- Finished steel trade yet to regain pace

- Price stability will hinge on demand revival, liquidity flow

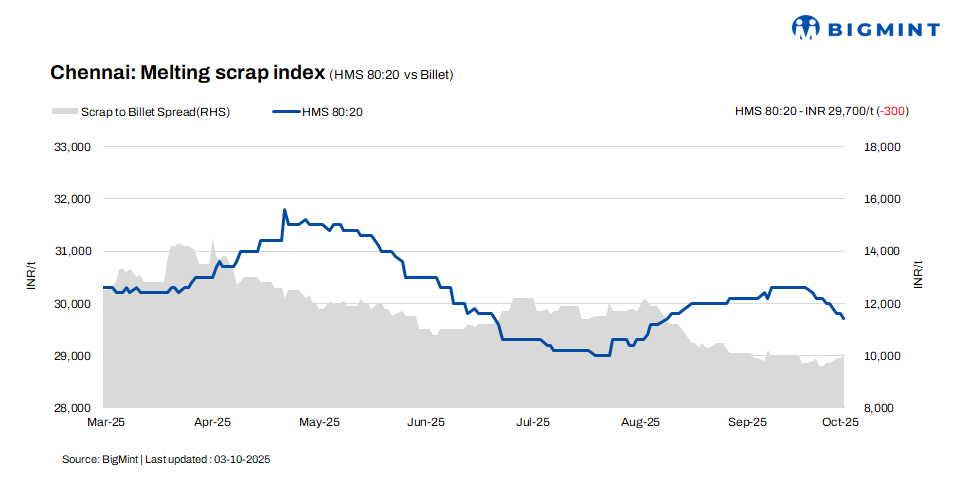

As of BigMint’s latest assessment, Chennai’s HMS (80:20) scrap prices saw a decrease of INR 300/t w-o-w, settling at INR 29,700/t, while dropping by INR 100/t d-o-d. In contrast, billet prices held steady, assessed at INR 39,700/t, both on a w-o-w and d-o-d basis. Rebar prices also remained unchanged d-o-d at INR 44,000/t, but decreased by INR 200/t over the week. Overall, the region displayed stability in immediate pricing with marginal weakness reflected in weekly trends.

Imported and domestic price trends

As per a scrap trader, Australian shredded scrap offers were reported at $350-355/t CFR Chennai, while HMS (80:20) stood at $325-330/t. Despite these levels, import demand remained muted as domestic scrap prices provided stronger competitiveness. Market participants continue to prefer local sourcing, highlighting the sustained price gap between imported and domestic material.

In Chennai, domestic HMS (80:20) scrap is being transacted at INR 29,500-30,000/t for spot deals with immediate payment, whereas deals on extended credit terms are fetching slightly higher rates of INR 30,000-30,500/t. The majority of offers and concluded deals were observed in the INR 29,500-30,500/t band, highlighting steady market dynamics and balanced buying activity.

Buyer-supplier sentiments

According to a mill representative, market activity has remained slow after the Dussehra holidays, with finished steel trade yet to regain pace. Billet offers stayed largely stable as sellers resisted lower bids, supported by the fact that several major billet producers also run re-rolling mills, enabling them to absorb material internally rather than sell at discounts. Meanwhile, rebar demand has softened, weighing on trade volumes and contributing to subdued sentiment in the broader steel market.

According to a local scrap supplier, domestic HMS (80:20) scrap is trading between INR 29,500 and 30,500/t, with marginal variation based on payment terms. While supply has been slightly tight, muted demand from the finished steel segment has prevented any significant price movement. Market participants expect scrap prices to remain range-bound in the near term, as subdued steel trade continues to offset supply constraints.

Regional comparison

In western India’s Jalna market, rebar prices held steady at INR 43,100/t, while billet declined slightly by INR 100/t to INR 38,000/t. HMS (80:20) experienced a sharper drop of INR 600/t, settling at INR 29,300/t. Market sources attribute the decline in scrap prices to production cuts by major mills, which are holding 15-20 days of finished steel inventory. The excess stock has reduced immediate buying requirements, exerting downward pressure on scrap prices, while rebar stability reflects cautious trading amid the slower demand and inventory-driven market dynamics.

Outlook

Although the market is experiencing a slowdown, scrap prices are projected to remain range-bound in the near term, with potential fluctuations restricted to about INR +/- 500/t. Traders note that price stability will largely depend on demand revival and liquidity flow, both of which remain uncertain. Until stronger buying activity emerges, the market is expected to hold steady within this narrow band.

Leave a Reply