- Auction participation remains weak

- Buyers remain highly selective

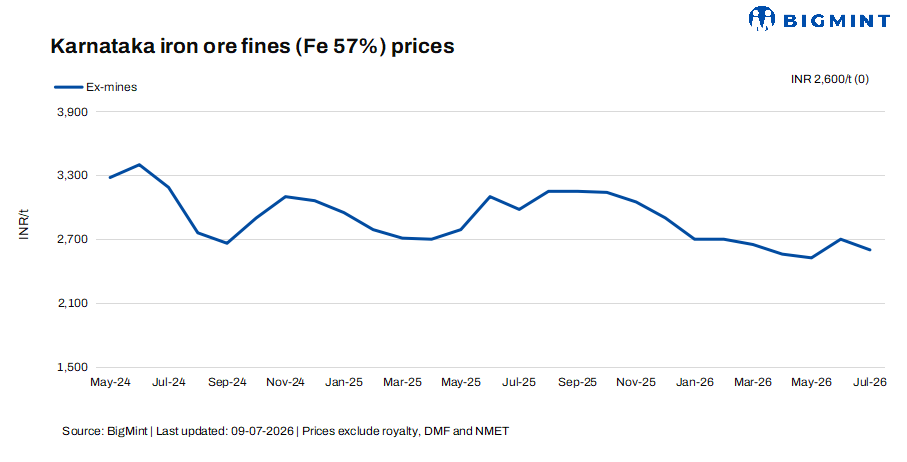

Karnataka’s iron ore market remained largely subdued during the week, with limited trading activity and no significant price movement across major grades. Market sentiment continued to be weighed down by sluggish demand from the sponge iron segment and persistent weakness in the finished steel market, restricting any meaningful recovery in iron ore prices. Most market participants preferred to stay on the sidelines, citing poor downstream offtake and cautious procurement strategies.

According to BigMint’s latest assessment, Fe 57% iron ore fines remained unchanged week-on-week at INR 2,600/t ($27/t) ex-mines. The lower-grade segment continues to face significant pressure as demand remains extremely weak despite ample material availability. Several miners have been actively offering low-grade fines; however, buying interest has remained limited as sponge iron producers continue to operate at reduced capacities or remain shut. The widening demand-supply imbalance has resulted in muted transactions, with buyers purchasing only against immediate requirements.

In contrast, benchmark Fe 62% iron ore fines remained stable at INR 4,900/t ($51/t) ex-mines. Higher-grade material continues to receive relatively better market support due to its limited availability across the state. Market participants noted that only a handful of miners are consistently able to supply premium-grade ore, while the gradual depletion and quality deterioration across several mining leases has further constrained the availability of high-grade fines. As a result, despite the overall weak market environment, prices for higher-grade material have remained resilient, supported by tight supply fundamentals and the absence of significant selling pressure.

Auction activity also remained lacklustre during the week, reflecting the prevailing cautious market sentiment. Only a limited number of miners conducted e-auctions, with a majority of lots either receiving bids at the reserve price or remaining unsold. Buyers continued to adopt a highly selective procurement approach, focusing on established miners and consistent material quality rather than aggressively participating across all auctions. This cautious buying behaviour has further curtailed overall market liquidity and trading volumes. Meanwhile, despite the ongoing monsoon season, rainfall has not yet caused any major disruption to mining operations or ore dispatches across Karnataka.

A Bellary-based miner told BigMint, “The market is currently under significant pressure as the demand-supply imbalance continues to widen, particularly for low-grade material. Many standalone sponge iron plants are either operating at reduced capacity or have temporarily halted production due to poor margins. At the same time, consumers using iron ore lumps are increasingly demanding consistent quality, but maintaining uniform grade has become challenging because of variations in ore quality from different mining leases. As a result, several buyers are gradually shifting their preference towards pellets, which offer better consistency and improved operational efficiency.”

Rationale

- Zero (0) trade via e-auction was recorded for Fe 57% in this publishing window and was not taken into consideration. Hence, the T1 trade category was accorded 0% weightage.

- Sixteen (16) offers and indicative prices were reported, out of which eleven (11) were considered as T2 trades. These were accorded 100% weightage.

C-DRI prices fall by INR 100/t ($1/t) w-o-w in Bellary: Sponge iron (C-DRI) prices in Bellary fell by INR 100/t ($1/t) w-o-w to INR 26,000/t ($272/t) primarily due to subdued demand from secondary steelmakers amid weak finished steel prices and sluggish order bookings. Compressed production margins prompted buyers to adopt a need-based procurement strategy, resulting in lower trading activity.

Outlook

Karnataka’s iron ore market is likely to remain under pressure in the near term as weak demand from sponge iron producers and subdued finished steel prices continue to weigh on buying activity. Lower-grade fines are expected to face persistent demand challenges due to ample availability, while benchmark-grade material may remain relatively supported by tight supply. Unless downstream steel demand improves significantly, prices are expected to trade within the current range.

Leave a Reply