- Weak Pacific enquiry pressures Panamax sentiment

- Slower fixture activity widens bid-offer gap

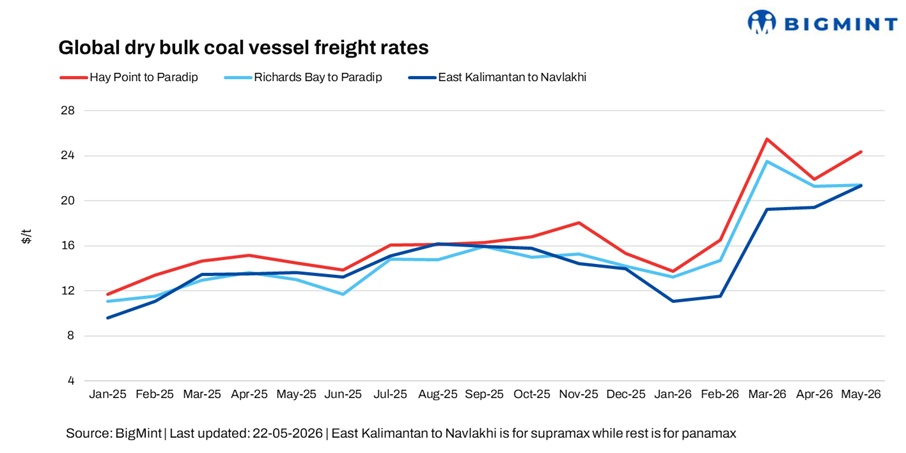

Dry bulk coal freights to India remained mixed in the week ended 22 May, with Pacific Panamax routes under pressure from weak enquiry and rising tonnage, while South Africa and Indonesia-linked routes stayed comparatively supported.

A shipbroker said, “The market is slow, not much firm enquiry is heard,” indicating cautious sentiment across key coal routes.

Route-wise update

In the Pacific, Panamax sentiment softened as limited Australia-India cargo enquiry and a growing list of open vessels weighed on freight ideas. Softer freight derivatives and easing bunker prices further pressured market confidence, with charterers bidding below previous fixture levels.

Another shipbroker informed, “Freight sentiment appears softer across Capesize, Panamax and Handysize segments, while Supramax remains relatively stable despite weaker FFA sentiment across vessel classes.”

Market participants told BigMint that fixture negotiations remained slow amid a widening gap between charterers’ bids and owners’ expectations. Presently charterers’ ideas are on the lower side while owners are expecting higher, so negotiations are taking long to materialise.

Meanwhile, the Atlantic market remained relatively steadier, with the RBCT-India Panamax route supported by tighter prompt vessel availability and stable India-bound coal stems.

In the Supramax segment, the Indonesia-India route continued to show resilience as firm coal movement and balanced Southeast Asia tonnage helped maintain sentiment despite softer trends in the larger vessel segments.

Market highlights

- Baltic Dry Index hits two-week low: The Baltic Dry Index (BDI) declined by 231 points w-o-w to 2,964 on 21 May, hitting a two-week low amid consecutive losses in the Capesize segment. The Panamax index fell sharply by 227 points to 2,276, weighing on overall market sentiment, while the Supramax index edged up by 13 points to 1,571, supported by steady minor bulk cargo demand and relatively balanced vessel availability across key trade routes.

- Bunker prices edge down w-o-w: Bunker prices fell by $32/t w-o-w to $803/t as of 22 May, from $835/t a week earlier, amid softer crude oil trends and easing buying interest across major bunkering hubs.

- Brent crude futures ease w-o-w: Brent crude oil (July 2026 contract) was last assessed at $105.5/bbl on 22 May, down by $2.8/bbl from $108.3/bbl a week earlier, amid easing supply concerns and softer global energy market sentiment.

- DCE coke futures decline w-o-w: Coke futures on the Dalian Commodity Exchange fell by RMB 76/t ($11.17/t) w-o-w to RMB 1,731/t ($254.44/t) as of 22 May, reflecting weaker market sentiment amid subdued trading activity and cautious downstream steel demand.

Outlook

Coal freights to India are expected to remain mixed in the near term. Panamax routes may continue facing pressure from subdued Pacific enquiry and rising tonnage, while Supramax sentiment is likely to remain relatively stable on balanced vessel supply and steady Indonesian coal demand.

Leave a Reply