- Demand from mills drops amid higher scrap use

- Chinese met coke producers moot 2nd price hike

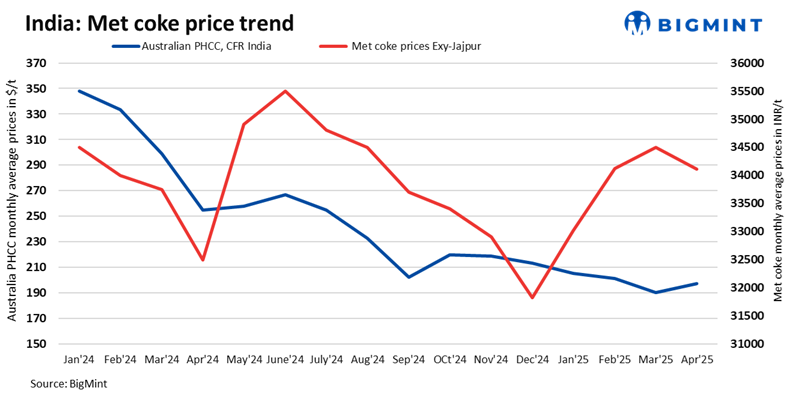

Domestic met coke prices in India showed mixed trends w-o-w amid a drop in pig iron tags and lukewarm demand from the steel sector. In the eastern market’s Jajpur, 25-90 mm BF grade coke prices dropped by INR 450/tonne (t) to INR 33,650/t exw, while tags in Gandhidham remained steady at INR 32,200/t exw.

The decline was also driven by reduced steel production and a shift towards cheaper scrap feedstocks.

Factors contributing to drop in met coke prices

Indian pig iron prices drop sharply: Indian steel-grade pig iron prices in Durgapur fell by INR 1,200/t w-o-w to INR 33,500/t exw, driven by abundant scrap availability, which has reduced the need for pig iron and, in turn, decreased coke consumption.

Demand from steel sector softens: Lower steel production led to reduced need for coke. Steelmakers also turned to scrap for its cost effectiveness, further diminishing coke demand.

Coking coal prices increase slightly: Australian coking coal prices rose marginally by $1/t w-o-w to $191/t FOB Australia. Meanwhile, availability from Australia remained a concern, with a large number of deals being done for Canadian coal.

Chinese met coke prices edge up: Chinese met coke prices rose by RMB 50-55/t for the first time since October 2024, driven by strong molten iron output and pre-holiday restocking. At the same time, Chinese met coke producers proposed a second straight round of price hikes.

Outlook: Weak demand likely to persist

In the short term, domestic coke prices in India are likely to remain under pressure due to persistent weak demand and the decline in pig iron tags. Global factors, such as Australian coking coal prices and Chinese coke trends, will play a supporting role in the days to come.

Leave a Reply