- Odisha dispatch restrictions weigh on supply

- Discount remains stable compared to last week

The Indian seaborne iron ore export market remained firm this week, supported by improving market fundamentals and tightening availability of lower-grade cargoes. However, buying interest for Indian fines continued to remain subdued, with overseas buyers resisting higher offer levels despite reduced supply.

Rationale

- No deal for Fe 57% was recorded during this publishing window and was not taken under prices calculation. Therefore, T1 trade was given 0% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received fifteen (15) indicative prices in the current publishing window, and eleven (11) were considered for price calculation as T2 inputs and given the rest 100% weightage.

Prices, deals

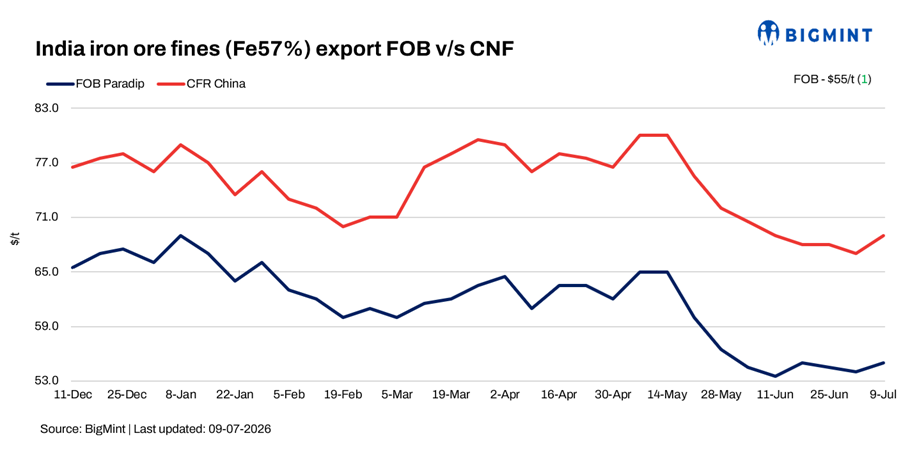

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index increased by $1/t w-o-w to $55/t FOB (equivalent to $69/t CFR China) east coast on Thursday, 9 July.

An Odisha-based exporter concluded an export deal for 120,000 t of Fe 57% fines at $69-70/t CFR China last weekend. No deals were recorded this week amid cautious market sentiments.

Market participants said freight rates have increased following recent geopolitical developments, adding pressure on exporters’ margins. As a result, FOB realisations have remained under pressure even as CFR offers stayed firm.

Several buyers’ bids were heard at discounts of around 23-26% to benchmark prices for Fe 57% fines but due to higher offers from sellers market, deals were absent in this publishing window from east coast.

Market scenario

An exporter based on the east coast said, “Vessel freight has increased noticeably over the past couple of days, which is squeezing exporters’ margins. Although CFR prices have improved, FOB returns have not increased proportionately, making fresh sales difficult.”

A couple of export shipments were concluded by Odisha-based miners last week, reflecting limited but steady demand for miner-owned cargoes. In contrast, several trader-held cargoes remained unsold due to the wide gap between buyers’ expectations and sellers’ offers.

An international trader noted, “Indian suppliers are currently seeking around $72-73/t CFR China for 57% Fe fines, while most Chinese buyers are bidding only $68-70/t CFR China. Until this pricing gap narrows, trading activity is likely to remain limited.”

Chinese steel mills are also showing greater preference for pellet cargoes over lower-grade fines, supported by better cost efficiency and improved blast furnace economics. Market sources indicated that elevated inventories of lower-grade fines at Chinese ports have further reduced the urgency for mills to procure additional Indian fines.

Iron ore inventories at 34 major Chinese ports stood at 155 (excluding pellets) mnt as of 8 July, remaining stable w-o-w.

Supply from India has also tightened following the recent Directorate of Geology and Mining (DGM), Odisha notification linking iron ore dispatches to the average mine planning grade. According to market participants, the directive has slowed the movement of lower-grade ore from Odisha, reducing export availability and supporting sentiment in the seaborne market.

An Odisha-based exporter commented, “The dispatch restrictions have reduced the availability of lower-grade material for exports. Fresh offers have slowed considerably, and miners are in no hurry to sell at discounted prices.”

Domestic vs export market

The price gap between export and domestic realisations was recorded at INR 450/t this week. Export realisations (Fe 57%) were at INR 2,850/t ($31/t) this week while domestic realisations (Fe 57%) remained stable at w-o-w at INR 3,300/t ($35/t) exw.

Chinese iron ore fines prices rise w-o-w: The benchmark iron ore fines Fe 61% index inched up by $1/t w-o-w to $99/dmt CFR China on 8 July. Prices tracking gains in Dalian iron ore futures as renewed geopolitical tensions in the Middle East and concerns over potential supply disruptions from Australia lifted market sentiment. However, subdued physical trading and lower steel output in China continued to cap further gains.

DCE iron ore futures stable w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2026 contract remained stable w-o-w at RMB 745/t ($110/t) on 9 July.

Outlook

BigMint expects Indian seaborne iron ore prices to remain firm in the near term, supported by constrained supply, while most trading activity is likely to continue through miners rather than traders until buyer resistance eases.

Leave a Reply