- MS Billet prices fell by INR 1,000-1,500/t w-o-w in Hyderabad and Chennai

- Scrap prices edged up slightly in Chennai due to supply constraint

Raw material (Sponge Iron & Melting scrap) Price movement :

Sponge iron prices in the Bellary cluster declined marginally by around INR 300/t w-o-w, with the current prevailing levels assessed at approximately INR 26,200/t ex-Bellary. The correction is primarily attributed to subdued demand from steel manufacturers, who have been operating cautiously amid moderate order inflows in finished steel.

Additionally, a slight softening in iron ore pellet prices provided limited cost relief to DRI producers, which also reflected in the downward price adjustment. Market sentiment remained relatively slow, with most buyers procuring only based on immediate production requirements rather than bulk stocking.

Melting scrap prices in the Chennai cluster moved up slightly during the week, supported by limited availability of material in the domestic market. Tight supply conditions kept spot prices firm despite moderate buying activity.

Additionally, lower import bookings by steel manufacturers increased their reliance on domestic scrap procurement, which further supported the positive price movement. Overall, market sentiment remained steady with a mild upward bias.

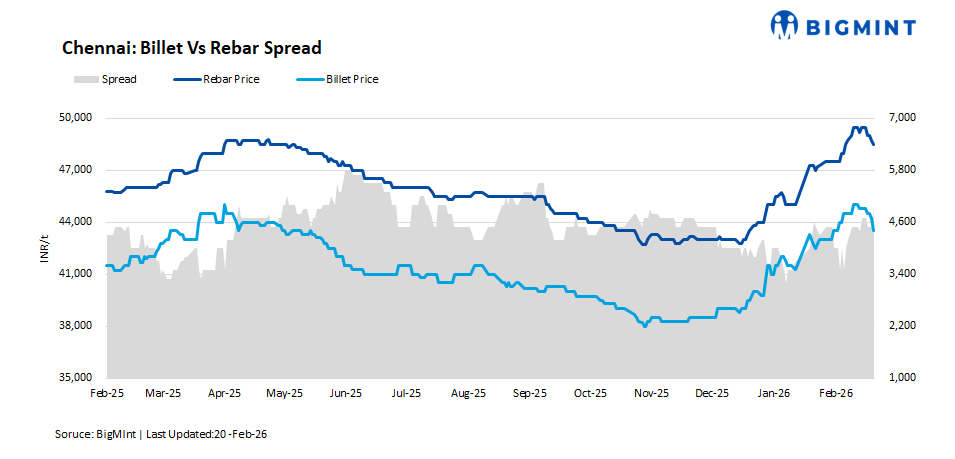

Semi-finished price trends :

Steel billet prices in South India declined sharply by around INR 1,000-1,500 per tonne in the Hyderabad and Chennai regions during the week. The correction was largely driven by sluggish offtake in finished steel segments, as demand from end-users and construction activity remained moderate. Mills reported slower order conversions, which weighed on overall market sentiment.

Additionally, competitive pricing from neighbouring markets exerted further pressure on local suppliers. In order to remain competitive and stimulate buying interest, billet manufacturers were compelled to trim their offers. The overall trend reflected a demand-driven correction amid cautious procurement and heightened regional competition.

Finished Steel Scenario:

Induction route rebar prices declined by around INR 1,000/t across major locations in South India, primarily due to limited demand and cautious buying from the distributor and retail segments. Market participants adopted a need-based procurement strategy, resulting in slower booking activity during the week.

In the Hyderabad cluster, trading activity remained particularly subdued owing to local factors and the festive occasion of Maha Shivaratri, which kept many market participants inactive and led to minimal fresh bookings.

Meanwhile, blast furnace (BF) route steel prices were assessed at around INR 57,500–58,000/t ex-works in key southern locations. The price gap between induction furnace and blast furnace producers continued to widen steadily, reflecting differences in cost structures and demand positioning.

Leading steel manufacturers continue to offer induction route rebars in the local market at prevailing price levels, although selective discounts are being extended in offers to attract buying interest of customers :

Outlook :

In the near term, steel prices in South India are likely to witness slight support, driven by expectations of improved finished steel demand and rising input costs such as melting scrap and non-coking coal.

The widening price gap between blast furnace and induction route rebar, along with steady project demand for blast furnace route material, may indirectly lend support to induction route prices as well, helping maintain overall market stability.

Leave a Reply