- Supply disruptions fuel rally despite muted utility coal demand

- Spot prices rise while utilities stay comfortably stocked

China’s domestic thermal coal market has staged its strongest recovery in nearly three months, lifting prices across major producing regions and northern ports after a prolonged period of weakness. At first glance, the rebound appears to signal the start of a stronger summer market, supported by tightening prompt supplies and improving sentiment.

However, a closer examination reveals that China’s thermal coal market is no longer moving as a single market. Instead, it is increasingly operating at two different speeds. While traders have turned increasingly bullish amid supply disruptions and tighter spot availability, power utilities remain largely on the sidelines, relying on long-term contracts and comfortable inventories rather than chasing rising spot prices.

The growing disconnect suggests that the recent recovery is being driven more by temporary supply constraints than by a broad-based improvement in coal consumption. Whether these two markets eventually converge will determine if the current rally develops into a sustained recovery or fades as another short-lived sentiment-driven rebound.

Key takeaways

- China’s thermal coal rally is being driven primarily by supply-side disruptions rather than stronger end-user demand.

- The market is increasingly splitting into two distinct segments–an active spot market led by traders and a well-supplied utility market showing little urgency to buy.

- Safety inspections, weather disruptions and lower rail arrivals have tightened prompt coal availability and improved market sentiment.

- Unless prolonged summer heat materially increases electricity demand and accelerates inventory drawdowns, the recovery could struggle to sustain itself.

Supply disruptions have shifted market sentiment

The latest rally has been built almost entirely on developments at the supply end of the market.

Northern port prices strengthened steadily during the second week of July as rail arrivals declined following heavy rainfall and weaker transportation economics. At the same time, continued safety inspections in Shanxi slowed mine restarts, while heavy rainfall associated with Typhoon Bavi disrupted production at several open-pit mines in Inner Mongolia.

These developments tightened prompt coal availability across northern ports, encouraging traders to rebuild positions and prompting sellers to become increasingly reluctant to release cargoes in anticipation of further price increases.

The rebound was equally evident upstream. Mine-mouth prices across Shanxi, Inner Mongolia and Shaanxi increased by 10-30 yuan/t, while some producers lifted offers by as much as 50-60 yuan/t over the previous week. According to Sxcoal’s survey, eleven mines raised prices on July 14, compared with only four that reduced offers, highlighting the sharp improvement in producer confidence.

The rapid recovery has also lifted market psychology. Sxcoal’s thermal coal sentiment index has reached its highest level since late April, reflecting growing confidence that the market may have established a near-term price floor.

China’s thermal coal market is now moving at two different speeds

Perhaps the most significant development is that recent price movements no longer reflect the behaviour of the entire market.

Instead, China’s thermal coal market is increasingly dividing into two distinct segments.

The first is the spot market, where traders respond quickly to tightening prompt supplies, weather disruptions and logistics constraints. Here, reduced rail arrivals and constrained mine production have been sufficient to trigger speculative buying, improve sentiment and lift prices.

The second is the physical consumption market, where power utilities continue to operate under a completely different set of fundamentals. Utilities remain well supplied through long-term contracts, maintain comfortable inventories and have shown little willingness to increase discretionary spot purchases despite the recent recovery in prices.

This growing disconnect means that today’s price movements increasingly reflect the availability of prompt spot tonnes rather than any meaningful tightening in China’s overall coal balance.

For exporters and international suppliers, this distinction has become increasingly important. Rising prices may suggest improving fundamentals, but without stronger participation from utilities, the current rally remains vulnerable to losing momentum.

Utilities remain well supplied

The China Electricity Council (CEC) data reinforces this divergence.

Although coal-fired generation and coal consumption increased modestly during the week ended 9 July as summer temperatures gradually strengthened, utilities remain comfortably supplied.

Coal inventories at surveyed power plants stood at 116.89 mnt, equivalent to 25.7 days of consumption, while power plants supplied by coastal shipping have received more coal than they have consumed for 11 consecutive weeks, allowing inventories to continue increasing despite the seasonal rise in electricity demand.

Several factors continue to suppress spot demand.

Frequent rainfall across southern and eastern China has supported hydropower generation, reducing thermal coal burn. Long-term contracts continue to meet most utility procurement requirements, leaving little need for discretionary buying even as spot prices recover.

Consequently, much of the recent market activity has originated from traders repositioning themselves rather than utilities responding to tightening physical supply.

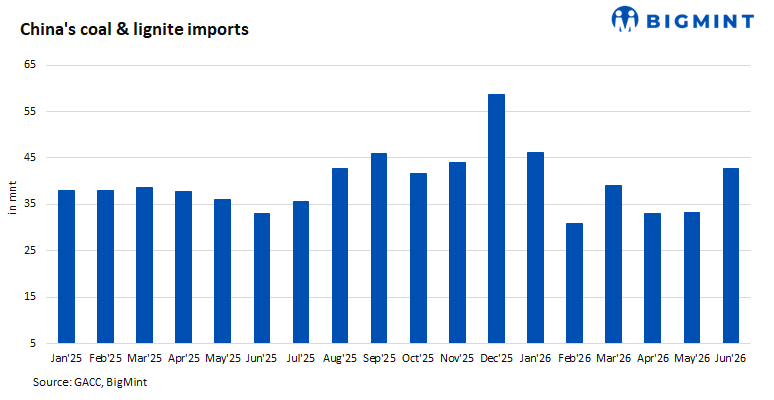

Imported coal market adequately supplied

The imported coal market presents a similarly mixed picture.

Higher freight costs and firmer overseas offers have supported imported prices, while strengthening domestic prices have encouraged some trading houses to rebuild positions. However, prompt fundamentals remain soft.

Large volumes of lower-calorific-value Indonesian cargoes continue to seek buyers, while inventories at South China ports remain elevated. Guangzhou Port held 3.41 mnt of imported coal as of 13 July, and utilities have largely completed procurement for August deliveries, with many already evaluating September cargoes.

This suggests imported coal is unlikely to provide additional demand support unless domestic consumption strengthens significantly.

Outlook

China’s thermal coal market has undoubtedly entered a more constructive phase after several months of persistent weakness. Supply disruptions, tighter logistics and constrained mine production have restored confidence and temporarily shifted pricing power back towards producers.

However, the sustainability of the recovery will depend on whether the second half of the market—the utilities—eventually joins the rally.

A prolonged period of intense summer heat could significantly increase air-conditioning demand, accelerate coal burn and begin reducing inventories, creating the physical demand needed to sustain higher prices. Conversely, if hydropower generation remains strong and utilities continue relying on existing inventories and long-term contracts, the current rally is likely to remain largely trader-driven.

For now, China’s thermal coal market is sending two very different signals. Traders are positioning for tighter supply and higher prices, while utilities continue behaving as though the market remains comfortably supplied. Until those signals converge, recent price gains should be interpreted as evidence of tightening spot availability rather than confirmation of a broad-based recovery in China’s thermal coal demand.

Leave a Reply