- Panamax supported by firm Australia fixtures, tighter vessel supply

- Supramax stays soft amid slow cargo movement, limited enquiries

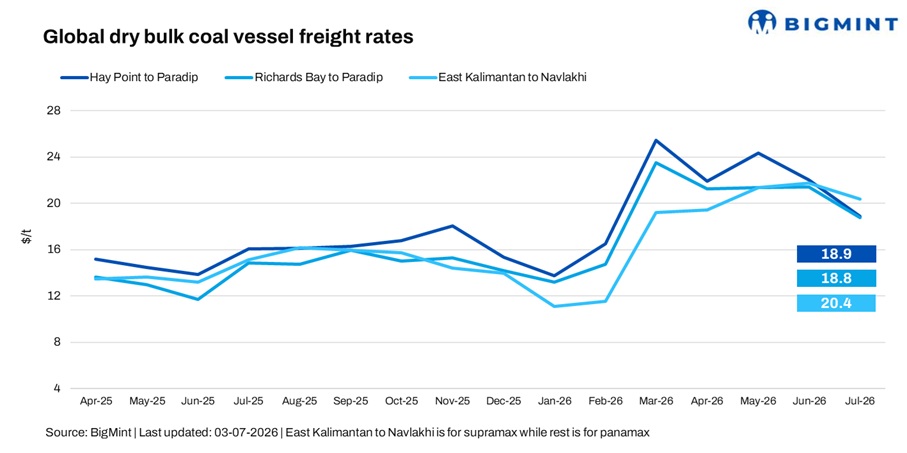

India’s dry bulk coal freight market witnessed mixed trends in the week ended 3 July 2026. Firm Australian coal fixtures and tightening prompt vessel availability lent support to Panamax rates, while slower cargo movement from South Africa and Indonesia continued to weigh on select trade routes.

Panamax sentiment improved modestly during the week, supported by stronger fixture levels out of Australia and a gradual reduction in prompt tonnage as vessels shifted towards the Atlantic basin. Despite these positives, limited fresh cargo enquiries in the Pacific kept the overall recovery measured.

A shipbroker told BigMint, “Market sentiment remains positive, supported by improved enquiries, although participants continue to monitor fresh cargo flows.”

Meanwhile, Supramax sentiment remained slightly softer as slow coal movement from Indonesia and wider bid-offer gaps kept market participants cautious.

Another shipbroker said, “Market sentiment is slightly on the softer side as overall activity remains slow. However, a few additional cargo orders entering the market are providing some support to freight levels.”

Route-wise update

Market highlights

- Baltic Dry Index (BDI) rises w-o-w: The BDI increased by 2.3% (59 points) w-o-w to 2,650, compared with 2,591 a week earlier, supported by improving sentiment across larger vessel segments. The Panamax index rose by 4.7% (99 points) to 2,195, driven by tighter prompt tonnage availability and stronger Atlantic demand, while improved Australian and North Pacific activity supported Pacific sentiment. Meanwhile, the Supramax index edged down by 0.2% (3 points) to 1,675, as weaker cargo availability in Asia offset firmer Atlantic activity.

- Bunker prices decline w-o-w: Bunker prices fell by $52/tonne (t) w-o-w to $661/t as of 3 July, compared with $713/t a week earlier, amid softer fuel oil values and easing crude oil prices as geopolitical risk premiums moderated and energy market sentiment weakened.

- Brent crude futures edge lower w-o-w: Brent crude oil (September 2026 contract) was assessed at $71.74/barrel (bbl) on 3 July, down $1.04/bbl w-o-w from $72.78/bbl a week earlier, as easing geopolitical concerns and adequate supply expectations continued to weigh on prices, while cautious global demand sentiment kept crude markets under pressure.

- DCE coke futures edge lower w-o-w: Coke futures on the Dalian Commodity Exchange for the September 2026 contract slipped to RMB 1,938/t ($285.46/t) as of 3 July, compared with RMB 1,946/t ($286.01/t) a week earlier. The marginal decline reflected cautious market sentiment amid subdued steel demand, weak coke fundamentals, and uncertainty surrounding China’s steel production outlook.

Outlook

Coal freight rates to India are expected to remain range-bound in the near term, with mixed regional fundamentals shaping market direction. Firm Australia activity and tighter vessel availability may continue to support Panamax rates.

However, slower Indonesian cargo movement and muted South African enquiries could keep overall sentiment under check. Market participants remain watchful of fresh cargo demand and tonnage availability in the coming weeks.

Leave a Reply