- Automotive, renewable sectors see limited activity

- Prices to drift lower in absence of demand triggers

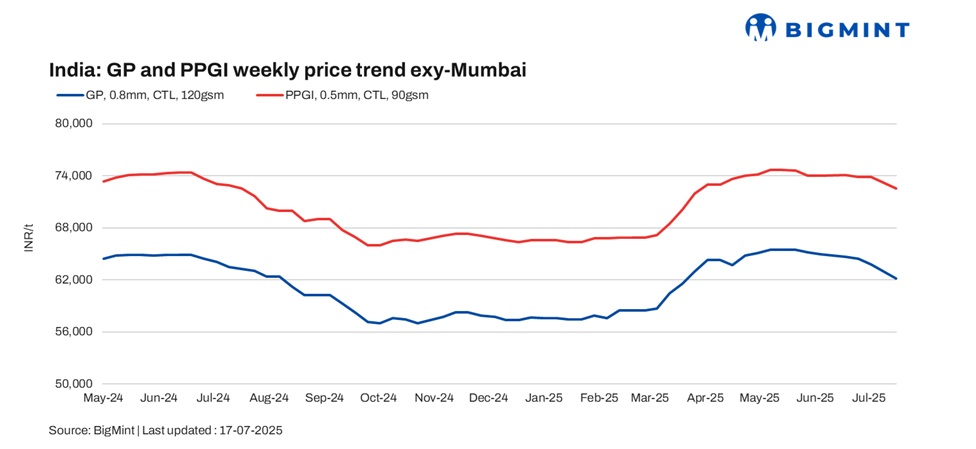

India’s coated flat steel market extended its decline through mid-July, driven by subdued demand, monsoon-related disruptions, and constrained logistics. Market sentiment remained weak across regions, with trade activity slowing and expectations building for further downward adjustments in the near term.

Market sources stated that while official mill prices have remained largely unchanged, flexibility in negotiated deals is being observed at the trade level, particularly for cut-to-length (CTL) material.

The latest weekly assessment on 17 July showed galvanised plain (GP) coil (0.8 mm/CTL, 120 gsm, IS277) prices at INR 62,200/tonne (t) ($722/t) exy-Mumbai, down INR 1,000/t ($12/t) w-o-w, with offers ranging between INR 61,800-62,700/t ($718-728/t).

Meanwhile, pre-painted galvanised iron (PPGI, 0.5 mm/CTL, 90 gsm, IS14246) was assessed at INR 72,600/t ($843 /t) exy-Mumbai, with offers hovering between INR 72,000-73,000/t ($836-848/t). Prices are exclusive of 18% GST. (USD 1 = INR 86.0719) (INR 1 = USD 0.11618632)

Market overview

Market sees muted demand, deferred purchases: Trading activity remained subdued across major markets, as buyers deferred procurement in expectation of further price corrections. Distributors highlighted a notable decline in transaction volumes, with downstream demand from key consuming sectors such as appliances, construction, and infrastructure remaining below expectations.

“Overall activity is limited, and there is no urgency to buy material among end-users,” a west India-based distributor noted.

Auto sector demand slows as production declines: Coated steel demand from the automotive sector remains under pressure. Despite steady OEM-level sales, production has slowed as manufacturers adjusted output to manage inventory. According to SIAM data, June 2025 production declined by 8.2% m-o-m.

Automotive-grade coated steel procurement has been limited, with Tier-1 and Tier-2 vendors cautious amid lacklustre retail movement and muted replacement demand.

Renewable energy sector remains weak: The renewable energy segment continues to face headwinds, reflecting broader weakness in coated steel consumption. Activity in July showed a w-o-w decline of 1-4%, as monsoon-related delays and subdued project momentum impacted demand for GP and PPGI products.

Steel consumption from solar and wind projects remains restrained, with engineering, procurement, and construction (EPC) firms operating at reduced capacity due to weather and pricing uncertainty.

Outlook

Coated flat steel prices are likely to remain under pressure in the near term amid weak demand, seasonal disruptions, and cautious buying. With no immediate recovery in end-user sectors and logistical constraints persisting, prices may soften further by INR 500-1,000/t. A potential demand revival post-monsoon could offer limited support, but near-term sentiment remains bearish.

Leave a Reply