- Higher Gujarat, Maharashtra output lifts supply outlook despite weak mill demand

- Rising imports and swelling closing stocks signal continued pressure on prices

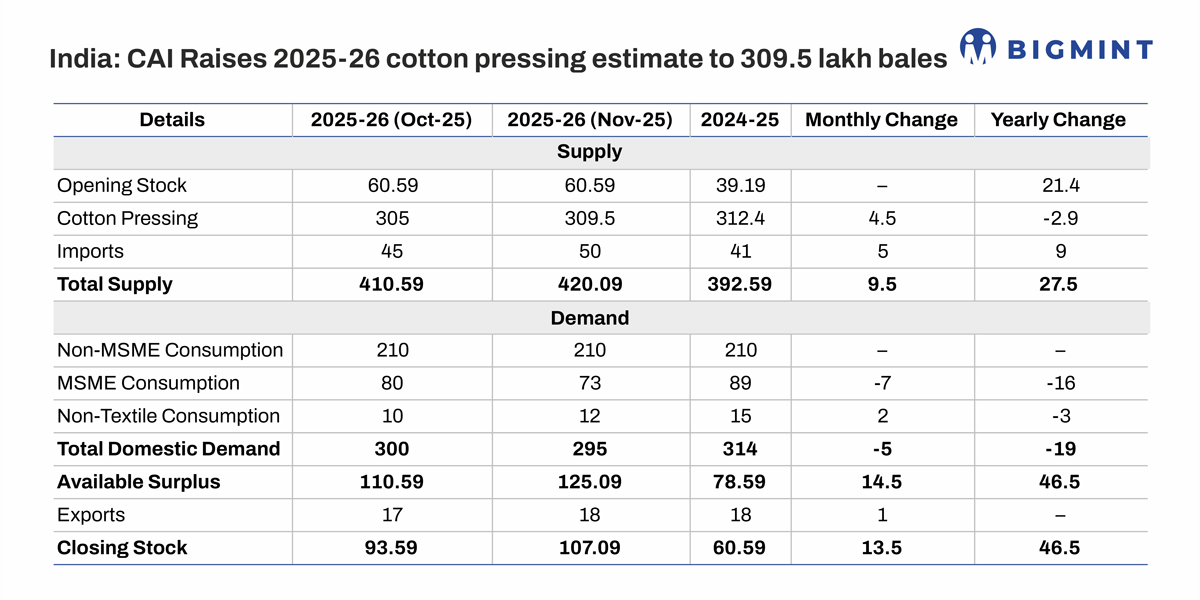

The Cotton Association of India (CAI) has revised India’s cotton pressing estimate for the 2025-26 season upward to 309.50 lakh bales (170 kg each), ±3%, an increase of 4.50 lakh bales from the previous estimate. The revision comes barely two months into the season that began on 1 October 2025 and reflects improved field and market feedback from key producing states.

Total cotton supply for the full season is now projected at 420.09 lakh bales, sharply higher than 392.59 lakh bales last year, largely driven by higher production and increased imports.

The upward revision is mainly due to better-than-expected pressings in Gujarat (+3 lakh bales) and Maharashtra (+3 lakh bales), which together offset declines in Telangana (-2.5 lakh bales). CAI noted that arrivals and ginning activity in western and central India have remained steady, supported by relatively better yields and smoother market movement compared to the southern zone where crop stress and yield loss continue to cap output. By end-November, cumulative pressings stood at 69.78 lakh bales, indicating a faster early-season pace than last year in Gujarat and Maharashtra, though Telangana continues to lag on a y-o-y basis.

Demand constrained

On the demand side, the picture remains weak. CAI has cut its 2025-26 domestic consumption estimate to 295.00 lakh bales, down from 314.00 lakh bales last season. The decline is concentrated in the MSME spinning segment, reflecting subdued yarn demand, tight working capital, and limited export orders. Consumption till end-November is estimated at just 48.40 lakh bales, highlighting cautious raw cotton buying by spinning millers despite ample availability.

Exports for the full season are maintained at 18 lakh bales, unchanged y-o-y, with shipments of only 3 lakh bales completed by end-November, underscoring India’s reduced competitiveness in global cotton trade.

Imports, however, are rising. CAI has raised its cotton import estimate to 50 lakh bales, up 9 lakh bales from last season, as spinning millers continue to source contamination-free and specification-friendly cotton from overseas. By end-November, 18 lakh bales had already arrived at Indian ports. With supply outpacing demand, closing stocks as on 30 September are projected at 107.09 lakh bales, nearly double last year’s 60.59 lakh bales.

Looking ahead, the CAI data clearly points to a supply-heavy, demand-constrained market. For ginners, higher pressings may sustain near-term liquidity but could increase price competition as stocks build. For spinning millers, abundant supply and rising imports may cap domestic prices, though yarn demand recovery remains the key missing link.

For brokers and traders, volatility is likely to persist, with market direction hinging on consumption revival, export competitiveness, and policy signals on imports and trade. Unless demand improves meaningfully in the second half of the season, the enlarged surplus is likely to keep cotton prices under pressure well into mid-2026.

Leave a Reply