- Higher substrate costs push mills to raise list prices

- Tight supply of thinner gauge material supports price hike

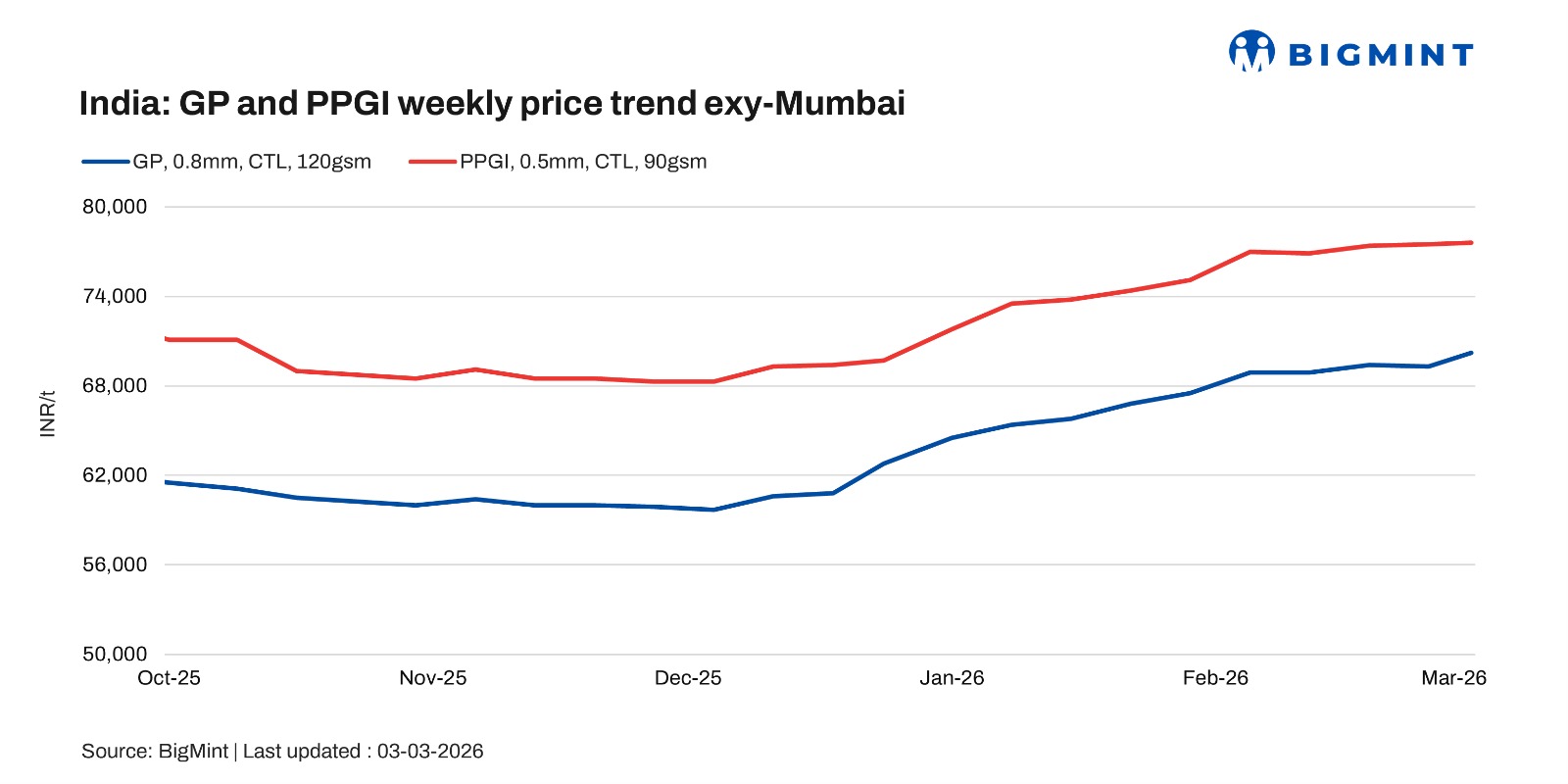

Indian coated flat steel prices increased w-o-w in early March 2026, supported by recent list price revisions from mills and slightly improved trade sentiment across galvanised plain (GP), pre-painted galvanised iron (PPGI), and galvalume (BGL) segments. Mills increased list prices by INR 750-1,500/t for March dispatches, largely in line with higher substrate costs.

Market momentum improved marginally; however, demand recovery remained below expectations. Buying activity continued to be largely need-based, with distributors and end-users cautious in building fresh inventories. That said, sentiment may improve in the near term if offtake strengthens and price stability persists.

Price updates

As per BigMint’s latest assessment, coated flat steel prices in the Mumbai market climbed higher on 5 March 2026.

GP coil prices increased by INR 900/t w-o-w to INR 70,200/t exy-Mumbai. Market offers were largely reported in the range of INR 69,500-70,500/t, reflecting improved realisations despite cautious trade sentiment.

PPGI prices rose marginally by INR 100/t w-o-w to INR 77,600/t exy-Mumbai. Offers were mostly heard in the range of INR 77,000-78,000/t, as mills maintained a firm pricing stance amid moderately strong buying interest.

Meanwhile, BGL prices moved up by INR 200/t w-o-w to INR 81,200/t exy-Mumbai. Market offers were reported in the range of INR 80,500-82,000/t, supported by relatively tight availability, although regional demand conditions remained mixed.

All prices are exclusive of 18% GST.

Hot-dip galvanised iron (HDGI) export offers remained stable w-o-w at $770/t as of 26 February 2026, reflecting continued cautious buying interest despite firm underlying mill pricing.

Market updates

Demand remained steady to slightly slow during the assessment period, although some momentum was observed following recent mill-led price hikes. Buying interest in the western and northern regions improved modestly, primarily driven by expectations of further price increases. This resulted in a short-term procurement push, largely speculative in nature. However, overall transaction volumes remained measured.

Inventory levels in the western and northern regions were reported at around 30-35 days, indicating relatively balanced stock positions. In contrast, the southern region continued to face slower demand conditions, with inventory levels elevated at approximately 55-60 days. As a result, purchases in the south remained largely need-based, and sentiment stayed subdued.

Across regions, tight availability of thinner gauge material provided underlying support to prices. While mills’ recent price hikes lent temporary momentum to the market, participants indicated that material movement, though improved, remains cautious.

Market participants are also closely monitoring ongoing geopolitical developments, as escalating war-related tensions have added a layer of uncertainty to global commodity and raw material markets. While no immediate disruption has been observed in domestic trade flows, participants remain watchful of potential volatility in the coming weeks.

Raw material price movements

On the raw material front, domestic zinc prices corrected from recent highs. Zinc ingot (99.995%) prices were assessed at INR 3,29,000/t as per the latest assessment, down from INR 3,37,000/t reported earlier. Despite the correction, zinc levels remain relatively elevated, providing underlying cost support to coated flat steel.

At the trade level, flat steel prices strengthened m-o-m in March 2026. HRC prices increased by INR 750/t to INR 54,500/t compared with INR 53,750/t in February. Meanwhile, CRC prices rose by INR 800/t to INR 60,500/t from INR 59,700/t during the same period.

On a w-o-w basis, BigMint’s benchmark (bi-weekly) HRC assessment increased by INR 800/t to INR 54,500/t as of 3 March against INR 53,700/t in the previous week. CRC prices were assessed at INR 60,500/t, up by INR 1,000/t w-o-w from INR 59,500/t. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Outlook

As per market assessment, recent price revisions and controlled mill supplies have strengthened the overall tone in the coated flat steel segment. Short-term restocking was observed in the western and northern regions amid expectations of further hikes, while elevated inventories in the south continue to cap aggressive buying.

Going ahead, price sustainability will depend on an improvement in actual consumption. If demand traction strengthens and inventories ease, particularly in the southern region, mills may attempt further increases. However, in the absence of steady offtake, prices are likely to consolidate within a narrow range in the near term.

Leave a Reply