- Post-festive demand lifts project buying

- Billet prices rise by INR 500/t w-o-w

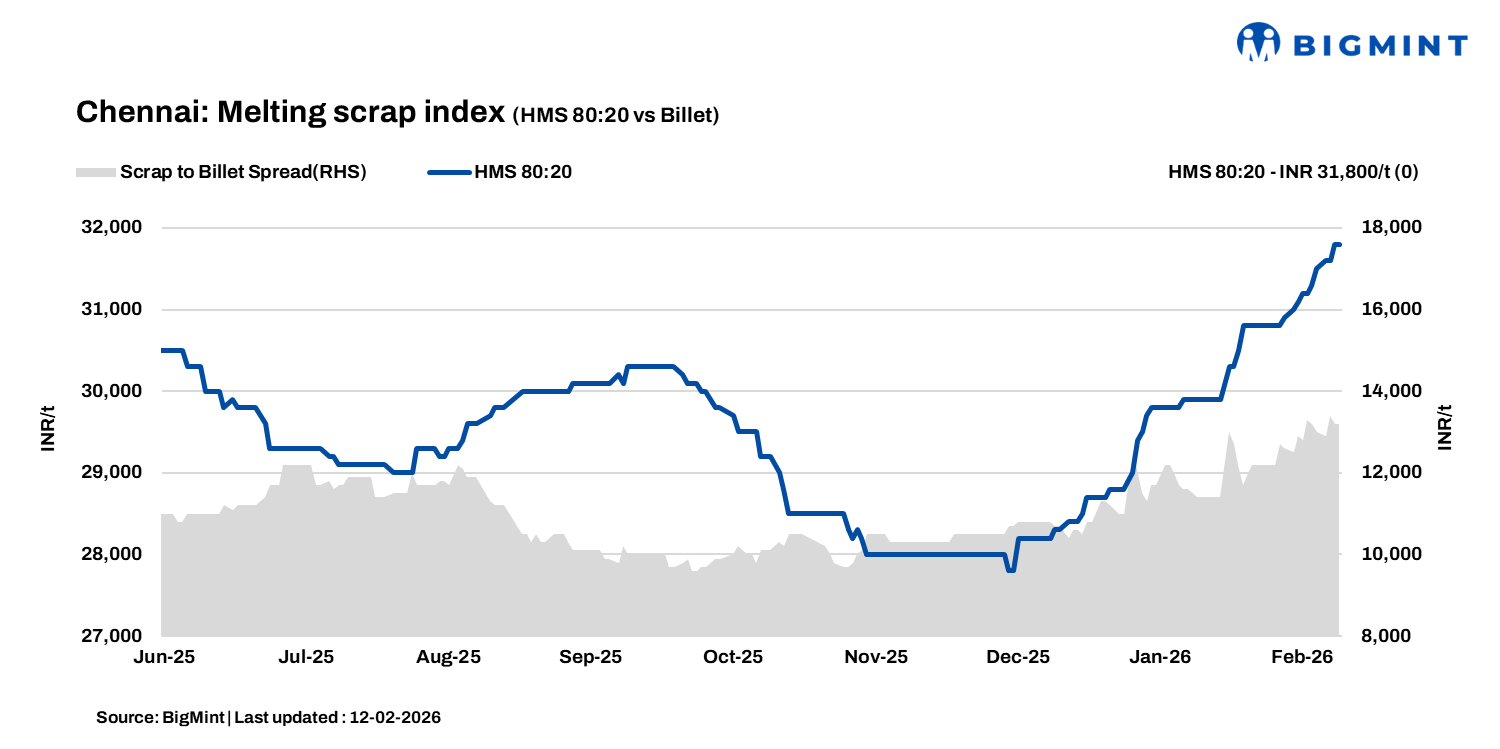

Chennai’s ferrous scrap market strengthened w-o-w, as assessed on 12 February, with HMS (80:20) prices rising by INR 600/t w-o-w to INR 31,800-32,200/t. The uptick followed improved steel offtake after mid-January, as construction activity resumed post the southern festive lull.

Project demand revives after festive slowdown

Market participants reported that project-based steel demand improved notably after the Pongal period, supporting fresh billet bookings. Billet prices increased by INR 500/t w-o-w to INR 45,000-45,200/t exw Chennai, reflecting better restocking from re-rollers and infrastructure-linked buyers.

A secondary mill source stated, “Enquiries from project contractors improved after mid-January, which helped clear finished steel inventories and stabilise billet production.” Rebar prices in the region also increased by INR 1,000/t w-o-w to INR 49,500/t, supported by steady retail demand and a gradual recovery in institutional buying.

Finished steel inventory levels have declined significantly, with mills currently maintaining average inventory levels of 7-10 days compared with 15-20 days previously. The reduction in inventory holding indicates an improvement in underlying demand conditions.

Imported, domestic price trends

Imported ferrous scrap offers from Australia to India remained broadly steady, though buying interest stayed restrained amid a visible bid-offer gap. Shredded scrap was heard at $365-370/t CFR Chennai, while HMS (80:20) was quoted at $340-345/t CFR, with buyers bidding $5-8/t lower, indicating resistance at higher replacement levels.

Indicative offers stood at $345-348/t CFR for HMS (80:20), $355-360/t for HMS 1, $365-370/t for shredded, and $375-380/t for PNS. Market activity remained selective, with approximately 1,500 t of HMS 60:40 booked at $328/t from Costa Rica, reflecting softer levels for lower-grade cargoes.

Market participants noted that export offers from Oceania remain firm due to slow collections; on the other hand, slower trading activity and cautious mill procurement limited upward revisions. Buyers continued to assess finished steel demand and scrap-to-billet spreads before committing to larger volumes.

In the domestic market, HMS (80:20) transactions were largely concluded in the range of INR 31,800-32,300/t, depending on credit terms and mill-specific requirements. Sponge iron prices increased by INR 500/t w-o-w to INR 28,000/t; however, on a d-o-d basis, prices corrected by INR 300/t, reflecting short-term booking adjustments.

Outlook

According to market sources, scrap prices are expected to either remain stable or witness marginal upside in the coming days, supported by recent improvements in prices of other steel products. Any price uptick is likely to be limited to a narrow range of around INR +/- 200-500/t.

Leave a Reply