- Softer futures, adequate availability keep domestic trading steady

- Domestic premiums remain stable at $300-310/t above LME cash

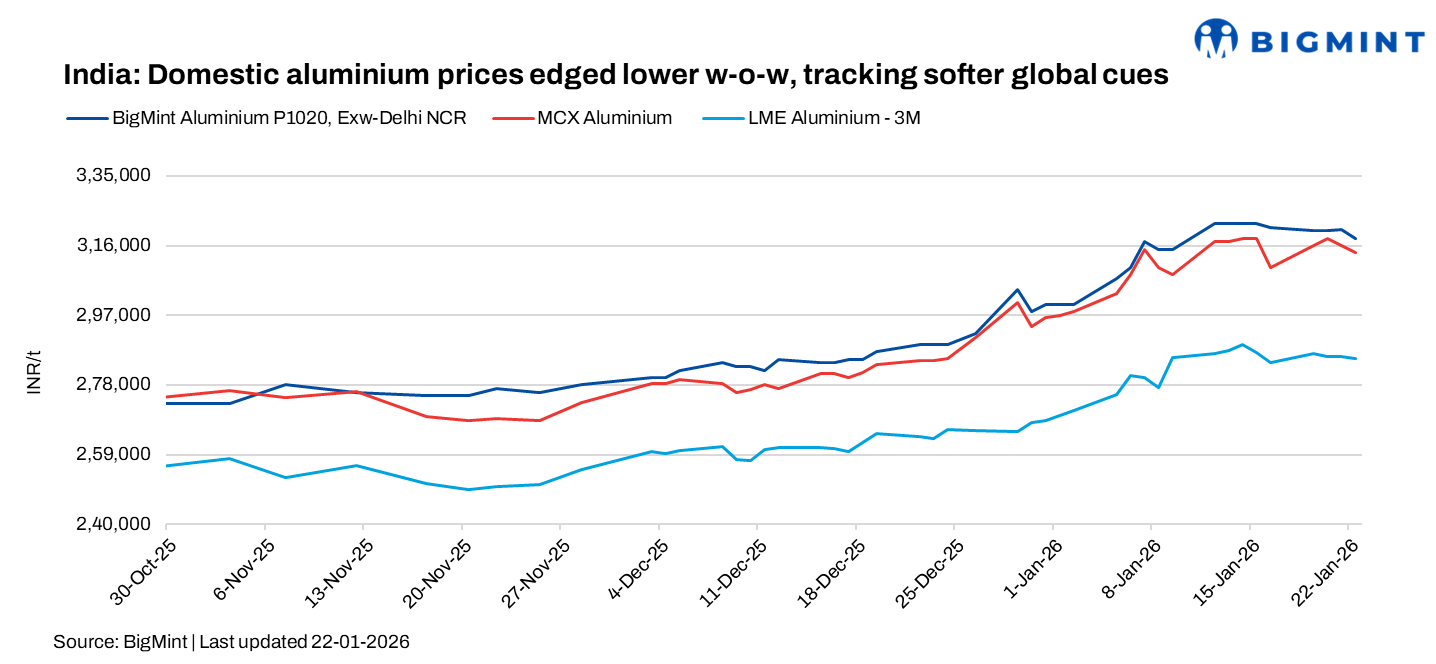

Domestic aluminium prices in India edged lower w-o-w, pressured by a dip in LME and MCX aluminium futures, even as global supply concerns persisted. The marginal correction came despite stable domestic availability, indicating that softer international price cues outweighed local fundamentals.

As per BigMint’s assessment, domestic aluminium ingot prices in Delhi declined by INR 4,000/t, or 1%, w-o-w to INR 318,000/t, while Mumbai prices fell by INR 6,000/t, or 1.8%, w-o-w to INR 319,000/t as of 22 January.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX weakened w-o-w, slipping by INR 4,000/t, or 1%, to INR 314,000/t as of 22 January, reflecting a mild correction after recent firmness.

In the global market, LME aluminium prices also moved lower, by $90/t, or 2.8%, w-o-w to $3,115/t, despite an underlying backdrop of supply-side tightness. Market sentiment continued to draw support from China’s strict enforcement of its 45-mnt smelting capacity cap, a sharp y-o-y fall in Chinese exports, and delays in overseas capacity additions — particularly in Indonesia — which together constrained incremental supply even as demand signals remained mixed.

Meanwhile, LME warehouse stocks increased by 15,175 t, or 3.1%, w-o-w to 507,175 t, indicating short-term inventory inflows. However, tight global supply conditions remained evident in physical markets. Reflecting this, the premium for aluminium shipments to Japan for January-March 2026 was set at $195/t, up 127% q-o-q and marking the first quarterly increase in a year. Elevated premiums are expected to persist into Q2CY’26, supported by ongoing smelter disruptions, tight global inventories, and firm underlying supply fundamentals, even as domestic demand remains moderate.

Aluminium majors’ pricing shows divergent trends

Domestic aluminium ingot prices showed mixed movement during the period, reflecting selective revisions by primary producers amid evolving market cues. BALCO largely maintained its pricing, holding its P1020 price at INR 339,750/t on 16-17 January before raising it to INR 341,250/t on 20 January, followed by a marginal cut to INR 339,000/t on 21 January, indicating a cautious recalibration after recent gains.

Hindalco’s pricing trended lower overall, with its P1020 price easing from INR 343,250/t on 16 January to INR 335,000/t on 17 January. Prices briefly recovered to INR 338,500/t on 20 January but softened again to INR 335,500/t on 21 January, suggesting moderated producer sentiment in response to softer market conditions.

Meanwhile, NALCO kept its P1020 price unchanged at INR 330,700/t, as last revised on 14 January, signalling a wait-and-watch approach amid mixed domestic and global signals.

Market participants indicated that sentiment in the domestic aluminium market remains stable, with demand holding steady amid a slight correction in LME prices. Comfortable inventories with major domestic producers ensured smooth supply, while trading activity stayed consistent. Premiums were reported to be stable at around $300-310/t above LME cash, reflecting sustained offtake and a balanced order book.

Participants added that the recent w-o-w decline in LME and MCX aluminium prices has supported buying interest at lower levels, helping maintain market stability. While overall demand growth remained moderate, softer futures prices and adequate availability have provided support to the domestic market, keeping momentum steady despite mixed global cues.

Japanese aluminium premium surges in Q1CY’26 on supply tightness

Japanese aluminium premiums for Q1CY’26 rose sharply by 127% q-o-q to $195/t, marking the first quarterly increase in a year. The sharp rise followed prolonged negotiations between buyers and producers due to a wide buyer-seller gap, with the final settlement reflecting tight global supply, smelter outages, and production disruptions. Key supply-side pressures included the mothballing of South32’s Mozal smelter in Mozambique, power-related disruptions at Icelandic smelters, and delays in overseas capacity additions, which pushed spot premiums higher despite muted domestic demand in Japan.

The surge in premiums was further reinforced by higher LME aluminium prices, which were up around 21% y-o-y in January 2026, and a sharp decline in LME warehouse inventories, down about 18% to below 0.5 mnt. As Japan sets a key regional benchmark for aluminium premiums in Asia, the elevated Q1 settlement highlights ongoing global supply tightness. Market participants expect premiums to remain firm into Q2CY’26, supported by persistent smelter constraints, tight inventories, and continued strength in overseas markets, even as Japanese end-user demand remains modest.

Outlook

Domestic aluminium prices are likely to remain at around current levels in the near term, supported by ongoing global supply tightness, elevated Japanese premiums, and firm overseas market fundamentals. Softer LME and MCX futures and moderate domestic demand may limit sharp gains, while steady buying interest and adequate inventories are expected to maintain market stability.

Leave a Reply