- Preference for high-grade ore sustains market activity

- Weak response to low-grade material limits some volumes

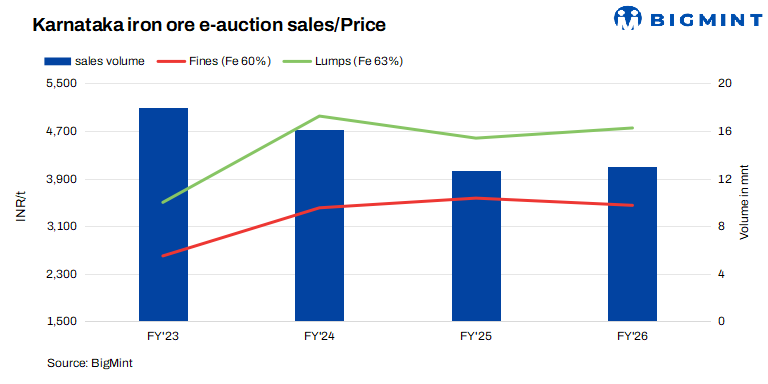

Karnataka’s iron ore e-auction sales volumes remained largely stable in FY’26, inching up marginally by 3% y-o-y to 13 million tonnes (mnt) compared to 12.66 mnt in FY’25, according to data maintained with BigMint. The stability was primarily driven by a balance between weak and strong demand phases during the year, strategic base price corrections by miners, and consistent supply support from NMDC Ltd. Additionally, cautious yet continuous procurement by buyers and sustained preference for high-grade material helped maintain auction participation despite intermittent market volatility.

On a monthly basis, volumes showed improving momentum towards the end of the fiscal, with March 2026 sales rising by 9% m-o-m to 1.25 mnt from 1.15 mnt in February, indicating a gradual recovery in buying activity.

NMDC Ltd. tops the chart with strong growth

NMDC retained its leadership position in Karnataka’s e-auction market, selling around 10 mnt (around 77% out of total auction volume) in FY’26, up 10% y-o-y from 9.11 mnt in FY’25. The miner contributed the largest share to total auction volumes, reinforcing its dominant presence in the market.

The growth was supported by key strategic initiatives, including a shift in pricing structure from inclusive to exclusive in January 2026, along with consistent base price reductions to align with market sentiment. These measures improved buyer participation and enabled higher auction clearances, particularly during weaker demand phases.

Other miners show mixed performance

Sandur Manganese and Iron Ores (SMIORE) emerged as the second-largest contributor, with sales of 1.18 mnt in FY’26, marginally down by 2% y-o-y.

Karnataka State Minerals Corporation Limited (KSMCL) ranked third, with volumes declining sharply by 33% y-o-y to 0.96 mnt. The drop was largely attributed to weak buyer response to low-grade material and multiple unsuccessful auctions, which weighed on overall volumes despite price corrections.

Vedanta Limited recorded a 37% y-o-y decline in sales to 0.41 mnt, reflecting limited offerings and lower production levels. However, some late-fiscal auction results remain excluded from the total.

Among smaller miners, Sri Kumaraswamy Minerals Private Limited sold 164,000 tonnes, while R Praveen Chandra recorded 146,300 tonnes, supported by better material quality and competitive pricing. Other players such as U Krishna Prasad, BKG Mining, and RPCL contributed minimal volumes, indicating a concentrated market structure.

Why volumes remained stable in FY’26

- Balanced demand cycles across the year: Crude steel production in India increased by 10.5% y-o-y to 168 mnt in FY’26, marking continued capacity-led growth, albeit at a more measured pace compared to the sharper expansion seen in the previous fiscal. The overall stability in auction volumes was largely driven by a balancing effect between weak and strong demand phases. While demand and cautious sentiment post-monsoon period and early 2026 kept the market intact.

- Strategic pricing interventions by miners: Base price corrections particularly by NMDC played a crucial role in reviving buyer interest. Competitive pricing enabled better bid alignment and higher auction clearances during periods of subdued demand.

- Preference for high-grade material: Consistent demand for high-grade iron ore supported auction participation, even as low-grade material struggled to attract bids. This selective buying trend helped sustain volumes in quality-driven auctions.

- Cautious yet consistent procurement: Buyers maintained minimum procurement levels to ensure uninterrupted plant operations. This steady baseline demand prevented sharp declines in auction volumes despite market volatility.

Prices exhibits mixed trend y-o-y in FY’26

The yearly weighted average e-auction prices in Karnataka exhibited a mixed trend in FY’26, reflecting shifting demand dynamics and quality preferences in the market. Iron ore fines (Fe 60%) averaged INR 3,450/t ($37/t), marking a decline of around INR 121/t y-o-y, while lump prices (10–40 mm, Fe 63%) increased by approximately INR 171/t to INR 4,750/t ($50/t). On a monthly prices declined by INR 300/t ($3/t) for fines and INR 400/t ($4/t) for lumps. Prices are on an ex-mines basis, excluding royalty, DMF, and NMET.

The decline in fines prices was primarily attributed to relatively comfortable availability and subdued demand during certain periods, particularly when steelmakers maintained cautious procurement strategies and operated with adequate inventories. In contrast, lump prices remained firm and moved higher, supported by tighter supply and steady demand from sponge iron producers, for whom lumps are a preferred raw material due to operational efficiency.

Outlook

Karnataka’s iron ore e-auction market demonstrated resilience in FY’26, with stable volumes despite demand fluctuations and structural shifts in sales strategies. Going forward, volumes are expected to remain range-bound, with steel demand trends, pricing strategies by miners, and availability of high-grade material continuing to shape market dynamics.

Leave a Reply