- Slow material lifting amid ample supply puts pressure on market

- Buyers await demand recovery despite July HRC price cuts

India’s coated flat steel market remained subdued during the week ended 9 July 2026, with prices under pressure as weak downstream demand and slow inventory movement continued to weigh on trading activity. Major mills reduced coated steel prices by around INR 1,000-1,250/t during the week in an effort to stimulate demand. However, buying interest remained limited, with distributors and end-users restricting purchases to immediate requirements amid ample material availability in the market.

Price update

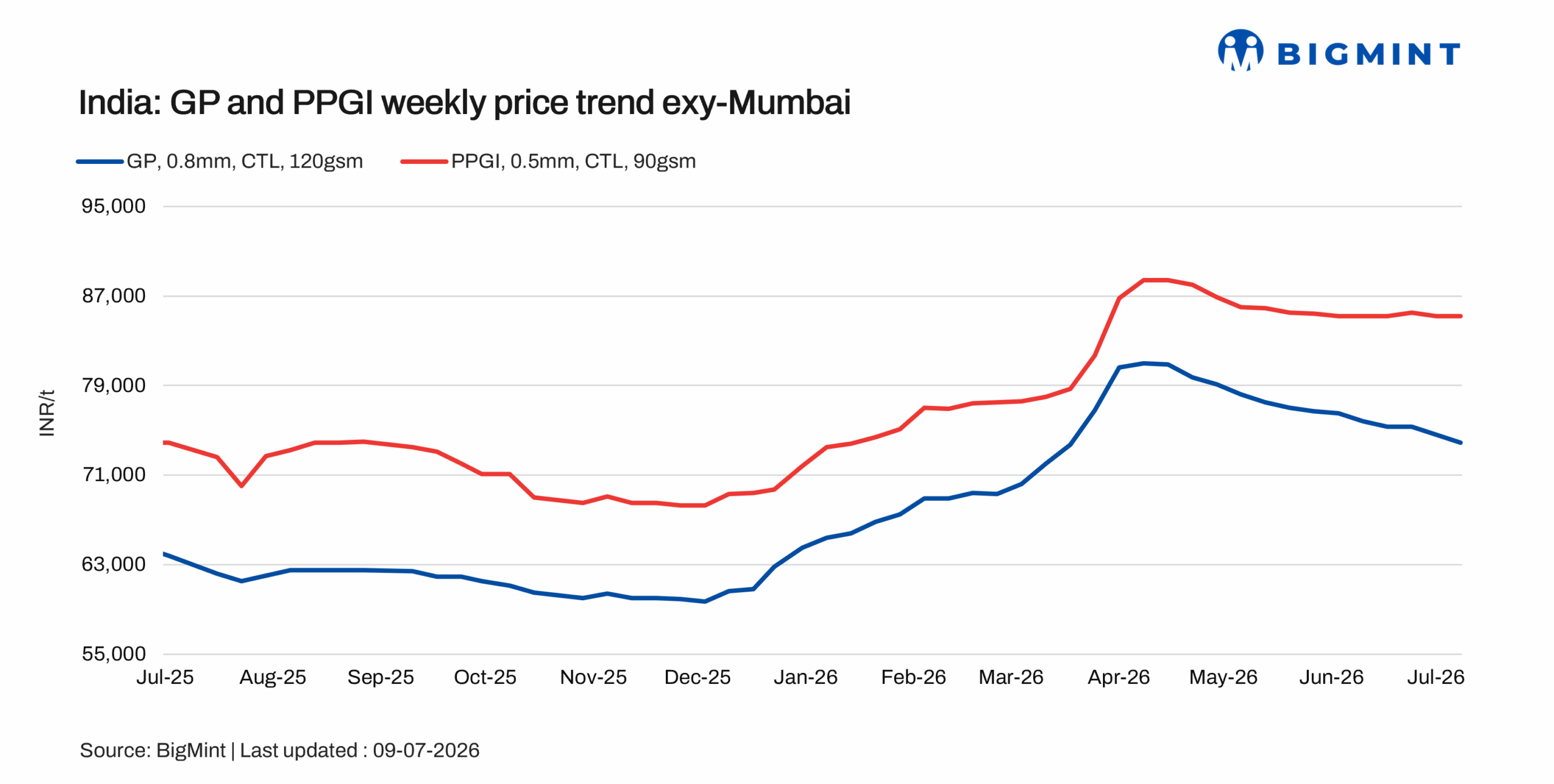

BigMint’s benchmark assessment for Mumbai GP coil (0.8mm/CTL, 120 GSM, IS 277) declined by INR 700/t w-o-w to INR 73,900/t ex-Mumbai. The correction reflected weak spot demand, comfortable inventories throughout the supply chain, and sluggish material lifting despite lower mill offers.

Meanwhile, Mumbai PPGI (0.5mm/CTL, 90 GSM, IS 14246) remained stable w-o-w at INR 85,200/t as limited transactions and balanced replacement costs prevented further price correction.

Similarly, Mumbai BGL (0.5mm/CTL, 1220mm, AZ150) remained largely unchanged w-o-w at INR 89500/t during the week, supported by stable replacement costs despite subdued booking activity.

Raw material prices

India’s zinc ingot (99.995%) prices increased by INR 7,000/t w-o-w to INR 377,000/t ex-Delhi, according to BigMint’s latest assessment. The recovery followed Hindustan Zinc Ltd’s upward price revision, firmer global zinc fundamentals, and continued tightness in imported material availability. Despite higher zinc prices, downstream procurement from galvanisers and alloy manufacturers remained largely need-based amid the ongoing monsoon season.

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) remained stable w-o-w at INR 58,200/t ($613/t) ex-Mumbai as of 7 July, reflecting balanced market fundamentals despite subdued spot buying.

Meanwhile, CRC (IS513, Grade O, 0.9 mm/CTL) edged down by INR 200/t to INR 65,000/t ($687/t) ex-Mumbai, reflecting cautious buying and competitive market offers.

Market updates

The Indian coated flat steel market remained subdued during the assessment period despite major mills reducing coated steel prices by around INR 1,000-1,250/t. Demand from key end-use sectors remained weak, resulting in slow material lifting across the distribution network. Inventory levels in the market were estimated at 30-35 days, while supply remained comfortable, reducing the urgency for fresh procurement and keeping pressure on spot prices.

The stability in domestic hot-rolled coil (HRC) prices, the primary substrate for coated flat products, provided mills with limited cost support. However, mills were compelled to reduce coated steel prices as weak downstream demand and elevated inventories outweighed stable raw material costs. As a result, distributors and service centres continued to procure only against confirmed orders, while competitive offers persisted across the market.

The Directorate General of Trade Remedies’ (DGTR) anti-dumping investigation into HRC imports from China, Japan and Russia could gradually reshape the coated flat steel market. Since HRC is the key feedstock for galvanised and colour-coated products, any anti-dumping duty that raises domestic HRC prices would increase production costs for coated steel manufacturers. While current coated steel demand remains too weak for mills to fully pass on higher costs, tighter HRC imports could reduce pricing pressure on domestic producers once inventories normalise and demand improves.

At the same time, stronger Indian HRC exports, particularly to Southeast Asia, have helped divert excess domestic flat steel volumes. Continued export opportunities could gradually improve domestic HRC supply-demand fundamentals, providing indirect support to coated steel prices over the coming months. However, in the immediate term, sluggish consumption, slow inventory movement and adequate supply are expected to remain the dominant drivers of the coated flat steel market.

Outlook

India’s coated flat steel market is expected to remain under pressure through July as weak downstream consumption, slow inventory movement and comfortable supply continue to weigh on buying sentiment. While mills have already reduced prices to improve offtake, sustained demand recovery will be necessary to support any meaningful improvement in market activity. Market participants will also closely monitor developments in the DGTR anti-dumping investigation and export opportunities, which could influence domestic supply dynamics over the coming weeks.

Leave a Reply