- Weak demand limits aggressive buying

- Rising costs reshape production strategies

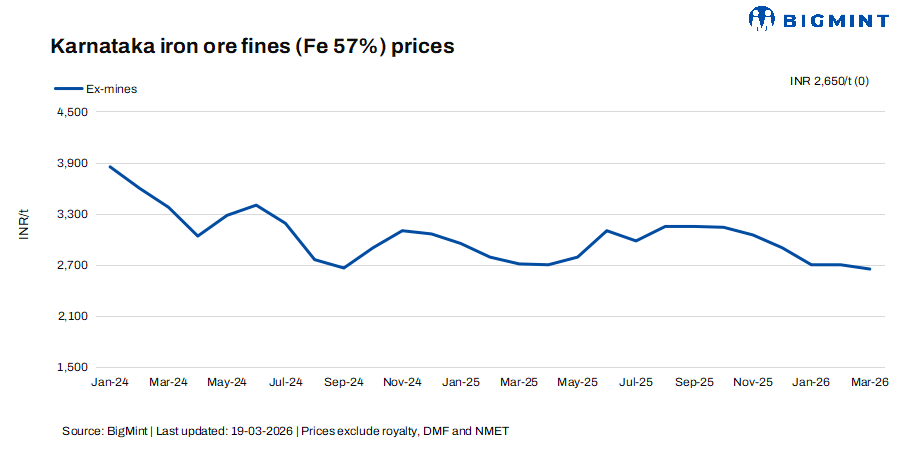

Karnataka’s iron ore market continues to reflect a resilient and firm undertone, as per BigMint’s latest weekly assessment, with prices largely holding steady despite volatility in downstream sectors. Supply-side constraints, coupled with disciplined and need-based procurement by buyers, have supported market stability. Low-grade fines (Fe 57%) remain unchanged at INR 2,700/t ($30/t) ex-mines, while Fe 62% fines also held firm at INR 5,100/t ($56/t), indicating limited downside amid cautious sentiment.

However, the steady trend in iron ore prices stands in contrast to the correction witnessed in downstream steel and sponge iron segments. Weak demand and shrinking margins continue to weigh on steelmakers, creating a widening disconnect between raw material costs and finished steel realizations. This imbalance is increasingly raising concerns about the sustainability of current ore price levels in the near term.

A key highlight of the market remains the strong traction for high-grade material. Auctions for superior-grade ore are witnessing robust participation, driven by tight availability across the region. Miners are tactically offering high-grade lots at relatively lower base prices, intensifying bidding activity and supporting firm realizations. The market is clearly shifting toward quality-focused procurement, with buyers prioritizing consistent chemistry and lower levels of impurities such as alumina and phosphorus over purely price-driven decisions.

On the demand side, procurement behavior has become increasingly selective. Buyers are focusing on securing reliable, high-quality feedstock to optimize operational efficiency rather than accumulating volumes. Even attractively priced material is being avoided if it does not meet stringent quality parameters, highlighting a structural shift toward performance-driven purchasing.

Market feedback further underscores these dynamics. A Bellary-based miner indicated that “the persistent shortage of high-grade ore continues to support strong price realizations, with auctions witnessing healthy participation”. In contrast, a regional buyer highlighted mounting cost pressures, noting that “while demand remains subdued, rising coal prices amid ongoing geopolitical tensions are significantly increasing production costs. Any further rise in iron ore prices, combined with elevated coal costs, could compress margins and push buyers into loss-making territory.”

The sponge iron segment, in particular, is undergoing structural adjustments. Weak demand for coal-based DRI (CDRI) and operational challenges among smaller, independent players have led to a gradual shift toward pellet-based DRI (PDRI), which is perceived as more efficient and easier to operate. This transition is subtly reshaping raw material consumption patterns and influencing buying preferences in the iron ore market.

Rationale

- Zero (0) trade via e-auction was recorded for Fe 57% in this publishing window and was not taken into consideration. Hence, the T1 trade category was accorded 0% weightage.

- Thirteen (13) offers and indicative prices were reported, out of which twelve (12) were considered as T2 trades. These were accorded 100% weightage.

C-DRI prices fall by INR 300/t ($3/t) w-o-w in Bellary: Prices of sponge iron (CDRI) in Bellary fell by INR 300/t ($3/t) w-o-w to INR 27,900/t ($299/t) primarily due to weak demand from steel manufacturers. Buyers have remained cautious in their procurement, as finished steel demand has not been strong enough to support higher raw material purchases.

At the same time, sponge iron manufacturers are facing pressure on their conversion margins. A sharp increase in coal prices has raised the overall production cost, while selling prices of sponge iron have not seen a corresponding rise. This mismatch is narrowing the conversion spread for producers.

Karnataka iron ore sales scenario (13-19 March 2026)

Outlook

The near-term outlook for Karnataka’s iron ore market remains cautiously stable. While supply constraints and strong demand for high-grade material are expected to support prices, persistent challenges such as dispatch issues, rising coal costs, and weak downstream demand may cap any significant upside. Market direction will largely depend on improvements in steel demand, resolution of logistical bottlenecks, and cost dynamics across the value chain.

Leave a Reply