.947 mnt. Out of these volumes, PPGI or the colour-coated coils aggregates to around 0.263 mnt in February and 0.285 mnt in January.

In terms of company-wise performance, SAIL has been the only producer to have produced higher in February, while others fell short of the previous month’s levels.

Outlook:

Trade market prices of coated flats have continued to rise since the beginning of March. However, these are likely to stay rangebound or show a marginal increase in the near term. Meanwhile, supplies are likely to fall short in the distribution network amid indications that some mills might opt for maintenance shutdowns in April, some industry participants informed.

Leave a Reply