- Limited inquiries at higher discount rates for Indian fines in sea market

- Sellers hold export offers following the weak demand and higher domestic fines prices

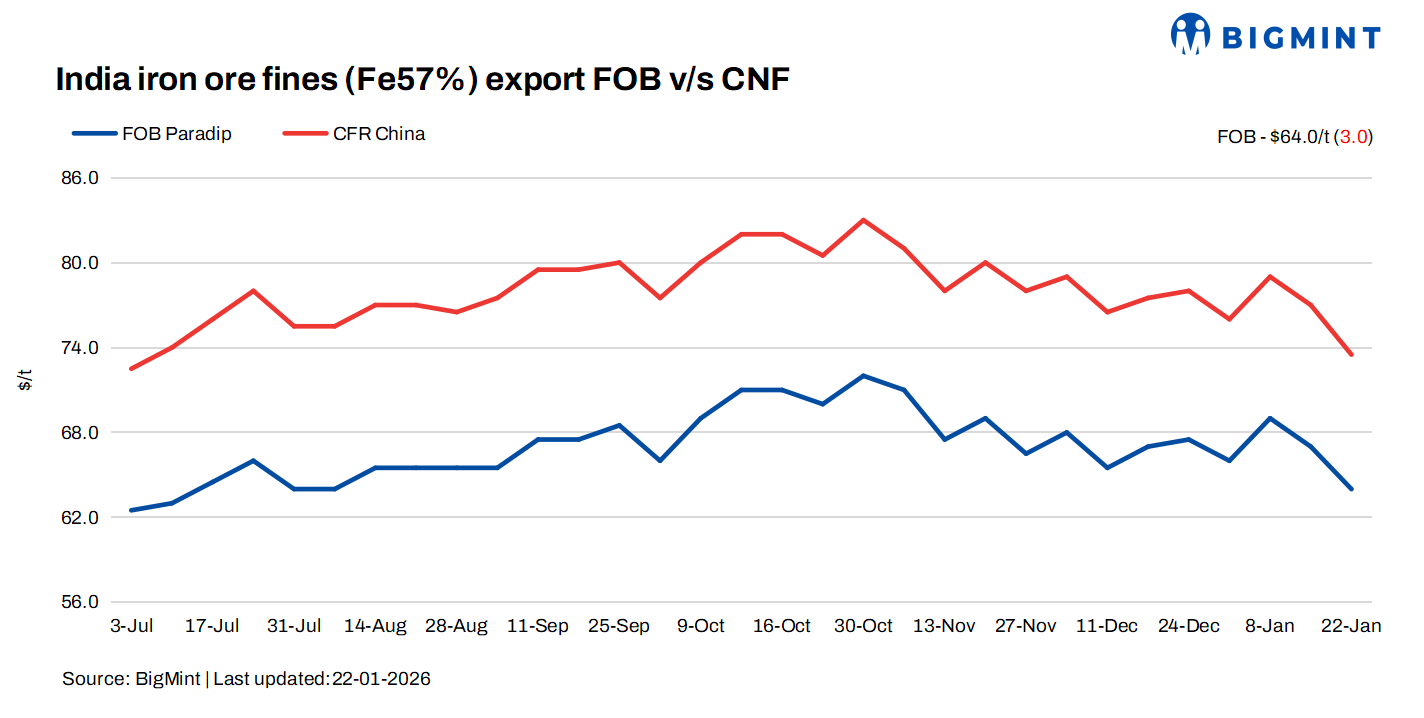

Indian iron ore fines export prices continued to weaken in the seaborne market this week, assessed 22 January 2026, pressured by higher discount rates against global benchmarks and subdued demand from China

Prices, deals

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices decreased by $3/tonne (t) w-o-w to $64/t FOB east coast on Thursday. Meanwhile, the index stood at $73.5/t CFR China.

Despite subdued market sentiments and lower export price realizations, a few Indian iron ore exporters managed to secure deals in the sea market over the past week. BigMint recorded approximately 450,000 tons of spot export deals for iron ore with Fe content between 55% and 57%.

According to sources, the export discount for Fe 57% fines widened to around 23-25%, while discounts for Fe 55% material increased to nearly 29-30% against the global fines index.

Market scenario

The oversupply of iron ore in China has persisted, keeping buying interest limited for seaborne cargoes. Traders noted that Chinese mills are currently well-stocked, with ample material available at ports, reducing their urgency to procure additional cargoes from the seaborne market. Meanwhile, global iron ore benchmark prices declined during the week, further weighing on sentiment across the sea market.

Market participants highlighted that discount rates for lower-grade iron ore material have increased sharply in China. An international trader said, “Mills are focusing on portside procurement as it is more cost-effective. Seaborne material is not their immediate purchasing priority.”

Indian sellers reported that some seaborne buyers have offered discounts of around 25% against benchmark prices for fines cargoes. However, domestic iron ore prices in India have continued to rise, keeping sellers’ cost structures elevated. An exporter informed, “With higher domestic prices, it is difficult for us to accept such steep discounts.”

Some sellers also indicated that they are anticipating discount levels of around 20% for post–Chinese holiday laycan cargoes and are currently not in a hurry to conclude fresh deals. Another exporter added, “We expect some correction after the holidays and are waiting for better pricing clarity.”

Despite the weak sentiment, a few miners are continuing to ship cargoes, as bulk deals were concluded several weeks ago at comparatively higher price levels.

Market participants expect Indian iron ore export prices to remain volatile in the near term, with demand likely to stay subdued. However, a few shipments may be concluded in the coming week, particularly if Chinese buyers find seaborne prices attractive amid expectations of short-term price stabilisation.

Domestic vs export market

Domestic prices exceeded export realisations by around INR 400/t ($4/t), with the gap widening w-o-w. Iron ore fines (Fe 57%) prices in Odisha were recorded at INR 4,050/t ($44/t) ex-mines, rising by INR 100/t ($1/t) w-o-w today. Meanwhile, the ex-mines realisation in exports from the Barbil region fell w-o-w to INR 3,650/t (40/t) ex-mines.

Chinese spot prices down w-o-w: The benchmark iron ore fines index (Fe 61%) recorded at $103/t CFR China, fell $5/t w-o-w on 21 January. Softer prices drew buyers, lifting trading activity in mainstream medium-grade fines as participants took advantage of the dip. Cargoes with full-month laycans were trading at discounts of up to 30 cents/dmt amid laycan differences, while some mills began looking at alternatives to low-grade material.

DCE iron ore futures fall w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 786.5/t ($113/t) on 22 January 2026, and dropping by RMB 26.5/t ($4/t) w-o-w.

Rationale

- One (1) deal for Fe 57% was recorded during this publishing window; not taken for price calculation. Therefore, T1 trade was given 0% weightage in the index calculation. A few deals were already factored into Monday’s assessment. For the detailed methodology, click here.

- BigMint received seventeen (17) indicative prices in the current publishing window, and thirteen (13) were considered for price calculation as T2 inputs and given 100% weightage.

Outlook

Indian seaborne iron ore fines prices are likely to remain volatile due to current global price dynamics and the higher stock levels at Chinese ports, which may limit further export deals from India. However, a few shipments are expected to be finalized for the period following the Chinese holidays.

Leave a Reply