- Pacific coal freights to India remain soft

- Atlantic rates stay relatively firm

Coal freight rates to India showcased mixed trends in the Pacific this week, with no major fixtures recorded as improving vessel availability and weaker regional sentiment pressured levels. In contrast, the Atlantic market remained firm, supported by stronger export offers and tighter tonnage lists that kept owners in a stronger negotiating position. Overall, the market continued to reflect a split trend, with declining Pacific rates partially offset by steady Atlantic strength.

“Asia-Pacific Panamax freight rates slipped as shipowners turned cautious, with limited cargo volumes from Indonesia and Australia and ongoing tropical storm disruptions further tightening vessel availability and weighing on sentiment,” a source said.

Coal freight rates on the Australia-India route continued to decline, pressured by weak demand from Indian steel producers who stayed inactive amid soft domestic steel consumption and ample supply. Market activity thinned as most buyers adopted a wait-and-watch stance, leaving SAIL as the only steady participant. With muted procurement and comfortable availability, overall sentiment remained subdued.

Freight rates on the South Africa-India route continued to edge higher this week despite the absence of major fixtures. South African thermal coal prices at Indian ports held firm w-o-w amid tight supply. Even as overall Indian coal demand stayed weak, a recent uptick in sponge iron prices boosted buying interest for select South African coal grades.

Supramax rates on the Indonesia-India route inched up w-o-w, but underlying activity remained subdued, with only a handful of fixtures and minimal new inquiries from Indian buyers. According to a ship operator, fixing information on the route was “fairly limited,” underscoring muted sentiment. Improving vessel availability also capped any meaningful upside, keeping the market’s tone soft despite the nominal rate increase.

Higher bunker costs add further pressure: Bunker prices have inched higher in recent sessions, adding fresh cost pressure for shipowners across major trading regions. The uptick tracks firmer crude oil sentiment, with Brent crude futures rising w-o-w by about $0.94/bbl to $63.17/bbl on 28 November, lifting marine fuel benchmarks alongside. Tightness in certain bunker hubs also contributed to the increase, raising operating expenses – particularly for longer-haul voyages. The rise in bunker costs has added another layer of pressure to freight economics, weighing on sentiment in an already cautious market.

Freight market split as demand-supply favours Atlantic over Pacific: The freight market displayed a clear split this week, shaped by contrasting demand-supply dynamics across the basins. In the Pacific, abundant vessel availability and inconsistent Indian coal procurement created an oversupplied environment, pushing rates lower and weakening owners’ bargaining power. Meanwhile, the Atlantic basin benefited from tighter tonnage lists and steadier export interest, allowing rates to hold firm despite limited fixtures. This divergence underscores how regional demand-supply balances continue to dictate freight direction, with the Atlantic maintaining support while the Pacific remains under pressure.

Route-wise updates

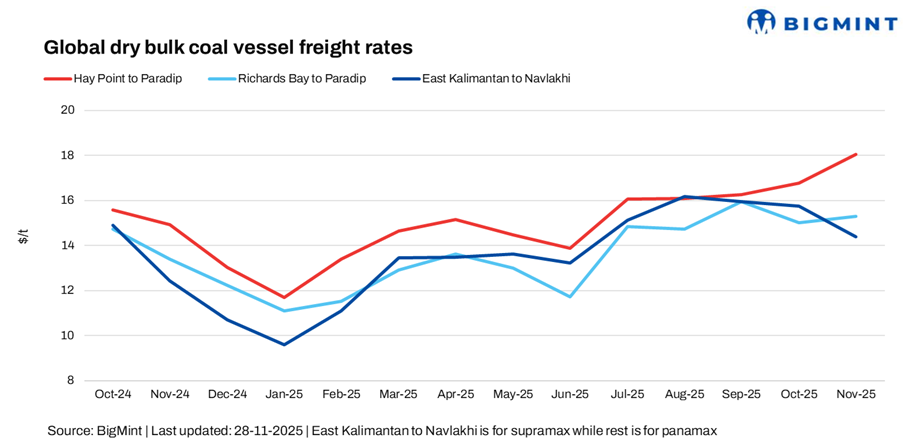

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India fell w-o-w by around 0.18/dry metric tonne (dmt) to $18.07/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route edged up w-o-w by $0.13/dmt to $16.03/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $14.50/dmt, an increase of $0.46/dmt, w-o-w.

Meanwhile, the Baltic Exchange’s dry bulk index for Panamax and Supramax vessels increased this week, with the Panamax index rising 50 points w-o-w to 1,962 and the Supramax index rising 2 points to 1,437. The w-o-w rise was supported by firmer Atlantic grain demand, selective coal and minor bulk inquiry in Asia, and tightening tonnage in key regions, which helped lift Panamax and keep Supramax rates slightly positive.

Outlook

Coal freight rates to India are likely to stay rangebound to mildly soft in the near term as Indian buying remains uneven and vessel availability in the Pacific stays comfortable. Limited spot demand on Indonesia–India and Australia-India routes continues to cap owners’ leverage and restrict rate upside.

The Atlantic market may hold relatively firm on tighter tonnage, but this strength is unlikely to lift the broader market without a pickup in Indian procurement. Overall, India-bound coal freights should remain steady to soft, with any meaningful change hinging on improved demand or a sudden tightening in vessel supply.

Leave a Reply