- Buyers cautious amid rising landed costs, limited price clarity

- Demand rises as mills prefer lower grades amid rising coal prices

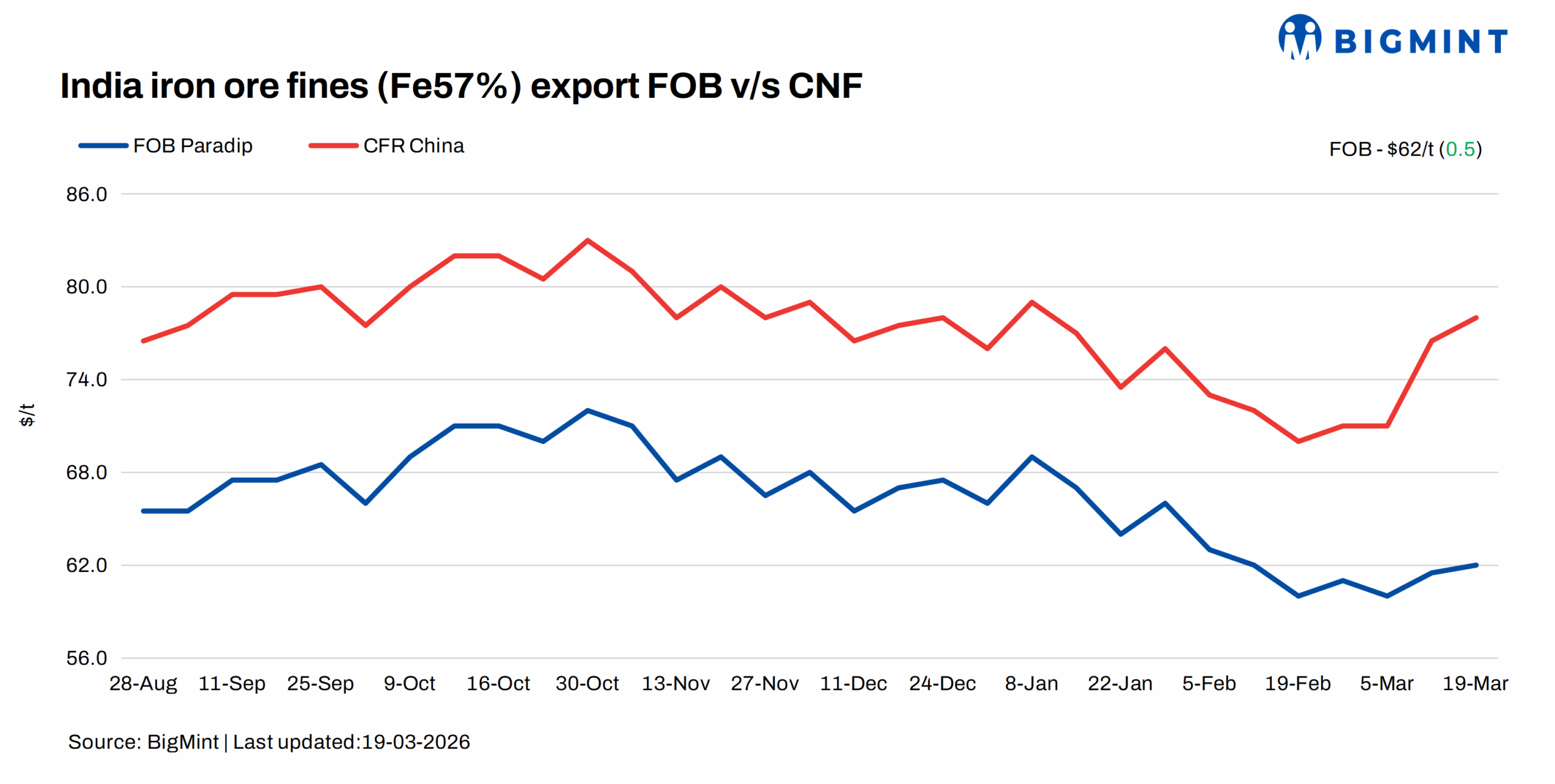

India’s low-grade iron ore fines export prices increased marginally w-o-w on 19 March 2026. However, rising vessel freights and ongoing geopolitical tensions continued to slow down trade and pressure exporter margins, keeping overall market sentiment cautious.

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index increased by $0.5/t w-o-w to $62/t FOB east coast on 19 March against 12 March.

No major deals were confirmed during the current publishing window, with most cargoes still under negotiation.

Meanwhile, CFR China levels rose more sharply by around $2/t w-o-w to $78/t, largely driven by higher freight costs.

Market scenario

Trading activity remained subdued, with most discussions still under negotiation and only limited deals closed. Sellers continued to hold firm offers, while buyers stayed cautious amid rising landed costs and a lack of price clarity.

Freights remained a key concern in the current geopolitical scenario, with vessel rates rising sharply and impacting overall import economics. An international trader noted, “Higher freight and fuel costs, along with vessel tightness, are pushing CFR levels up, making buyers more cautious.”

An exporter said, “FOB prices have moved up only slightly, but bids are not workable, as freights have increased significantly.”

BigMint’s assessment for Supramax vessel freights from Paradip (India) to Qingdao (China) stood at $15.5/t, rising $0.5/t w-o-w on 17 March 2026, driven by an uptick in the Capesize segment and firmer forward freight agreement (FFA) levels. However, overall market activity remained subdued, with participants adopting a cautious stance amid bunker price volatility and rising freights.

Market participants highlighted that rising coal prices forced Chinese mills to readjust their raw material mix, shifting focus to lower grades and further improving demand for Indian fines. Import margins remained under pressure, keeping buying interest weak.

Additionally, the market remained largely quiet this week amid an ongoing conference in Qingdao, with participants adopting a wait-and-watch approach and expecting clearer direction following the event.

Deal activity was limited, with discounts largely stable. Demand was seen more for single-mine cargoes, while blended cargoes continued to receive a weaker response. International traders also mentioned that price clarity is still lacking in the market, contributing to the cautious stance among buyers.

Domestic vs export market

Domestic prices exceeded export realisations by around INR 550/t ($6/t), with the gap being largely stable w-o-w. Iron ore fines (Fe 57%) prices in Odisha were recorded at INR 3,850/t ($41/t) ex-mines, down marginally w-o-w on 18 March. Meanwhile, the ex-mines realisation in exports from the Barbil region was recorded at INR 3,300/t ($35/t) ex-mines.

Chinese iron ore fines prices rise w-o-w: The benchmark iron ore fines Fe 61% index increased by $4/dmt w-o-w to $109/dmt CFR China on 18 March. Chinese steel futures rose d-o-d on better downstream demand and improved mill output outlook, supporting sentiment. However, seaborne activity stayed muted as ongoing negotiations with a major miner pushed buyers to delay spot deals. Import losses and high portside stocks capped price gains and curbed offer increases.

DCE iron ore futures rise: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 807.5/t ($111/t) on 19 March, largely stable w-o-w.

Rationale

- No (0) deals for Fe 57% was recorded during this publishing window, and thus, this category was not taken for calculations. Therefore, T1 trade was given 0% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received eighteen (18) indicative prices in the current publishing window, and twelve (12) were considered for price calculation as T2 inputs and given rest 100% weightage.

Outlook

Iron ore fines export prices are expected to remain firm next week, as Indian domestic prices are stable and material availability is tight. However, rising freights may lead to exporters’ inability to keep CFR levels high. A few deals are under negotiation; these could be concluded in the coming weeks if pricing aligns.

Leave a Reply