- IF rebar prices rise across markets on renewed trade optimism

- HRC prices weaken as sentiments remain muted even after Diwali

- Longs prices may rise on fresh momentum, flats outlook uncertain

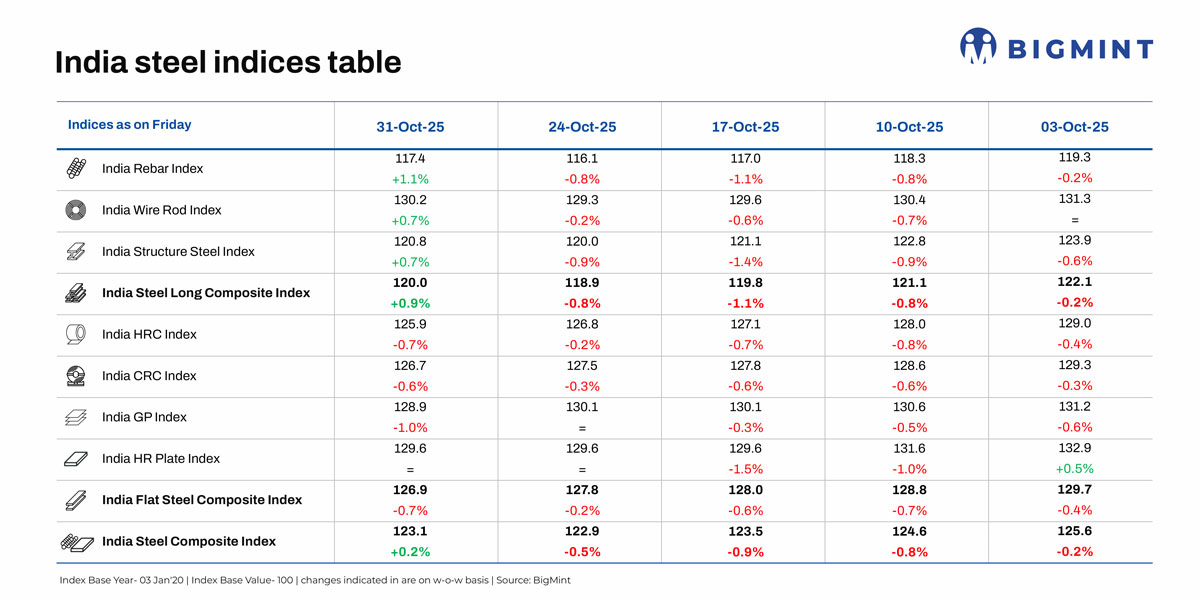

Morning Brief: BigMint’s flagship India steel composite index, a barometer of the domestic steel market, edged up by 0.2% w-o-w as assessed on 31 October 2025, marking a rare uptick amidst the sustained downtrend in the steel market and after a spell of 11 weeks of successive decline.

The post-Diwali resurgence of momentum in the steel market provided support to prices, with the long steel composite index inching up by 1.1% w-o-w. However, the flat index composite index fell 0.7%, showing sustained weakness amid weak global prices and trade sloth.

Highlights of price movements

IF rebar prices trend up: On a weekly basis, rebar prices surged by INR 100-1,700/t across regions except in south India such as Bangalore, Hyderabad, and Chennai, as per BigMint’s assessment.

The IF rebar market witnessed a positive trend this week supported by improved buying activity and better sales momentum. The market reflected positive vibes post-Diwali, with increased participation from traders and increased momentum in major projects which strengthened overall market sentiment. Smoother dispatches and lifting from buyers led to a reduction in inventory levels from around 15 days to nearly 10-12 days.

Trade-level blast furnace rebar prices, however, edged down w-o-w across major markets except in a few. Some primary mills either increased their discounts or reduced list prices owing to subdued market sentiments after Diwali. Inventories at mills rose slightly by around 15% in end-October, compared with levels seen at the beginning of the month, as per sources. This was majorly due to a slow domestic market during the festive season.

Flat steel prices soften further: Trade-level prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) showed a downtrend w-o-w. BigMint’s benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 300/t ($3/t) to INR 47,400/t ($538/t) on 28 October against INR 47,700/t ($541/t) on 17 October. CRC (IS513, Gr O, 0.9 mm/CTL) prices dropped by INR 300/t ($3/t) on 28 October to INR 55,000/t ($624/t) against INR 55,300/t ($627/t) as on 17 October. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Domestic HRC prices have edged slightly lower, while overall demand stays subdued amid limited trading interest. A source informed Bigmint, “Market participation remains thin as post-festive sentiment is still soft, with many participants yet to return fully to active trading”, resulting in a slow and quiet market mood.

India’s bulk imports of HRC touched 343,891 t as of 25 October, based on vessel line-up data. Bulk exports of HRC touched 291,034 t as of 25 October and around 35,000 t of additional cargo is in transit. BigMint’s India HRC (S275) export index for Europe fell by $5/t w-o-w to $540/t FOB main port. Notably, an unconfirmed deal was heard concluded for November shipment at slightly lower levels. The HRC (SAE 1006) export index for the Middle East and Vietnam remained stable w-o-w.

Outlook

The post-Diwali resurgence in steel market momentum and expectations of a pickup in infrastructure and construction activities will drive steel demand and trade. In the short term, steel market participants are largely in a wait-and-watch mode. The upcoming monthly price revisions to be announced by the leading mills will guide sentiment and set the trajectory for the domestic market.

Leave a Reply