- High import offers, subdued coal trade pressure freights

- GST reforms to lift landed costs, may curb fresh imports

Dry bulk coal freights softened this week, with major routes coming under pressure on the back of weak demand-supply fundamentals, higher import offers, and limited fixture activity, as noted by market participants. Apart from a few Australia–China fixtures reported by SAIL, activity on key lanes such as South Africa–India and Indonesia–India remained muted.

“Time charter (TC) sentiment is firming up, as owners remain optimistic on vessel demand and period employment. Bunker prices are easing, reducing voyage costs and providing some relief to operators. However, net spot/voyage freight earnings are marginally down, reflecting subdued cargo demand and limited fixture activity despite the supportive TC and fuel market trends,” a ship-broker observed.

Sources indicated that overall market confidence continued to erode. However, in the Pacific, operators and traders highlighted a notable uptick in fresh coal cargo inquiries.

Another source told BigMint, “Supramax freights in the Asia-Pacific showed a mixed trend, with limited trading activity heard on the Indonesia-India coal corridor.“

From South Africa, too, trading activity stayed muted as participants considered prevailing freight levels high, limiting purchases mainly to need-based requirements. Cautious industrial appetite also kept overall coal consumption in check.

India’s portside thermal coal inventories fell 7.1% w-o-w to 12.1 million tonnes (mnt) in Week 36 from 13.03 mnt in Week 35. Arrivals remained muted, as elevated import offers and higher freights pushed up landed costs, while subdued domestic demand further curtailed fresh bookings from traders and steelmakers.

Meanwhile, the upcoming GST revision and INR 400/t cess removal on coal are expected to push up landed costs, prompting traders to liquidate stocks ahead of the deadline while curbing fresh imports thereafter. This shift is expected to dampen coal trade flows into India, reducing spot inquiries and vessel demand.

Route-wise updates

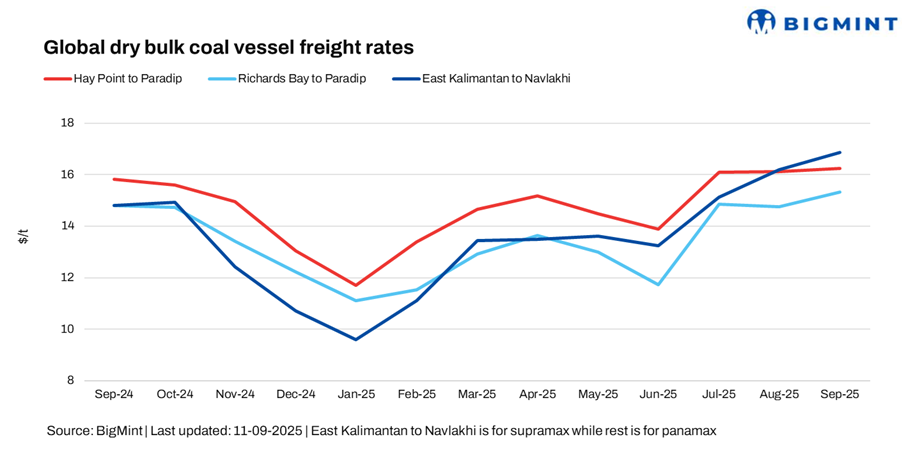

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India fell by around $0.26/dry metric tonne (dmt) w-o-w, with BigMint’s latest assessment placing the Hay Point-Paradip route at $16.12/dmt. “Panamax freights on the Australia-India route remained weak as participants adopted a wait-and-watch stance for clearer market cues. Cargo replenishment was sluggish at the start of the week, while freight derivatives traded in a narrow range during Asian hours, and bunker prices remained stable,” said a source.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route decreased by $0.25/dmt w-o-w to $15.20/dmt. Amid the prevailing uncertainty, no fresh fixtures were heard from South Africa during Asian trading hours.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route stood at $15.96/dmt, a significant drop of $1.79/dmt, w-o-w. “Asia-Pacific Supramax freights softened, with participants pointing to the usual slow start to the trading week. Limited activity and scarce cargo availability kept rates subdued in the Indonesian basin,” a source highlighted.

Market highlights

- Baltic index rises w-o-w on higher rates across vessels: The Baltic Exchange’s main dry bulk sea freight index continued its uptrend on 11 September 2025 amid higher rates across vessels despite overall muted market sentiments. The overall index increased sharply w-o-w by around 172 points to 2,112. Additionally, the Panamax segment also witnessed a significant hike of 256 points w-o-w to 1,975, while the Supramax segment increased by 11 points to around 1,478.

- DCE coal futures drop w-o-w: Coking coal futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract witnessed a w-o-w drop of RMB 6/t ($1/t) to RMB 222/t ($31/t) on 11 September. DCE coking coal futures fell this week, as lacklustre steel demand in China, ample portside inventories, and softening raw material prices weighed on sentiment. With mills curbing output amid poor margins and industrial slowdown, oversupply concerns eased, while parallel weakness in coke and iron ore further pressured futures.

Outlook

In the near term, coal vessel freights are likely to stay under pressure, as muted Indian demand, elevated landed costs from the GST hike/cess removal, and subdued cargo trading activity limit fresh fixtures, though occasional pre-deadline stocking or opportunistic cargoes may offer brief support; overall sentiment leans soft to range-bound across Indonesia–India and South Africa–India routes.

Leave a Reply