- Higher offers gradually gaining acceptance

- China market edges up but buyers remains cautious

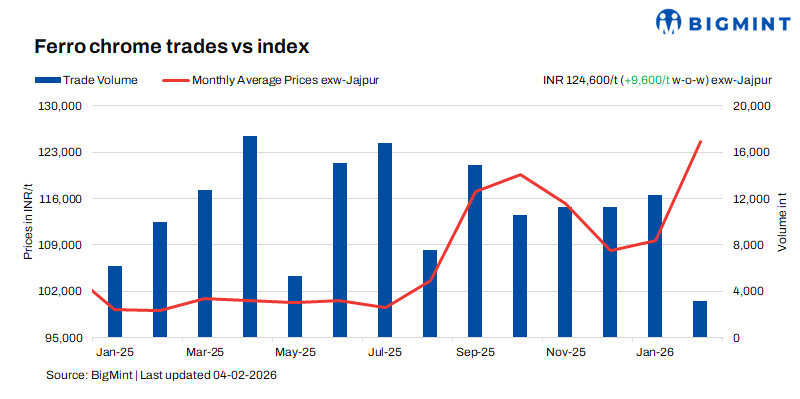

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices witnessed an increase of INR 9,600/t ($106/t) as compared to the previous assessment on 28 January 2026. Prices reached their highest point since September 2023 following high-grade material scarcity in the market and higher premiums at recent domestic auctions.

High-carbon ferro chrome (HC 60%, Si: 4%) prices in India were INR 124,600/t ($1,379/t) exw-Jajpur, as per BigMint’s assessment on 4 February. Around 5,500 t of deals were finalised last week within the price range of INR 117,500-126,500/t ($1,300-1,400/t) exw.

Low-silicon high-carbon and low-carbon (C:0.1%) ferro chrome prices too went up by INR 8,000/t ($89/t) and INR 4,500/t ($50/t) w-o-w to INR 130,000/t ($1,439/t) exw-Jajpur and INR 214,500/t ($2,374/t) exw-Durgapur, respectively.

Market highlights (29 January – 4 February)

Prices on the rise, buying sentiment mixed: In the domestic market, nearly four key ferro chrome suppliers, with a combined monthly production of around 40,000-45,000 t, remained out of the spot market due to export commitments, temporary plant closures, and limited availability of higher-grade chrome ore. This absence of material led to a noticeable supply crunch, prompting sellers to raise offer levels.

Initially, buying activity was muted as buyers resisted the sharp increase in prices. However, as the tight supply situation persisted, the market gradually adjusted to the higher offers and deals began to materialise at elevated price levels. Despite this, a degree of caution continued to prevail amongst both buyers and sellers, given the uncertain demand outlook. A key stainless steel producer told BigMint, “We’re not buying as market seems uncertain currently. Additionally, we have ferro chrome stocks to last till February end.”

China’s market scenario: Ferro chrome (HC60%) prices in China edged up by RMB 100/t ($14/t) w-o-w to RMB 8,900/t ($1,282/t) exw-Inner Mongolia. For HC50%, prices were at RMB 8,645/t ($1,245/t) exw-Inner Mongolia. Prices edged higher over the week, supported by firm chrome ore prices and rising smelting costs, though spot market activity remained muted as buyers awaited clearer price signals from major mills. The chrome ore market stayed strong, backed by higher futures and limited port inventories, which kept sellers holding firm on offers, particularly for South African concentrates. Despite some volatility in coking coal, chromium ore costs remained the key driver. In Inner Mongolia, increasing smelting expenses encouraged producers to maintain price support.

Meanwhile, downstream stainless steel demand recovered slowly, with mills consuming pre-holiday inventories. Spot transactions were largely limited to existing contracts, keeping the market cautious. In the near term, strong raw material costs are expected to support prices, while sluggish downstream demand may cap significant upside.

Stable end-user segment: Stainless steel prices for 304 grade CRC stayed steady, moving up slightly by INR 1,000/t ($11/t) w-o-w to INR 202,000/t ($2,235/t) exw-Mumbai. The strengthening Indian rupee dampened market sentiment, prompting buyers to adopt a cautious, wait-and-see approach. However, rising ferro alloy costs continued to lend support to prices.

Market participants indicated that while demand was moderately stable, import activity remained slow, with buyers hesitant to commit to large volumes. Some delayed cargoes from Malaysia were reportedly cleared after importers paid a 7.5% duty. Another participant highlighted persistent market volatility and weak demand, though noting that the India–US trade deal could open new opportunities for the pipes and tubes segment, supporting future demand. Globally, higher alloy costs have pushed mills to raise prices, offering near-term support despite uneven downstream demand.

Outlook

Ferro chrome prices in the coming week are expected to stay at similar levels, backed by firm offers from sellers.

Leave a Reply