- Domestic spot zinc trades above HZL benchmark amid tightening physical supply

- Limited imports, supply constraints support sentiment

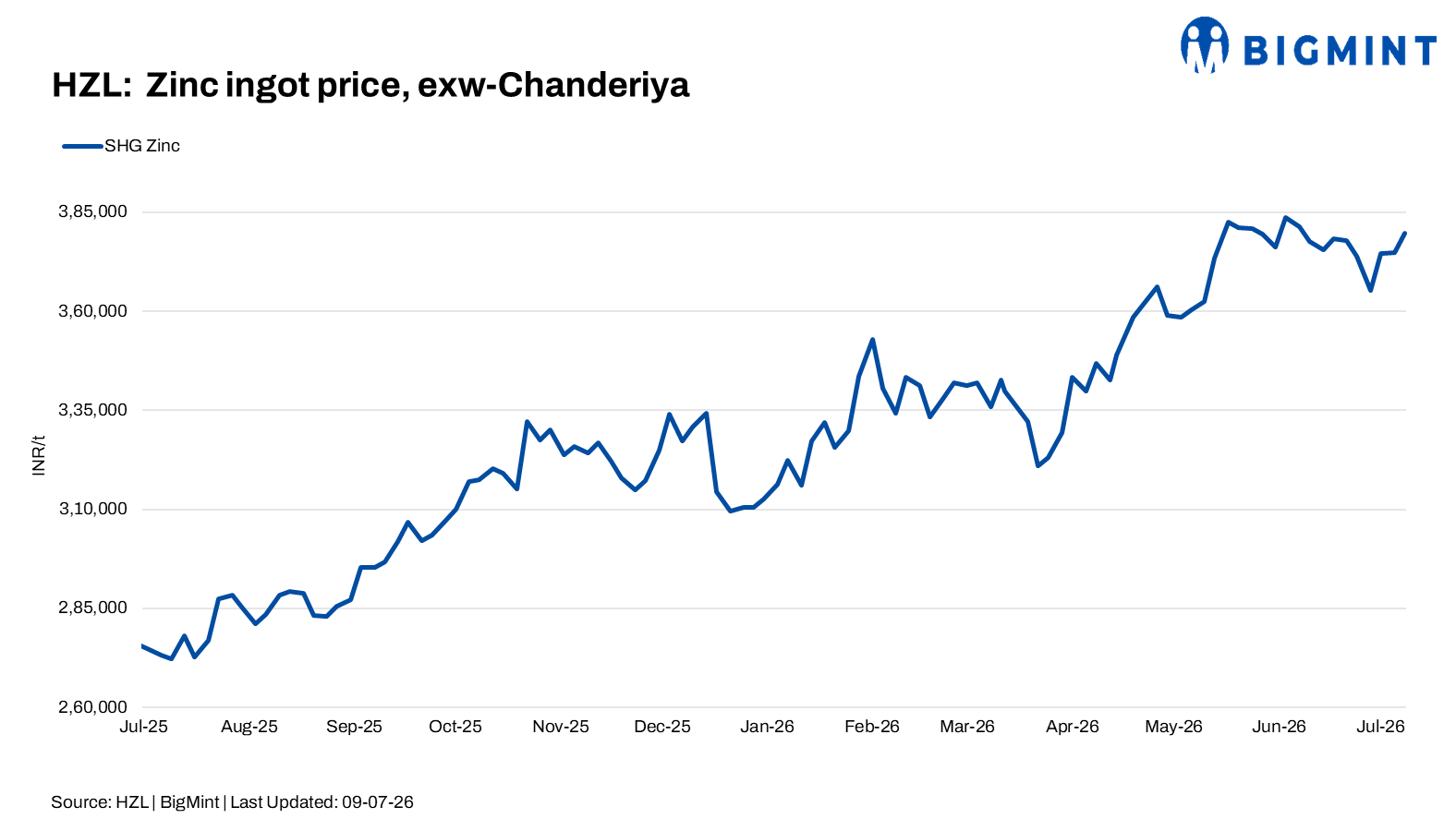

Hindustan Zinc Ltd (HZL) on 9 July 2026 increased zinc ingot prices by INR 4,900/t ($57/t) and lead ingot prices by INR 900/t ($10/t) compared with its previous revision announced on 6 July.

Following the latest revision, HZL’s benchmark Special High Grade (SHG) zinc ingot prices were raised to INR 379,700/t ($4,438/t), while lead ingot prices increased to INR 211,200/t ($2,468/t).

On the London Metal Exchange (LME), zinc prices were trading at $3,542/t, up 0.4%, while lead prices stood at $1,890/t, marginally down by 0.05% as of 6:00 PM IST. Zinc remained supported by improving sentiment amid tightening physical availability.

Despite the latest price increase, HZL’s benchmark SHG zinc prices remained below prevailing domestic spot market levels. According to BigMint’s assessment, SHG zinc ingot prices were assessed at INR 381,000/t ex-Delhi on 9 July, up INR 3,000/t d-o-d, placing the domestic spot market at a premium of around INR 1,300/t over HZL’s benchmark prices. The narrowing gap reflects strengthening physical market conditions, with higher domestic prices supported by constrained availability.

Market participants indicated that fresh import arrivals remained limited, with only previously delayed transshipment cargoes gradually entering the Indian market. At the same time, higher production costs and maintenance activities at key facilities have curtailed supply, lending further support to domestic prices. Traders noted that HZL’s benchmark revisions continue to serve as the primary reference for pricing decisions across the domestic market, even as physical spot prices have moved above the producer’s benchmark.

Fundamentally, the zinc market continues to derive support from tightening supply-side conditions. LME zinc inventories have declined steadily over the past week, to 115,925 t on 8 July from 119,200 t on 1 July, reflecting reduced exchange availability. Limited import inflows, ongoing concentrate tightness, and production-related constraints are expected to keep refined zinc availability relatively firm in the domestic market, while demand from galvanising and die-casting segments remains broadly stable.

Overall, domestic zinc prices are expected to remain well supported by constrained supply, falling exchange inventories, and firm physical market conditions. However, global macroeconomic uncertainty and volatility across international base metal markets may continue to influence short-term price movements, prompting consumers to maintain a cautious procurement approach despite improving domestic fundamentals.

Leave a Reply