- Market activity slows due to limited offers

- Exporters wait for better price realizations

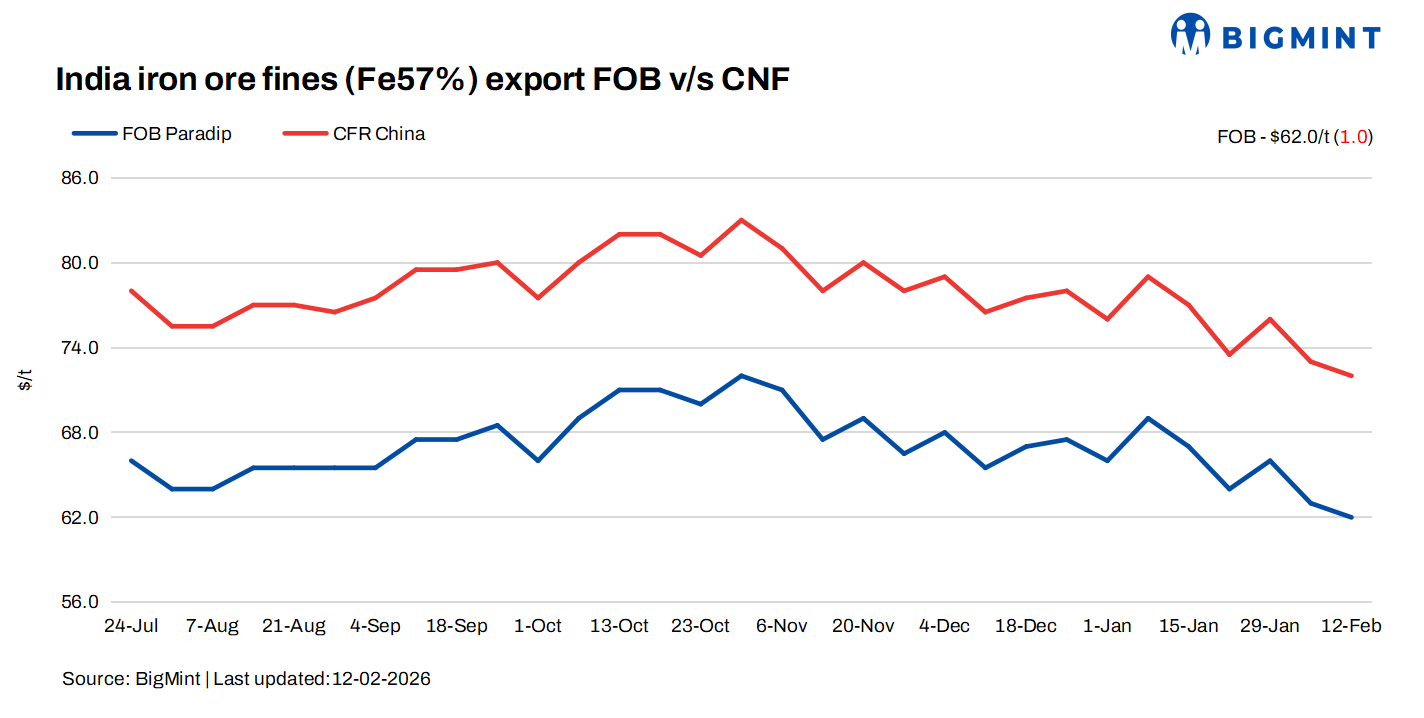

India’s iron ore fines export market remained under pressure this week, with a drop of $1/t, witnessing a bearish trend amid muted buying interest ahead of the upcoming holidays in China. Market participants reported a widening gap between seller expectations and buyer bids, keeping trade activity largely subdued.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices inched down by $1/tonne (t) w-o-w to $62/t FOB east coast on Thursday. Index has hit its lowest since End-Jun’25 with over seven months, as per data maintained with BigMint.

Exporter remained cautious this week amid the downtrend in prices for the seaborne trades. However, BigMint recorded around 115,000 t iron ore export deals in this publishing window, concluded by the east coast miners. BigMint did not record any confirmed export transactions from traders, although a few discussions were heard for March laycan cargoes without closure.

According to sources, the export discount for Fe 57% fines was heard around 21-23%, while discounts for Fe 55% material widened to nearly 26-28% against the global fines index, reflecting continued pressure on lower-grade offerings. The discount on the global fines index remained stable w-o-w.

Market scenario

Exporters indicated that their workable price levels for 57% Fe fines cargo are around $77-78/t CFR China. However, current bids in the seaborne market are hovering at $70-71/t, which exporters consider unviable. An exporter from the East Coast added, “At these bid levels, it is difficult for us to conclude any deals. The margins simply do not support fresh bookings, adding that most sellers are staying away from the market for now.”

Another international trader noted that only miner-origin cargoes are attracting limited bids in the seaborne market, while trader-held material is struggling to find buyers. He said, “With higher port inventories in China and subdued buying interest, traders are reluctant to offload cargo at discounted levels.”

An exporter further highlighted that elevated domestic iron ore sourcing costs in India are restricting aggressive export offers. “If the market does not improve, we may hold back cargo and wait until after the Chinese holidays to receive better price levels,” he informed.

On the demand side, Chinese mills appear cautious as most have completed their pre-holiday restocking. According to a market source, mills are now focusing on cost-effective and cheaper alternatives rather than actively booking Indian low-grade fines.

Meanwhile, east Indian miners are receiving healthy demand from domestic buyers for low-grade material, limiting export availability. However, a few Odisha-based miners reportedly concluded export deals at relatively steeper discounts compared to trader cargoes.

Domestic vs export market

Domestic prices exceeded export realizations by around INR 700/t ($7/t), with the gap being largely stable w-o-w. Iron ore fines (Fe 57%) prices in Odisha were recorded at INR 4,100/t ($45/t) ex-mines, steady w-o-w on 12 February. Meanwhile, the ex-mines realization in exports from the Barbil region fell w-o-w to INR 3400/t (37/t) ex-mines.

Chinese spot prices edge down w-o-w: The benchmark iron ore fines index (Fe 61%) was recorded at $100/t CFR China, down by $2/dmt w-o-w on 11 February. Limited deal-making and sparse offers were observed, as most mills shifted focus toward the upcoming Lunar New Year holiday. Pre-holiday transactions remained selective, although liquidity for non-mainstream low-grade fines continued to be reasonably available.

DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 764/t ($110/t) on 12 February 2026, and remained under pressure w-o-w.

Rationale

- Two (2) deals for Fe 57% was recorded during this publishing window and one (1) was taken under calculations. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received Sixteen (16) indicative prices in the current publishing window, and thirteen (13) were considered for price calculation as T2 inputs and given rest 50% weightage.

Outlook

Export sentiment is likely to remain weak as the Chinese holidays approach. The seaborne market is expected to remain quiet over the next couple of weeks, with prices for lower-grade exports likely to remain rangebound.

Leave a Reply