- Middle Eastern exporters keep offers on hold amid shipping route disruptions

- Indian buyers cautious amid lack of clarity on market direction, Holi slowdown

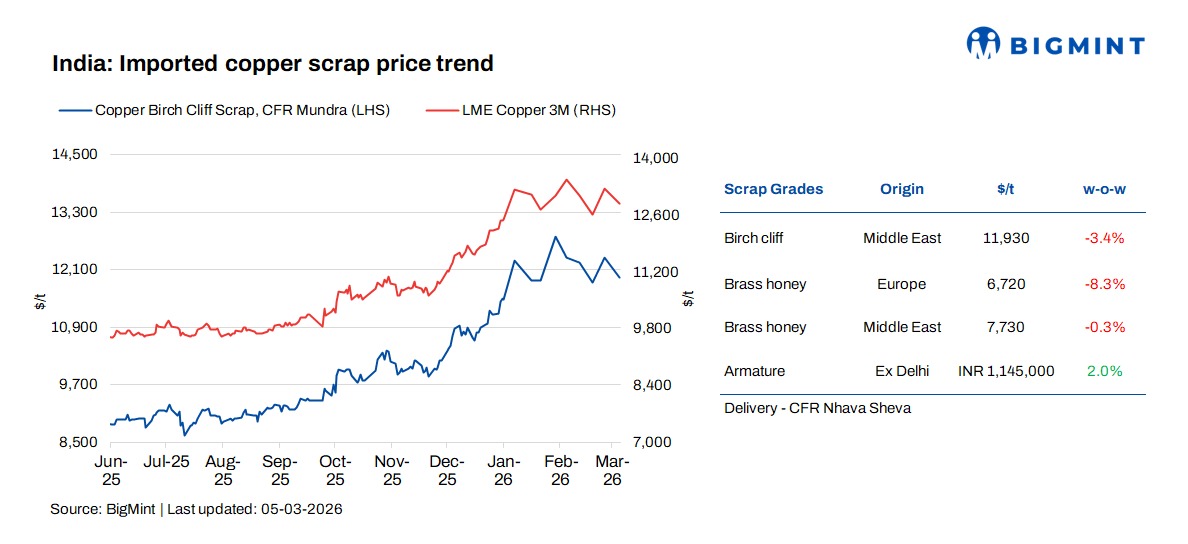

Imported and domestic copper scrap prices in India showed mixed trends w-o-w in a narrow range on 5 March amid a slight drop in London Metal Exchange (LME) prices and cautious sentiment due to the conflict in the Middle East. Offers from the Middle East region remained stable but were limited.

Copper prices on the London Metal Exchange (LME) declined by 1.9% w-o-w to $13,050/tonne (t) on 5 March from $13,300/t on 26 February.

Copper armature scrap prices were assessed at INR 1,145,000/t, an increase of 1% w-o-w, Imported offers remained range-bound, with Millberry from Europe heard at 97% of three-month LME futures, Candy Berry at 95%, and Birch Cliff at 90.5-91%. There was a lack of clarity on offers from the UAE, with Birch Cliff last heard at 92.75%. EU meatballs 21% from the EU were heard at $2,450/t CIF Mundra.

Market insight

India’s imported copper scrap market remained uncertain as the ongoing Iran conflict disrupted key shipping routes across the Middle East. Several shipping lines have either suspended or rerouted cargo movements through critical corridors such as the Strait of Hormuz and the Red Sea, prompting exporters in Middle Eastern countries to temporarily hold shipments. As a result, many suppliers adopted a wait-and-watch approach, putting export offers on hold and complicating price discovery in the scrap market.

Meanwhile, buyers stayed cautious and avoided fresh purchases. Many participants believe that ongoing geopolitical tensions, including the Iran-related conflict risks affecting shipping routes, could eventually pressure global metal prices upward. As a result, buyers preferred to wait for clearer direction before committing to new cargoes. Despite this sentiment, copper prices remain relatively strong and physical availability is comfortable in the domestic market, indicating no immediate shortage of material.

Meanwhile, several sellers are actively trying to move material, anticipating that prices could rise further. Market participants are closely monitoring potential policy support from China, where authorities have been signalling additional economic stimulus measures to support manufacturing, infrastructure spending, and property-sector stabilisation. Such measures typically support copper demand since China accounts for roughly half of global consumption, often pushing prices upward when stimulus expectations strengthen.

Domestic activity also remained slightly slow this week due to the Holi festival. Some processors and yards reported temporary labour shortages, which reduced operational activity and kept spot market trading limited. Overall, the market is currently in a wait-and-watch phase, with participants closely tracking global developments and policy signals from China.

Copper scrap imports

India’s copper scrap imports surged 15% m-o-m in January 2026 to 35,042 tonnes (t) from 29,750 t in December 2025, as per BigMint data.

US led scrap inflows but sourcing diversified. Volumes from the United States declined marginally by 1% to 8,596 t, indicating stable trade flow, while Germany fell 4% to 2,522 t, likely due to limited spot availability or shipment rescheduling. Imports from Saudi Arabia surged 91% m-o-m to 6,234 t from 3,270 t, likely due to large cargo arrivals and improved shipment scheduling from Middle East suppliers after year-end slowdowns. The United Kingdom also recorded a strong 36% rise to 2,464 t, possibly reflecting deferred December shipments clearing in January.

Global refined copper production rises 4% in CY’25

Global refined copper production climbed up by 4% y-o-y in CY’25. The growth in global refined copper production during the CY’25 was primarily driven by China and the Democratic Republic of Congo (DRC), which together account for around 57% of global output and recorded a combined increase of about 9% (China +9.4%, DRC +7.8%). Excluding these two countries, world refined copper production declined by approximately 1.8%.

In Asia (excluding China), refined copper output is estimated to have decreased by 3.7%, mainly due to lower production in Japan and the Philippines.

As per ICSG, India recorded a 19% increase in refined copper production, supported by improved operating capacity rates and the ramp-up of the Adani refinery.

Chilean refined copper production declined by 10%, with electrolytic output (from concentrates) down 16% due to smelter maintenance shutdowns, and electrowinning (SX-EW) production decreasing by 6.8%.

Global secondary refined copper production (from scrap) increased by 5.8%, largely driven by growth in China.

Outlook

The Indian copper market is expected to remain cautious in the near term as buyers stay hesitant amid geopolitical tensions and elevated LME prices. However, physical availability remains comfortable, limiting sharp downside risks. Market activity may gradually improve after the Holi slowdown, while China’s policy stimulus signals and global supply dynamics will continue to influence price direction.

Leave a Reply