- Wide bid-offer disparities limit imported scrap purchases

- Domestic Extrusion, Taint/Tabor witness stronger demand

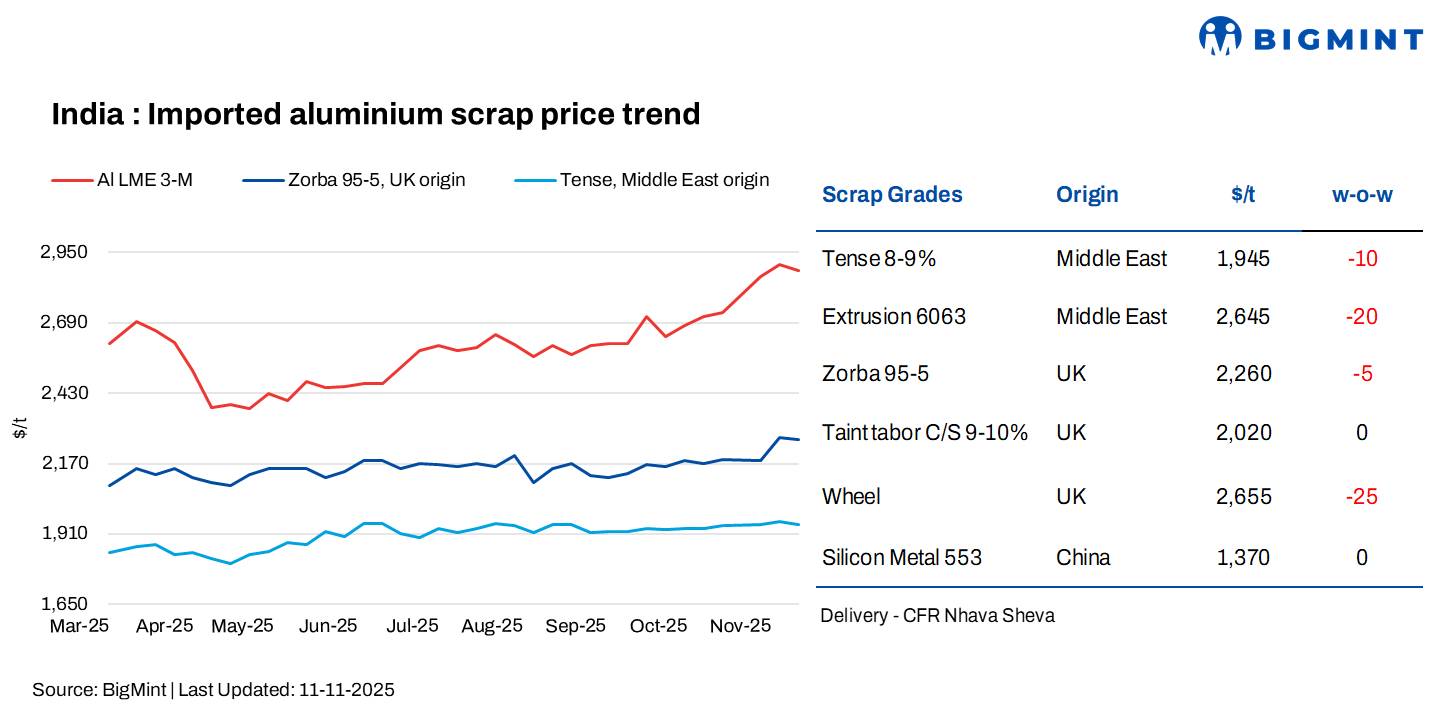

India’s imported aluminium scrap prices edged down by $20-25/t w-o-w, following negative movements on the London Metal Exchange (LME). BigMint assessed UAE-origin Tense scrap at $1,945/tonne (t), down by $10/t w-o-w, while UK-origin Taint Tabor C/S (9-10%) stood at $2,020/t, stable w-o-w.

UK-origin Zorba 95/5 stood at $2,260/t w-o-w, down by $5/t, while UAE Extrusion 6063 decreased by $20/t to 2,665/t w-o-w. Meanwhile, UK-origin Wheel decreased by $25/t to $2,655/t w-o-w.

LME prices decrease w-o-w; inventories fall

At closing on 10 November, LME aluminium prices stood at $2,883/t, down by a minor $24/t from $2,907/t last week.

Meanwhile, aluminium inventories at registered warehouses decreased notably by 7,350 t to 547,225 t from 554,575 t in the previous week, indicating tightening supply conditions.

Market scenario

The imported aluminium market remained cautious as local demand continued to stay subdued despite the relative stability in LME prices. While international benchmarks held steady, the domestic market witnessed weak buying momentum, with most participants adopting a wait-and-watch approach.

Prices of imported aluminium scrap recorded minor declines compared to previous weeks; however, trading activity slowed down due to limited procurement interest. Market participants noted that although demand exists, purchases were being made selectively, as buyers remained cautious amid high prices.

However, traders and secondary smelters noted that offers for key imported grades were elevated, leading to significant bid-offer gaps. US-origin Taint Tabor HRB with 2-3% attachment, in particular, continued to face wide disparities between bids and offers.

Selective buying interest emerged for Zorba, primarily influenced by prices and delivery terms, while most buyers remained cautious and avoided fresh bookings until market conditions showed more stability.

In contrast, the local market faced sharper price corrections. Local Tense was traded at around INR 14,000/t lower than imported material, with extended credit periods of up to 45 days offered to attract buyers.

Despite the overall sluggishness, some improvement was seen in specific segments. The Extrusion and Taint/Tabor categories witnessed relatively stronger demand, supported by a gradual recovery in downstream consumption and selective restocking by manufacturers.

Additionally, India’s aluminium ADC12 alloy ingot prices inched up m-o-m in November 2025, primarily due to the positive auto demand following GST cuts.

According to BigMint’s monthly assessment, OEM-grade ADC12 prices registered slight m-o-m increases across major regions, with Delhi and Chennai both assessed at INR 232,000/t — up by INR 2,000/t and INR 1,000/t respectively — while Pune stood at INR 231,500/t, marking a rise of INR 1,500/t; all prices are based on 30-day payment terms.

Silicon price trends

According to BigMint’s assessment, China’s 553-grade silicon prices remained largely steady m-o-m at $1,370/t CFR Mundra, driven by steady demand.

Outlook

India’s imported aluminium scrap prices are expected to remain slightly weak in the near term as local demand stays subdued. However, continued declines in LME aluminium inventories could lend some support to prices if supply tightness deepens globally. Market activity is likely to stay limited, with buyers maintaining a cautious approach amid high prices.

Leave a Reply