- CBAM policy supports regional steel production sentiment

- Elevated freight costs continue pressuring export activity

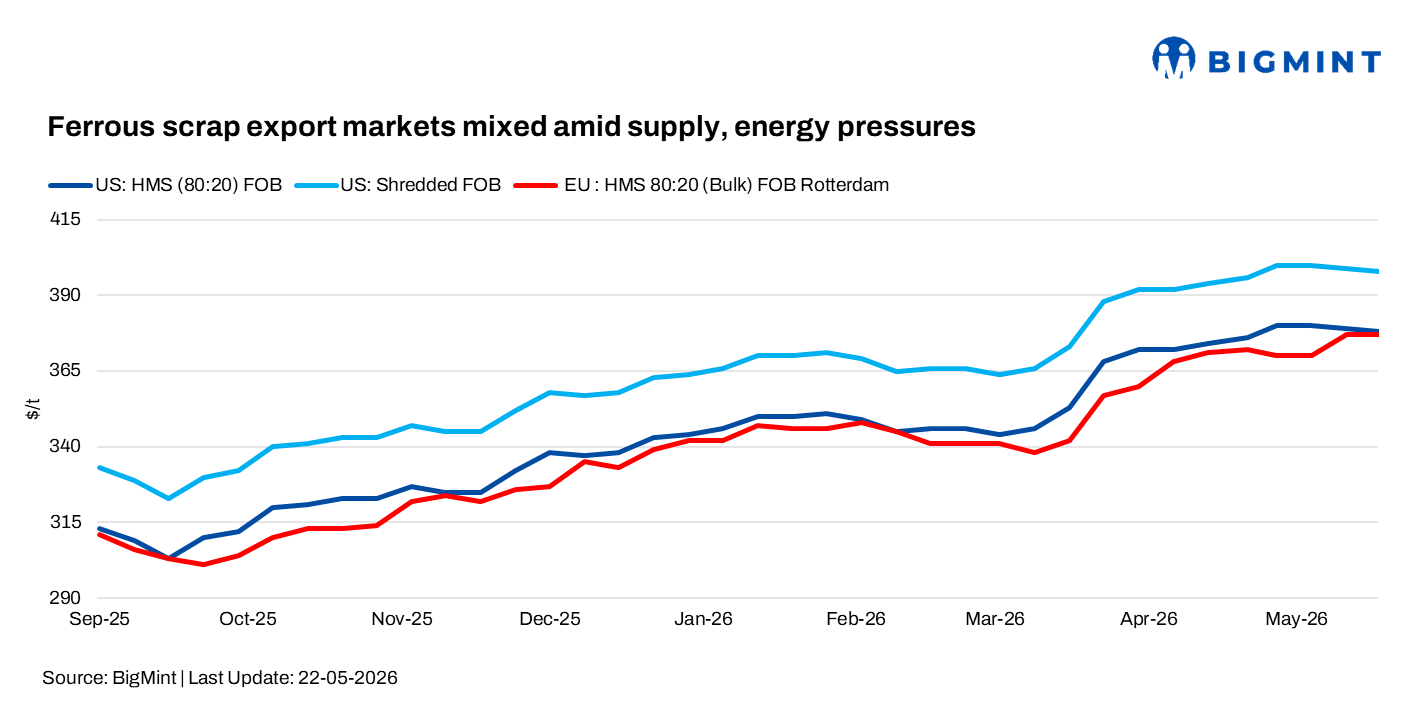

Ferrous scrap markets in key regions witnessed mixed sentiment during the week ending 22 May, as improving scrap availability and softer export demand pressured US obsolete grades, while elevated energy costs supported European prices. Meanwhile, Brazil’s market remained firm amid tighter domestic supply conditions, although export activity continued facing pressure from freight and currency-related challenges.

US ferrous scrap markets showed mixed trends during the week, with obsolete grades remaining under pressure while prime scrap prices stayed comparatively firm. US export HMS 80:20 prices were largely stable at $379/t FOB, while shredded scrap remained around $399/t FOB.

In the domestic market, Midwest shredded scrap prices were heard at $425-435/t delivered, while busheling prices increased to $455-465/t delivered from $440-450/t during April, supported by stronger flat steel demand, elevated pig iron costs, and improved steel mill margins.

Market participants noted that obsolete grades such as HMS and shredded scrap remained under pressure due to improving seasonal collection flows and ample supply availability. Softer export demand and elevated freight costs also kept more material within the domestic market.

European ferrous scrap markets remained firm during the week, supported mainly by higher steel production costs rather than improved downstream demand. German E3 (HMS 80:20) scrap prices increased to around euro 313/t ($364/t) from nearly euro 283/t ($329/t) in late 2025, tracking firmer steel prices.

Meanwhile, dock levels this week were heard at EUR 300-305/t ($348-354/t), down by EUR 5/t ($6/t) w-o-w.

A market participant said, “Rising energy costs and higher Dutch TTF gas prices, up around 50-60% since the start of the year, continued supporting steel prices, although weak construction demand limited scrap consumption growth.” Meanwhile, the EU’s CBAM policy continued supporting regional steel production by reducing import competitiveness, although weak downstream demand is expected to cap further upside in scrap prices and steel output.

Brazil’s ferrous scrap market witnessed upward price pressure during the week, although steelmakers kept purchase prices unchanged. Market participants reported increased price fluctuations among recyclers, supported by tighter supply conditions and relatively improved domestic rebar sales sentiment.

Market participant indicated some mills may have faced short supply positions despite continued pressure on steel margins. HMS 80:20 prices were stable at BRL 845-850/t ($169-170/t) FOT, turnings scrap at BRL 765-770/t ($153-154/t) FOT, and clean steel scrap at BRL 925-930/t ($185-186/t) FOT.

Export activity remained sluggish as a weaker Indian rupee, elevated freight costs, and forex volatility continued to squeeze trade margins. “We haven’t been able to close anything. Rupee and freight are hurting business,” a market participant said. Export HMS 80:20 prices held stable at $310-315/t FOB Brazil, while shredded scrap offers were heard at $330-335/t FOB.

Leave a Reply