- Liquidity crunch across steel value chain slows trade

- Billet prices fall INR 300/t w-o-w, rebar remains stable

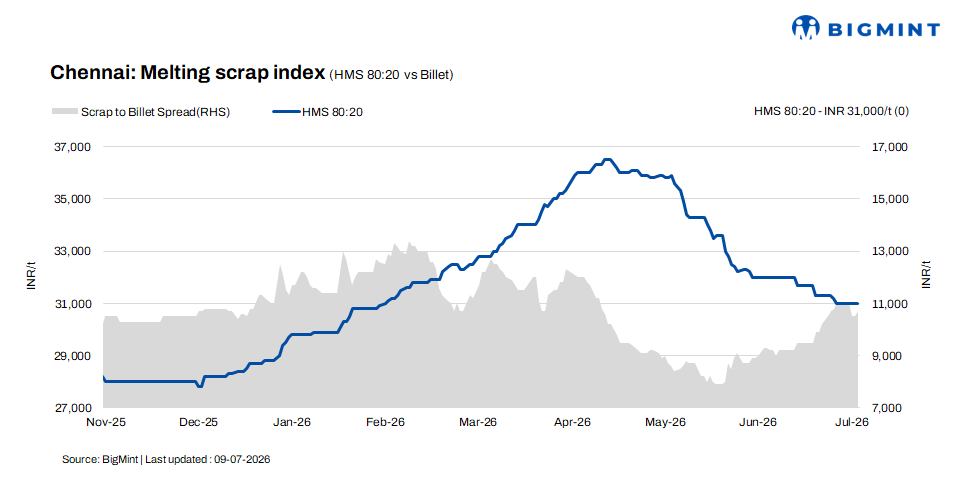

HMS (80:20) scrap prices in Chennai were assessed unchanged d-o-d and w-o-w at INR 31,000/t, according to BigMint’s latest assessment on 9 July 2026. In the semi-finished steel segment, billet prices inched up by INR 200/t to INR 41,700/t d-o-d, though they recorded a w-o-w correction of INR 300/t, reflecting subdued market sentiment. Similarly, rebar prices remained stable d-o-d and w-o-w at INR 45,800/t.

The stability in scrap prices contrasted with softer billet sentiment, as mills continued to procure raw materials cautiously amid weak finished steel demand and comfortable domestic scrap availability.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $365-370/t CFR Chennai, while HMS (80:20) was quoted at $345-350/t CFR. Buyers remained cautious, with bid levels trailing prevailing offers by around $15-25/t, resulting in a significant bid-offer gap. Despite the shortage of imported bookings, domestic scrap continued to remain the more economical procurement option, limiting buying interest for imported material and keeping import trade activity muted in the Chennai market.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 30,500-31,000/t for immediate payment deals, while transactions on extended credit terms were concluded at INR 31,000-31,500/t. Overall, market activity remained largely confined within the INR 30,500-31,500/t range, reflecting balanced supply despite subdued demand from the downstream steel sector.

Transaction prices continued to vary based on payment terms and mill-specific procurement volumes. With finished steel demand remaining weak, most mills maintained a cautious, requirement-based purchasing approach, limiting fresh scrap procurement and avoiding inventory build-up.

Buyer-supplier sentiments

A mill representative told BigMint that finished steel demand remains subdued, with buyers continuing to avoid bulk purchases and opting for need-based procurement. The representative added that trade activity has slowed since the previous month, as both infrastructure project demand and retail sales have weakened. The slowdown in these segments has reduced overall offtake, keeping market sentiment cautious and exerting pressure on finished steel demand.

A scrap supplier told BigMint that domestic HMS (80:20) scrap prices are currently hovering in the INR 30,500-31,500/t range, depending on payment terms and transaction volumes. The supplier further noted that liquidity pressure across the steel value chain has significantly reduced market activity, particularly in the finished steel segment. As a result, mills continue to procure scrap cautiously, purchasing material only against immediate production requirements while avoiding inventory build-up.

Regional comparison

In the western India-based Jalna market, billet prices declined by INR 600/t to INR 39,500/t, reflecting weak buying interest from downstream steel consumers. Similarly, rebar prices fell by INR 300/t to INR 44,000/t amid subdued demand in the finished steel segment. In contrast, HMS (80:20) scrap prices remained unchanged at INR 31,100/t, supported by balanced domestic scrap availability and cautious procurement by mills.

Market participants noted that rebar demand has remained weak over the past couple of weeks, resulting in price corrections in the finished steel segment. Despite subdued steel demand, a mild shortage of scrap continues to persist, prompting mills to increase sponge iron usage to around 30-40% of the charge mix. This strategy is helping producers manage raw material requirements amid constrained scrap availability and optimise production costs.

Outlook

The Chennai scrap market is expected to remain range-bound in the near term, as weak finished steel demand and liquidity constraints continue to weigh on buying sentiment. Mills are likely to maintain need-based procurement, while comfortable domestic scrap availability is expected to limit any sharp price recovery. Price movements are expected to remain within INR +/- 200-500/t.

Leave a Reply