- Rebar tags drop INR 500/t w-o-w, stable d-o-d

- Semi-finished steel prices remain stable w-o-w

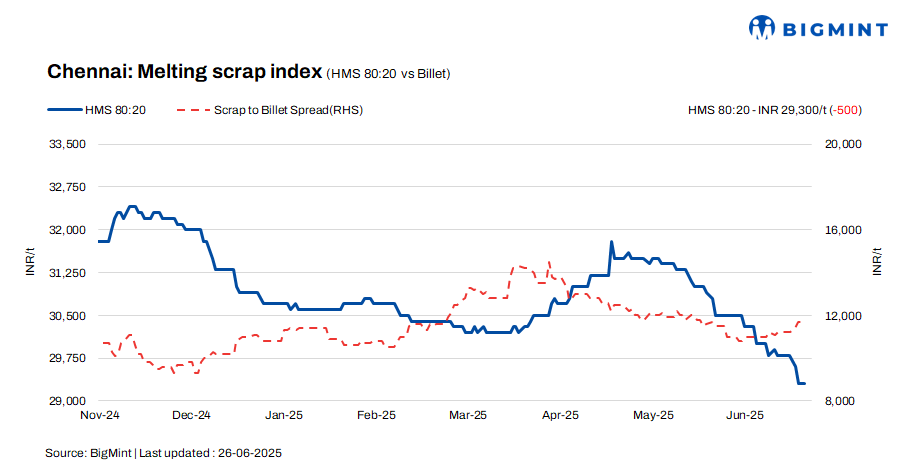

As per BigMint’s recent assessment, HMS (80:20) scrap prices in Chennai declined by INR 500/t on a weekly basis, settling at INR 29,300/t, while daily prices remained flat. Billet prices held steady at INR 41,000/t, showing no change in both daily and weekly trends. Meanwhile, rebar registered a similar weekly drop of INR 500/t to INR 46,000/t, though remained stable on a d-o-day basis, signaling continued weakness in downstream steel consumption and potential pressure on mill margins.

Imported, domestic price trends

A scrap trader informed that current offers for shredded scrap from Australia are at $350-355/t CFR Chennai, while HMS (80:20) offers are slightly lower at $330-335/t. Despite the lower price levels, mill interest in imported scrap remains subdued, primarily due to the availability of domestic scrap at comparable or lower prices. Additionally, domestic scrap offers the advantage of immediate availability, whereas imported material typically takes 15-30 days to arrive.

In the Chennai market, domestic HMS (80:20) scrap is being transacted at INR 29,000-29,500/t for immediate payment spot deals, whereas trades on extended credit terms are concluding slightly higher at INR 29,500-30,000/t. The prevailing trade band of INR 29,000-30,000/t highlights the influence of payment terms on price realization, with liquidity playing a crucial role in shaping deal closures.

Buyer-supplier sentiments

A mill representative informed BigMint that finished steel demand remains at a moderate level in the current market. Billet inflows from neighboring states have slowed due to lower price competitiveness compared to Chennai offers, resulting in firm demand and a slight shortage of locally sourced billets. Rebar demand also remains moderate, with mill inventory levels at around 10-15 days. Scrap availability is currently aligned with production needs, ensuring stable supply at the plant level.

According to a scrap supplier, HMS (80:20) is currently trading at INR 29,000-30,000/t, with pricing largely dependent on payment terms. A prevailing liquidity crunch has slowed trade activity in recent weeks. Rebar demand has weakened, prompting mills to lower scrap procurement prices to manage conversion costs. Additionally, some mills are reducing their domestic scrap purchases due to continued arrivals or existing stock of imported scrap at the ports.

Regional comparison

In the Jalna market of western India, billet prices have increased by INR 500/t, now standing at INR 39,800/t, While rebar prices improved by INR 800/t to INR 44,300/t. HMS (80:20) scrap prices remained steady at INR 30,500/t. The upward revision in steel prices is attributed to a recent hike in electricity costs by INR 1/unit, which has raised steel production costs by approximately INR 800-1,000/t. Scrap purchase prices have held firm, as suppliers are resisting lower offers amid tight availability.

Outlook

Sources indicate that scrap prices are likely to remain range-bound in the near term, with possible fluctuations of INR +/- 500/t. This relative stability is driven by continued uncertainty in the finished steel market, where both buyers and sellers are maintaining a cautious stance. The subdued sentiment is expected to keep scrap prices confined within a narrow band in the short run.

Leave a Reply