- Global alumina production falls on maintenance-related disruptions

- Copper climbs amid tight global mine supply, US Fed rate cut

At close of trading on 1 November 2025, base metals prices on the London Metal Exchange (LME) remained rangebound w-o-w, with zinc witnessing the highest gain of 0.99% to $3,056/tonne (t). Meanwhile, LME warehouse stocks exhibited positive trends, with aluminium witnessing the highest drop of 17.95%.

On the LME, three-month aluminium prices stood at $2,884/t, up by 0.87% w-o-w, while zinc increased by 0.99% to $3,056/t. Copper prices were at $10,088/t, up by 0.68% w-o-w, and lead was up by 0.02% at $2,017/t. Nickel stood at $15,226/t, up by 0.88% w-o-w.

London Metal Exchange (LME) copper prices climbed to a record high on 29 October, supported by tightening global mine supply and improved sentiment ahead of the upcoming US-China trade talks, along with the Federal Reserve’s latest rate cut. Prices touched $11,200/t before closing at $11,183.50/t, marking a 25% gain so far this year. Persistent supply disruptions at major mines in Indonesia, the Democratic Republic of Congo, and Chile continue to strain the market, with Glencore lowering its 2025 output forecast to 850,000-875,000 t.

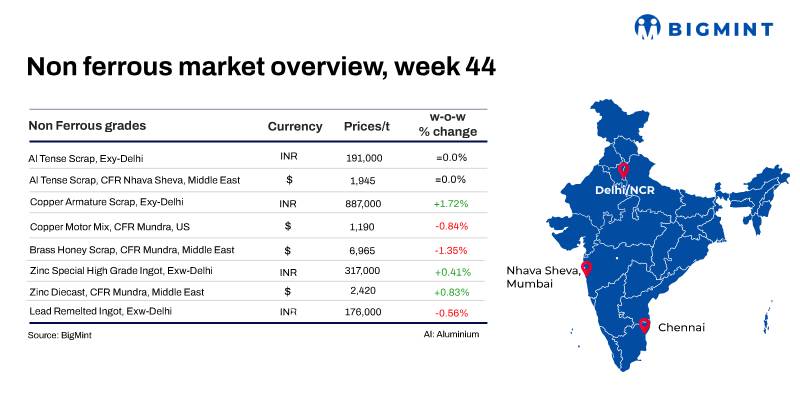

India’s imported aluminium scrap prices remained rangebound w-o-w, though London Metal Exchange (LME) benchmarks witnessed positive movements.

BigMint assessed UAE-origin Tense scrap at $1,945/tonne (t), while UK-origin Taint Tabor C/S (9-10%) stood at $2,250/t, both stable w-o-w.

Global metallurgical alumina production declined 3% m-o-m to 12.14 million tonnes (mnt) in September from 12.51 mnt in August, according to the International Aluminium Institute (IAI). The decrease was primarily attributed to maintenance-related slowdowns and energy constraints affecting major producing regions.

Global primary aluminium production in September stood at 6.08 mnt, down 3.1% m-o-m from 6.28 mnt in August. The drop reflects weaker output across major producing regions amid operational slowdowns and market adjustments.

Imported copper scrap prices in India fell w-o-w, despite gains on London Metal Exchange (LME) futures. Meanwhile, domestic copper scrap prices edged higher amid muted demand and limited activity, as the market continued to recover from the post-festive lull.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $10,180/t, down by $50/t w-o-w, while US motors mix stood at $1,190/t (both CFR Mundra), down by $20/t w-o-w.

The International Copper Study Group (ICSG) has released preliminary data for January-August 2025, indicating that global refined copper production grew approximately 4% y-o-y. This included a 3.9% increase in primary production (from ores via electrolytic and electrowinning processes) and a 5% rise in secondary production (from scrap).

Zinc

India’s zinc scrap and dross market witnessed an upward movement this week, with prices strengthening on sustained demand from local processors.

BigMint assessed zinc diecast scrap (Middle East origin) at $2,420/t CFR west coast India, up by $30/t w-o-w, amid steady inquiry levels.

Zinc dross was assessed at INR 249,000/t ex-Delhi, up by INR 8,000/t w-o-w, marking a five-month high since BigMint’s assessments began.

Domestic zinc spot prices stood at INR 316,000/t exw-Delhi, up by 4.6% w-o-w. HZL zinc prices were up by 0.3% w-o-w to INR 330,100/t ex-Chanderiya.

Lead

Domestic primary lead ingot prices stood at INR 190,000/t, down by INR 2,000/t w-o-w, while re-melted ingots stood at INR 176,000/t, up by INR 1,000/t w-o-w.

Meanwhile, HZL lead prices remained stable INR 209,400/t ex-Chanderiya.

Other updates

Nexa Resources records production surge

Nexa Resources strengthened its position as a leading global zinc producer in Q3CY’25, reporting zinc production of 84,000 t, driven by record output at Aripuan and recovery at Vazante. Net income reached $100 million, supported by higher by-product prices and disciplined costs, while adjusted EBITDA rose 16% q-o-q to $186 million. Mining cash costs improved sharply, though smelting costs increased due to raw material prices. The company maintained its 2025 zinc production guidance of 300,000–336,000 t, with sustainable initiatives like hydro-powered smelters and eco-brick production underscoring its commitment to ESG practices.

Leave a Reply