- Weak demand, ample vessel supply weigh on prices

- Cautious Chinese buying, seasonal lull impact Capesize market

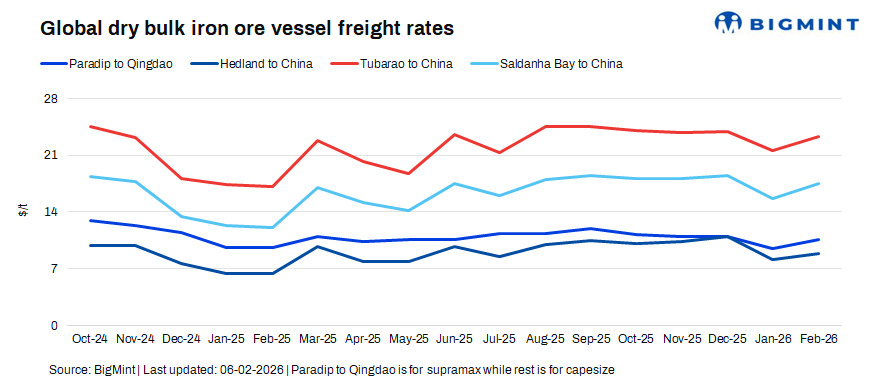

Dry bulk iron ore freight rates exhibited mixed trends during the week, reflecting a combination of softer cargo demand and rising vessel availability. Capesize freight markets weakened as iron ore shipment volumes from key exporting regions- Australia and Brazil-slowed, with miners showing limited urgency to fix tonnage amid stable inventories and muted price signals.

India-China Supramax freight rates edged higher due to steadier regional cargo demand and tighter vessel availability in the Indian Ocean, which helped absorb prompt tonnage. Unlike Capesize markets, the Supramax segment benefited from diversified minor bulk flows and shorter-haul trades, allowing owners to maintain firmer rate resistance despite broader weakness in iron ore freight.

On the demand side, Chinese steel mills adopted a cautious procurement strategy, supported by comfortable port stocks and narrowing steel margins. The absence of aggressive restocking, coupled with seasonal disruptions around the Lunar New Year, curtailed spot market activity and reduced fixture volumes on major iron ore routes such as Brazil-China and West Australia-China.

Meanwhile, the supply side remained heavy, with increased ballasting and prompt tonnage availability in the Pacific and Atlantic basins intensifying competition among shipowners. This imbalance exerted downward pressure on voyage rates and time charter equivalents, particularly for long-haul Brazil trades, where limited fresh cargoes struggled to absorb available vessels.

Adding to the cautious sentiment, weaker iron ore futures and a softer broader commodities complex weighed on charterers’ appetite to commit at higher levels. Although occasional cargoes provided brief support, they were insufficient to offset the broader softness in fundamentals.

Overall, iron ore freight rates trended lower w-o-w, constrained by subdued demand, seasonal factors, and oversupply of tonnage, keeping the Capesize segment under pressure despite relative stability in smaller dry bulk segments.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China gained by $0.5/dry metric tonne (dmt) w-o-w to $10.5/dmt on 6 February.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China decreased by $0.7/dmt w-o-w to $8.3/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments dropped by $0.8/dmt w-o-w to $23.5/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao remained stable w-o-w to $17.4/dmt.

Market highlights

- Baltic index drops w-o-w: The Baltic Dry Index dropped by 66 points w-o-w to 1,936 on 05 February, driven by weaker dry bulk cargo demand, cautious chartering activity, and increased vessel availability across key segments.

- Brent crude futures down w-o-w: Brent crude oil futures dipped about $2/bbl w-o-w to $68.4/bbl for the April 2026 contract on 06 February, pressured by demand-side concerns, easing geopolitical risk premiums, and expectations of ample global supply.

- DCE iron ore futures fall w-o-w: Iron ore futures on the Dalian Commodity Exchange slipped by RMB 31/t w-o-w to RMB 760.5/t on 06 February, amid softer steel demand outlook, high port inventories, and cautious buying from Chinese mills.

Outlook

Iron ore freight rates are likely to remain under pressure in the near term, as subdued cargo demand and seasonal factors continue to outweigh any support from producers. Chinese mills are expected to maintain a cautious procurement approach amid high port inventories and weak steel margins, limiting restocking activity after the Lunar New Year. At the same time, ample vessel availability-particularly in the Capesize segment-will keep competition among owners intense, capping any upside in rates. While occasional cargoes may offer brief support, a sustained recovery in iron ore freight is unlikely until steel demand and chartering confidence show clearer signs of improvement.

Leave a Reply