- Bid-offer disparity prevails in market

- Wait is on for NMDC’s Oct price revision

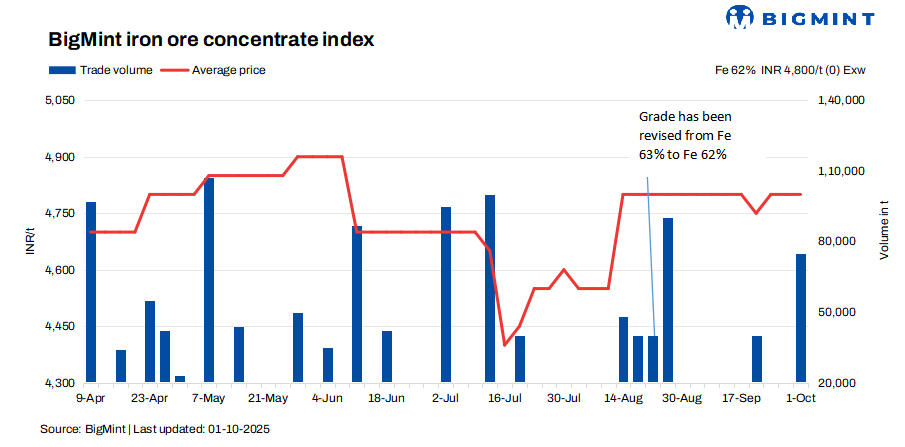

BigMint’s bi-weekly assessment for India iron ore concentrate stood unchanged at INR 4,800/tonne ($54/t) exw-Jabalpur, holding firm from the previous evaluation on 27 September 2025. Meanwhile, Fe 63% concentrate prices hovered near INR 5,000/tonne ($56/t) exw, though the absence of any concluded trades at these levels reflected the market’s hesitancy and lack of conviction.

Sellers are deliberately holding their offers steady amid an uncertain market direction and unfulfilled older orders, waiting to clear existing inventories before quoting fresh prices. The market tone remains stagnant, but anxiety is rising as participants warn that any imposition of export duty could cause a market correction, triggering a major setback in prices.

A Jabalpur-based seller told BigMint, “Buyers are unwilling to accept the current price levels, while sellers are equally firm in not lowering their offers. In most cases, deals are forced to conclude at about INR 100 below the offer price. Some negotiations are ongoing under these strained conditions, but the bid-offer disparity remains a concern.”

Adding to the cautious outlook, market sources indicated that many participants are busy clearing existing inventories ahead of planned maintenance shutdowns, leading to a near standstill in fresh buying activity. This has further deepened the prevailing uncertainty, leaving the market in a delicate balance.

Meanwhile, market participants still awaits the NMDC’s price revision for clear market directions.

Rationale

- One (1) trade was recorded in the publishing window, and taken into consideration, receiving 50% weightage

- Eight (8) offers and indicative prices were heard and were taken into consideration as T2 trades, receiving 50% weightage.

Factor supporting iron ore concentrate prices

- Pellet prices remain steady in Raipur: BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained stable at INR 10,300/t ($116/t) DAP on 30 September 2025 compared to the previous assessment on 26 September. The festive season, along with weak market sentiment, kept buyers largely on the sidelines, resulting in subdued demand. Market participants noted that recent declines in sponge PDRI and billet prices have added to buyer caution, further curbing fresh inquiries.

- Odisha iron ore fines prices firm w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index stayed firm at INR 5,300/tonne ($60/t) ex-mines on 27 September 2025, unchanged w-o-w. Prices remained largely steady despite expectations of volatility after the September OMC auction. Continuous rainfall disrupted production, limiting material availability in the region. Miners also restricted offers, further squeezing spot supply. As a result, market sentiment stayed cautious, with tight supply supporting stability in prices.

Outlook

Iron ore concentrate prices are expected to remain rangebound in the near term, supported by steady pellet and Odisha fines prices, as well as tight spot supply due to rainfall-led production disruptions. However, weak demand from buyers, bid-offer disparities, and cautious market sentiment amid declining sponge PDRI and billet prices could cap any major upside. Market participants are closely watching NMDC’s upcoming price revision and potential policy moves, such as export duty changes.

Leave a Reply