- Gas shortage, drop in imports keep supply tight

- Billet prices decrease by INR 300/t w-o-w

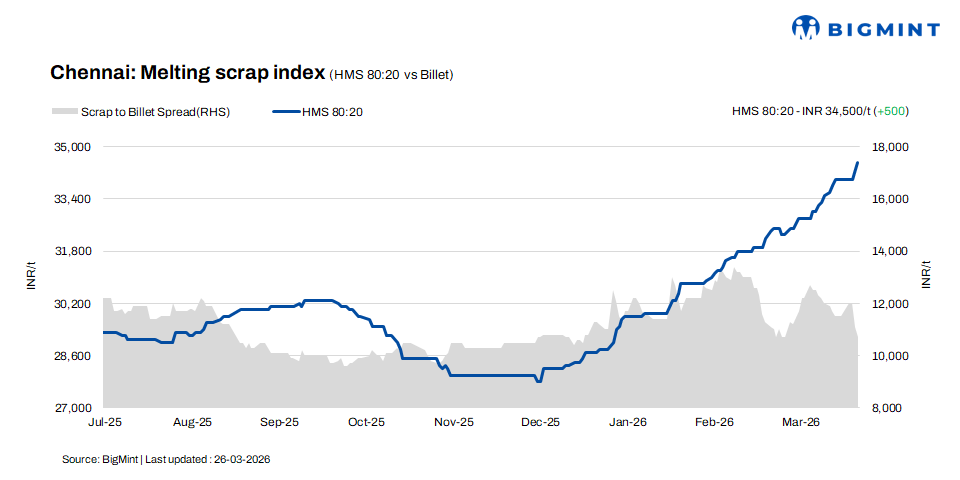

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai rose by INR 300/t day-on-day to INR 34,500/t, with a weekly increase of INR 500/t. Billet prices declined by INR 300/t w-o-w and edged down INR 100/t d-o-d to INR 45,200/t. In contrast, rebar prices increased by INR 300/t w-o-w to INR 50,500/t, with no change observed on a daily basis. The trend reflects mixed sentiment with steady support from finished steel demand.

Imported and domestic price trends

Market participants indicated that Australia origin imported shredded scrap was offered at $385-390/t CFR Chennai, while HMS (80:20) scrap was quoted at $365-370/t. Buyers were bidding $10-15/t lower. Buying interest remained subdued as the strengthening US dollar continued to push up landed costs, keeping buyers cautious about fresh imported scrap bookings.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 34,500-35,000/t for spot deals with immediate payment, while transactions on extended credit terms were concluded at INR 35,000-35,500/t. Overall, market activity remained largely concentrated within the INR 34,500-35,500/t range, with most trades being executed within this band, reflecting stable pricing with variations driven by payment terms.

Buyer-supplier sentiments

A mill representative noted that sponge iron prices have softened slightly, as supplies from neighbouring states are being offered at more competitive rates compared to local suppliers. At the same time, merchant sponge iron availability remains adequate in the market. Billet prices have declined in recent days due to liquidity constraints, as some major financiers have temporarily withheld funding ahead of financial year-end and book closure. Rebar demand remains strong from the project segment, while the retail segment continues to be slow. Overall, mill inventory levels are estimated at around 10-15 days.

A scrap supplier indicated that HMS (80:20) prices were currently hovering in the range of INR 34,500-35,500/t, with variations largely dependent on payment terms and mill-specific volume requirements. The ongoing commercial gas supply issue continues to disrupt scrap cutting and processing activities, thereby impacting overall ferrous scrap availability. Additionally, lower imported scrap bookings due to higher dollar rates have further tightened supply, contributing to the current shortage in the market.

Regional comparison

The Jalna market in western India witnessed mixed price movements, with billet prices declining by INR 300/t to INR 43,000/t, while rebar prices increased by INR 600/t to INR 51,600/t. Meanwhile, HMS (80:20) scrap prices remained stable at INR 33,000/t. Market participants reported a sense of panic following the announcement of restrictions on petrol and diesel sales, which led mills to raise their offers. However, finished steel demand remains moderate, and adequate scrap availability at mills has supported price stability.

Outlook

The Chennai scrap market is expected to remain firm with a slight upward bias. Domestic scrap prices are supported by tight supply conditions due to gas-related processing constraints and limited imported scrap bookings. However, moderate finished steel demand and cautious mill procurement may restrict sharp price movements.

Leave a Reply