- Firm bunkers and weak demand kept rates range-bound

- Owner-charterer bid-offer disparity kept fixtures limited

Dry bulk coal freight rates to India remained supported on a w-o-w basis, despite sluggish market fundamentals and limited fresh fixture activity. The firmness in rates was largely sustained by tonnage positioning and steady cargo expectations, even as overall trading momentum and enquiry levels remained relatively subdued.

“Asia-Pacific Panamax freight rates trended mostly lower, with both the Pacific and Atlantic basins witnessing relatively subdued activity. Freight derivatives softened during Asian trading hours, while bunker prices edged slightly higher on a d-o-d basis,” a source told BigMint.

Another ship-operator noted, “Activity in the Indian Ocean was reported to remain largely lacklustre, with limited fresh cargo enquiries and subdued fixture momentum. Market participation stayed muted as both charterers and owners adopted a cautious stance amid uncertain demand visibility.”

Why dry bulk coal freight rates are under pressure?

- Baltic dry index drops w-o-w on soft demand: The Baltic Dry Index declined by 66 points w-o-w to 1,936 as of 05 February 2026, primarily weighed down by weakness in the Panamax segment, which fell by 57 points to 1,659 amid softer coal and grain trading activity. In contrast, the Supramax segment provided some support, rising by 40 points to 1,102, backed by relatively steady minor bulk demand and improved cargo availability in select regions.

- DCE coke futures fall w-o-w: DCE coke coal futures for May 2026 contract fell w-o-w by RMB 47.5/t ($6.9/t) to stand at around RMB 1,698.50/t ($244.8/t). DCE futures declined mainly due to weaker steel demand expectations, which dampened procurement interest from mills. Sentiment was further pressured by comfortable coke inventories at plants and ports, along with stable-to-soft coking coal prices reducing cost support.

- Rising bunker costs intensify pressure and heighten market concerns: Persistently elevated bunker prices continued to influence the vessel freight market this week, as higher fuel costs prompted owners to maintain a firm stance on rate expectations to safeguard voyage economics. The sustained strength in bunkers kept the bid-offer gap relatively wide, with owners resisting lower offers while charterers remained cautious, leading to slower fixture momentum across certain segments. The cost pressure has continued to provide underlying support to freight rates, particularly on longer-haul voyages, even as broader market sentiment stayed mixed.

Route-wise updates

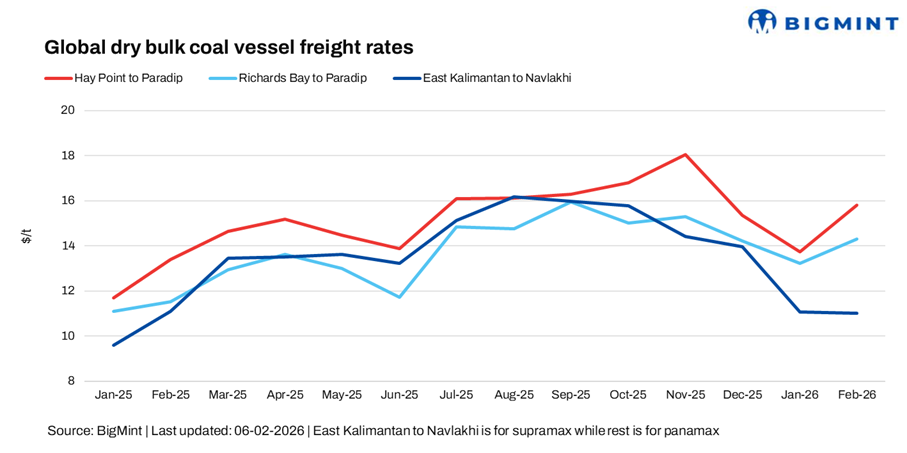

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up marginally by around 0.1/dry metric tonne (dmt) w-o-w to $15.1/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route stood unchanged w-o-w at $14.2/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood flat at around $11/dmt. Indonesian miners have paused spot coal exports following the government’s proposal for steep production cuts, leaving Asian buyers struggling to secure supplies from the world’s largest exporter. According to a shipbroker active on the route, “spot shipments are unlikely to resume this quarter unless Indonesia relaxes the proposed output curbs.”

Outlook

In the near term, dry bulk coal freight rates to India are expected to remain relatively supported, underpinned by firm bunker prices and balanced vessel availability in key loading regions. Owners are likely to maintain a strong rate stance to offset elevated voyage costs, which could keep freight levels from softening sharply despite moderate cargo enquiry levels.

However, overall rate momentum may remain range-bound as coal demand visibility stays mixed, with seasonal buying patterns and cautious procurement by utilities and traders limiting strong upside. Market direction will largely depend on fresh cargo emergence from Indonesia, South Africa and Australia, along with movements in bunker prices and tonnage supply across the Indian Ocean basin.

Leave a Reply